|

The U.S. dollar index (DXY) immediately ran up 0.43% to an intraday high of 98.33 on Friday, right after the U.S. Department of Labor released the non-farm payrolls report saying that the July jobs numbers came in with a 215,000 increase, down 11.52% year-on-year and below the Wall Street estimate of a 225,000 gain. The May and June numbers were revised up to 260,000 and 231,000, respectively, resulting in a 14,000 more jobs gained during the periods.

The DXY run-up lasted only two hours though, as the index pulled back sharply before the close of the European markets to a level below the previous day’s close of 97.83.

The Department of Labor also said the July unemployment rate stood at 5.3% and more than 144,000 people left the labor force, pushing the labor force participation rate to a 38-year low at 62.6%, meaning a record 93.8 million Americans, 16 years and older, did not have a job and were not actively trying to find one. Although the labor force participation rate seemed to stabilize at 62.6% in June and July, the troubling part is that more than half a million people left the labor force during that period.

The dollar has been strengthening since the FOMC meeting on July 29, as the Fed made it clear to the market that it will hike the rate this year, regardless of the tepid U.S. economy. The forward and backward looking U.S. economic data of late have been mixed at best. The U.S. Bureau of Economic Analysis said on July 30 that the first estimate of second quarter 2015 U.S. GDP was 2.3%, missing expectations of 2.6%. For the first half of 2015, the GDP was revised upward to 1.45% from 1.25%.

The Federal Reserve Bank of Atlanta said this week that the third quarter GDP could dip to 1.0%, as inventory adjustments are likely to slash growth again, compared to 2.3% growth in the second quarter.

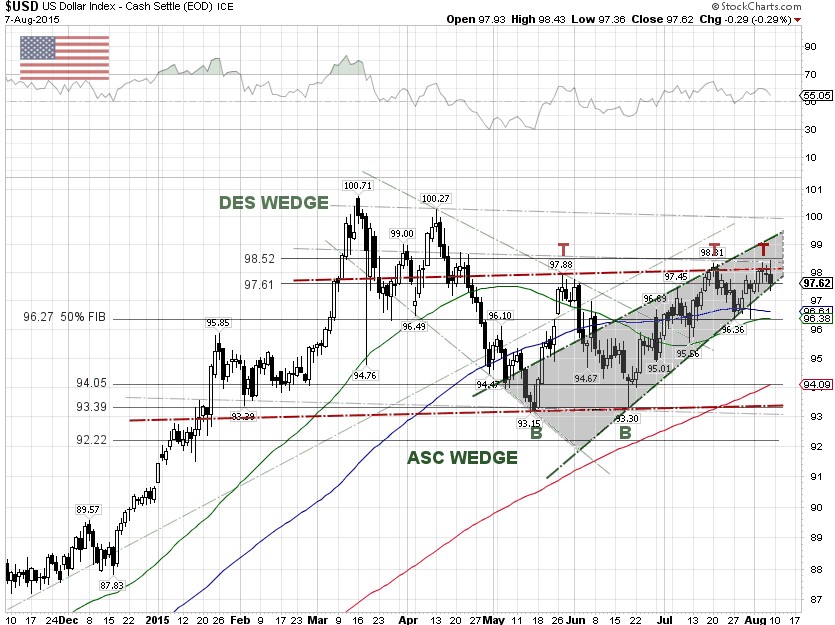

Technically, the U.S. dollar index has been moving in a bearish ascending wedge pattern since mid-June. The DXY was unable to break out the trendline head resistance at about the 98 level, twice since mid-July. The index is at risk of an ascending wedge breakdown, resulting in a pullback to retest 96.27, or the 50% Fibonacci retracement level. If the U.S. dollar index falls below the 96.27 level and the double top is confirmed, our near-term target for the DXY is 95.

The headline risks for the U.S. dollar index next week are the JOLTS report on Wednesday, the U.S. retail sales due on Thursday, and the eurozone April-June GDP due on Friday. |