|

The

bond market sees it differently though, as it is betting against

the possibility that the Federal Reserve will raise interest

rates in December. The yield spread between the 10-year and

2-year Treasury Notes has been falling since July 10, at 1.77

percentage points, and just broke the March 24 support of 1.30

percentage points. The next support level for the 10-year and

2-Year yield spread is the February 2 support of 1.19 percentage

points.

Falling spreads may indicate worsening economic conditions in

the future, resulting in a flattening yield curve. A very low or

negative spread could signal an upcoming recession.

A mixed bag of economic data released last week by the U.S.

Commerce Department from the U.S. gross domestic product (GDP),

durable goods, core personal consumption expenditures (PCE) and

consumer spending have sent the yield of the 10-year Treasury

Note tumbling 2.25% in a week, to close on Monday at

2.213%.

The Commerce Department said last Tuesday that the second

estimate of the third-quarter U.S. GDP came in at 2.1% on a

year-on-year basis, in line with economists' expectations. The

upward revision, however, came mostly from the decrease in

private inventory investment, which was smaller than previously

estimated, meaning businesses accumulated more inventories in

the third-quarter than the government thought. Strong inventory

accumulation by businesses could hurt growth in the

fourth-quarter.

The Commerce Department also reported that the preliminary estimate for corporate profits from current production, adjusted for inventory valuation and capital consumption, decreased $22.7 billion in the third-quarter, in contrast to an increase of $70.4 billion in the second-quarter. According to Reuters, corporate profits, which have been undercut by the dollar's strength and lower oil prices, were down 8.1% from a year ago, the biggest decline since the fourth-quarter of 2008.

By definition, the latest FactSet data showed that the S&P 500 companies are officially entering into “earnings recession”, meaning two consecutive quarters of year-over-year declines in earnings.

The Commerce Department said on Wednesday that the non-defense, or “core” capital goods orders, excluding transportation items such as aircraft, increased 1.3% last month, beating expectations for a gain of 0.2%. Shipments of core capital goods, a category used to calculate quarterly economic growth, decreased 0.4% in October, worse than the forecasted drop of 0.3%.

The Commerce Department also said that core inflation, excluding food and energy as measured by the PCE price index, rose 1.3% year-on-year, remaining unchanged for 10 months and below the Federal Reserve’s target of 2% for the 42nd straight month. Consumer spending came in with a 0.1% increase, missing the Reuters forecast of a 0.3% rise.

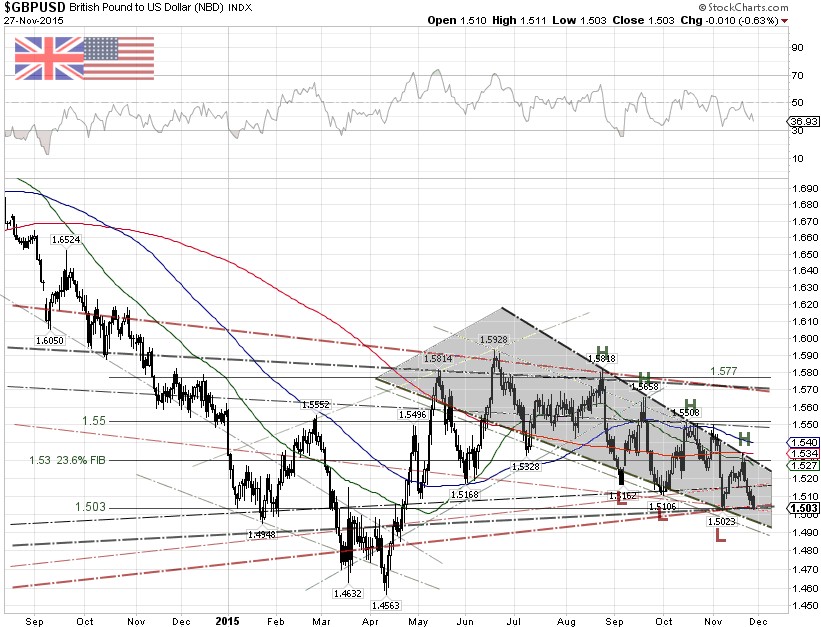

As of November 17, there are 39,753 short positions of British pound sterling, traded on the Chicago Mercantile Exchange (CME), by leveraged funds, a week-over-week decrease of 1,718 short positions. This is compared to about 48,717 long positions, down 507 from the previous week, according to the Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC). Hedge funds have slightly increased their net long positions about 1,211 contracts from the previous week, where British pound sterling contracts are traded in units of 62,500 GBP.

The currency markets are apparently more worried about the Fed rate hike at the December FOMC meeting and less about the weakening U.S. economy, as seen by the flattening yield curve. A near-term risk for the British pound sterling is the U.S. non-farm payrolls report due on Friday, December 4, 8:30 AM ET. The market is expecting a 200K jobs gain, with unemployment rate unchanged at 5.0%. |