|

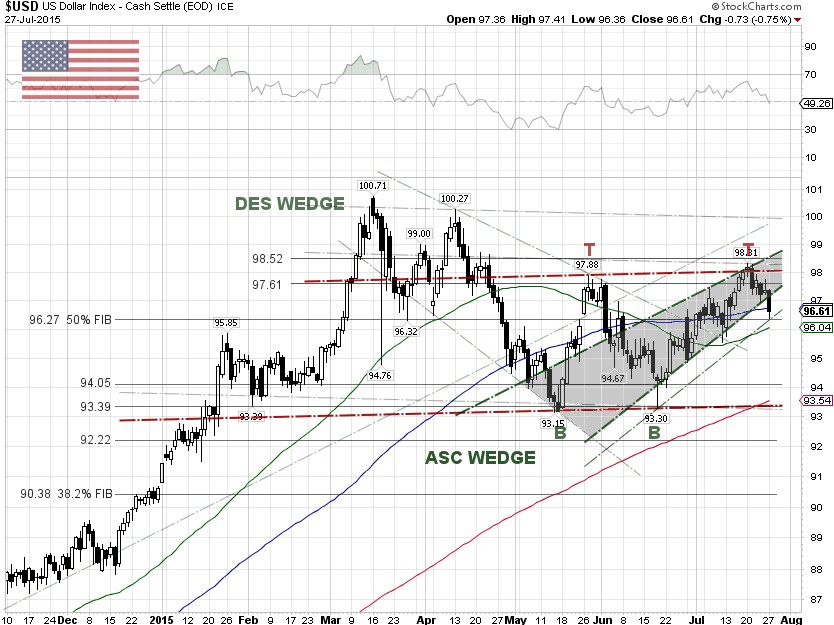

The U.S. dollar index (DXY), a weighted geometric index of the value of the U.S. dollar relative to a basket of six major currencies, tumbled 1.01% on Monday to an intraday low of 96.36, or around the 50% Fibonacci retracement level, as the Shanghai composite index plunged 8.48% after reports said that brokerages, who have been extending credit during the crisis, have begun restricting margin trading. The news sparked panic selling, especially among China's neophyte retail investors.

The euro, which is 57.6% weighted in the DXY index, surged 1.06% against the dollar as Chinese stocks unraveled. The Greek debt crisis appears to be on the back burner, as the Greek government is ready to start the 86 billion euro bailout talks after a delay due to a lack of a secure location in Athens.

Hedge funds might have been exiting the dollar trade after the housing data, reported by the U.S. Commerce Department on Friday, showed that new U.S. single-family home sales fell in June to a seven-month low and May's sales were revised sharply downward. As economic outlooks in both China and the U.S. are wobbly and tilting to the downside, the Fed is risking losing their credibility if they decide to hike the rate in September, and it botches the U.S. and global economy next year.

Bond king Jeffrey Gundlach, CEO of the DoubleLine Capital with about $46 billion under management, disagreed with Fed Chair Janet Yellen and said the Fed won’t raise rates in 2015. The U.S. FOMC meeting on July 28-29 may provide some direction on the interest rate and U.S. currency.

Technically, the U.S. dollar index is breaking down the bearish ascending wedge pattern. The DXY bounced off 96.27, or the 50% Fibonacci retracement level. If the 96.27 level breaks down, the U.S. dollar index could head back to retest the 94.05 support level. |