|

Goldman Sachs is now backtracking on their call for euro-dollar parity. According to The Wall Street Journal, Goldman’s chief FX strategist Robin Brooks wrote in a note last Monday that the bank now sees the euro at $1.07, $1.05 and $1 in three, six and 12 months, respectively. Previous forecasts for those time horizons had been $1.02, $1 and $0.95. Goldman Sachs had said in March that the euro would hit parity with the dollar by September.

As of December 8, there are 182,251 short positions of euro FX, traded on the Chicago Mercantile Exchange (CME), by leveraged funds, a week-over-week decrease of 15,470 short positions. This is compared to about 42,876 long positions, up 1,881 from the previous week, according to the Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC). During the week ending December 8, hedge funds have increased their net long positions about 17,351 contracts, where euro FX contracts are traded in units of 125,000 euros.

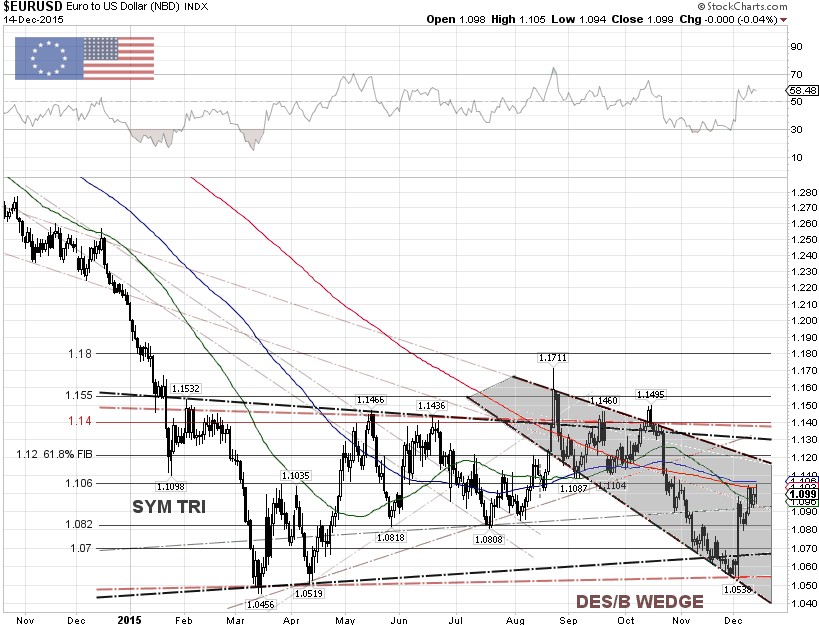

Technically, the EUR/USD currency pair has been trading in a symmetrical triangle band, between the 1.045 and 1.155 dollars per euro levels. The hedge funds are cutting back their short positions, as the currency pair is moving upward in a bullish descending broadening (DES/B) wedge.

A headwind for the dollar could be coming from the People’s Bank of China (PboC), as the bank set the daily reference at 6.4358 yuan to a dollar on Friday, the lowest since August 5, 2011, according to the PBoC’s China Foreign Exchange Trade System. Since China stunned financial markets by devaluing the yuan in August, the PBoC move would be to sell dollars to support the yuan. Tommy Xie, a Singapore-based economist at Oversea-Chinese Banking Corp, told Bloomberg News that he hasn’t seen any decisive intervention this week, but they may come back in after next week’s FOMC meeting.

Another headwind for the dollar is the U.S. high-yield bond market, which sooner or later will blow up, according to Carl Icahn, activist investor and fund manager of $30 billion Icahn Capital Management. Tumbling crude oil prices put more of a squeeze on small energy companies that sell high-yield, or junk bonds, to finance their operations. There could be as much as $212 billion worth of U.S. energy junk bonds out there, according to Bank of America Merrill Lynch. Standard & Poor's Ratings Service recently warning that a 50% of energy junk bonds are "distressed," meaning they are at risk of default. |