|

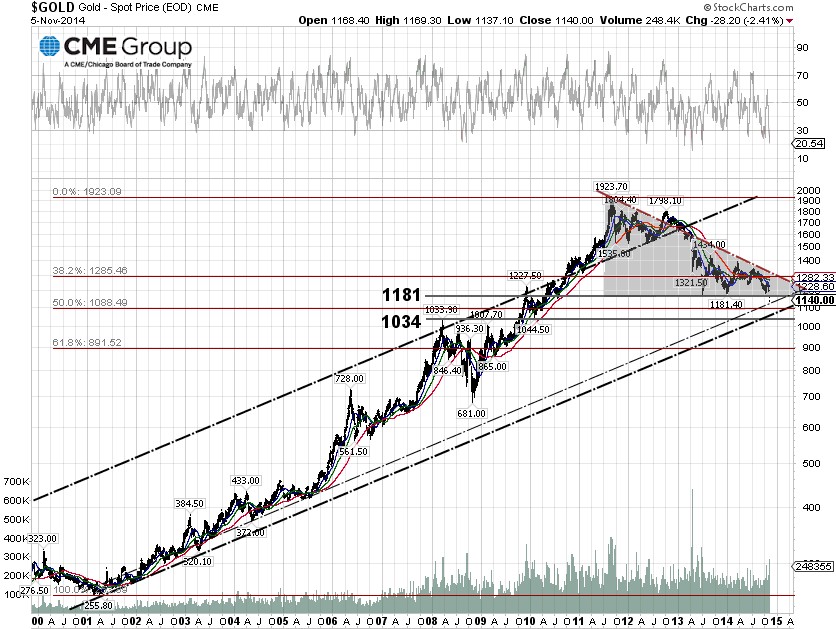

Here is the 15-year chart of the gold spot price on the Chicago Mercantile Exchange (CME). The unit is $USD per ounce, not inflation adjusted. Basically, the gold price rises and falls along with inflation, measured by the consumer price index (CPI). In mid-2005, the housing bubble began in the United States and ended with a big burst in early-2008, resulting in a retreat of the gold price from US$1033.90 per ounce to US$ 681.00 per ounce.

In early-2009, the US Federal Reserve began quantitative easing (QE) and expanded its balance sheet by approximately US $1 trillion a year. The gold price and equity markets responded to the Fed’s injected liquidity until mid-2011, where the gold bubble began to form. In 2011, the hedge funds started piling into the gold ETF, known as “GLD”.

The gold ETF burst in 2013 as China’s economy began to slow down and the “PIGS” (Portugal, Italy and Greece and Spain) were drowning in deep debt. “PIGS” is the acronym started by Mr. Paul O’Neill, chairman of Goldman Sachs Asset Management. The European economic mess escalated, which shot the US dollar to the moon and nose-dived the euro and gold price.

From an asset management viewpoint, we can’t evaluate the value of gold because gold has no earnings and gives no dividends. From a technical viewpoint, the “buying USD and selling (shorting) gold” trade is over crowed, but it is possible that the gold price could dip to ~US$ 1089 per ounce level (50% Fibonacci Retracement). If the gold price drops below US$ 1000 per ounce, the central banks could step in and shift their policy from being net sellers to buyers, but there is no guarantee. |