|

In the first-quarter ended March 2015, Celgene Corp. [NASDAQ:CELG] reported total revenues of $2.08 billion, up 20.28% year-over-year and EPS with ex-items of $1.07, up 28.92% year-over-year. Wall Street was expecting earnings of $1.06 per share on revenues of $2.12 billion.

The company reported sales of their multiple myeloma drug, Revlimid, of $1.34 billion, up 17.4% year-on-year, in line with analysts' estimates of $1.33 billion. Revlimid now accounts for about 64.4% of Celgene's total revenues. On an operational basis, including the impact from both foreign exchange rates and hedging activities, Revlimid sales were up 19.3% year-over-year.

Abraxane, a cancer drug indicated for the treatment of breast cancer, non-small cell lung cancer and metastatic adenocarcinoma of the pancreas, posted sales of $223.4 million, an increase of 20.9% year-over-year. Sales were short of the $246 million analysts had expected, on average.

Looking forward, Celgene reaffirmed its revenues to be between $9.0 billion and $9.5 billion in 2015 and adjusted diluted EPS in the range of $4.60 to $4.75, compared with analysts' estimates for $4.77 per share on revenues of $9.25 billion. Celgene forecasts Revlimid sales to climb 14.5% to between $5.6 and $5.7 billion, as the company gains wider approval for the different lines of treatment.

For 2017, Celgene forecasts net product sales to be between $13 billion and $14 billion, and EPS of $7.50. The company expects to more than double its hematology and oncology sales in 2020 to $20 billion with an EPS of $12.5 per share.

Celgene signed a partnership in April with London-based AstraZeneca Plc [NYSE:AZN] to co-develop an experimental therapy for blood cancers and paid $450 million upfront to share rights to the anti-PD-L1 inhibitor, a new type of cancer drug that takes the brakes off the body’s immune system, helping it fight malignancies.

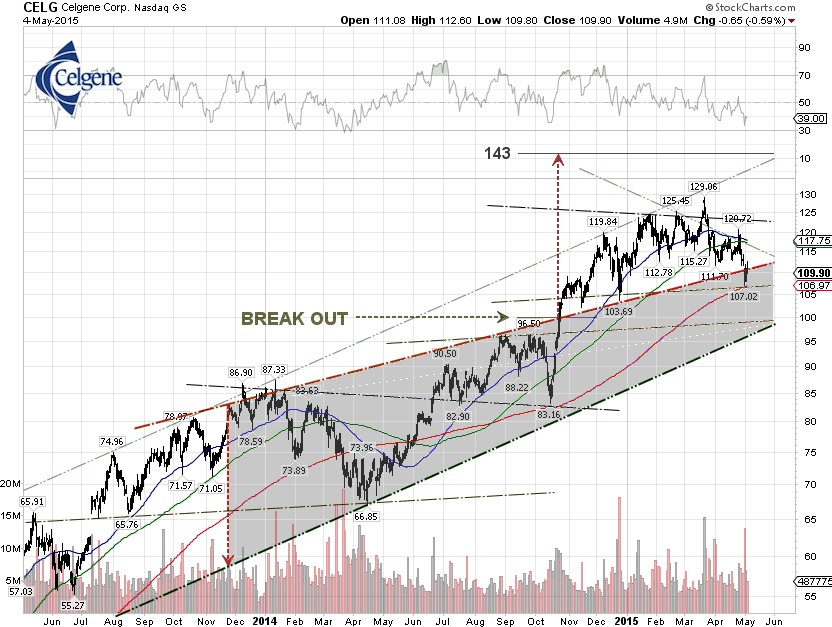

Since December 2014, CELG has been moving in a rising wedge chart pattern. The stock broke out of the rising wedge in October 2014. A key near-term risk is the polymorph patent (EP682) hearing in front of the European Patent Office on May 7th. A negative outcome for Celgene would drastically limit patent protection for Revlimid for myeloma in Europe beyond June 2022. Leerink’s analysts, however, don’t believe the European hearing will have much impact on U.S. patents.

Other headline risk could be the strong U.S. currency as Celgene sees the negative impact of foreign exchange on net product sales to approach $100 million in 2015.

It needs to be pointed out that CELG is traded along with the Nasdaq Biotechnology Index [NASDAQ:IBB] and maybe counter traded with Market Vectors Semiconductor ETF [NYSEARCA:SMH].

From our technical analysis, the price projection for CELG is $143.00, determined by adding the width at the top of the pattern to the point of breakout. The stock ran up in the first-quarter of this year when Celgene said its hematology and oncology sales would more than double by 2020. The stock has pulled back about 17.43% since it peaked in March at $129.06. There is key technical support at around the $100 level, if the stock decides to pull back further.

Last week, Leerink maintained its price target for CELG at $150.00.

Disclosure: Long Position CELG in Portfolio |