|

The SET tumbled 1.28% on Tuesday, along with most of the Asian-Pacific stock indices, including the SENSEX, PSEi and STI, down 2.37%, 1.54% and 1.51%, respectively, as the global bond markets sold off. It got started in Germany where the Germany 10-Year bond yield skyrocketed 31.39% on Tuesday, on the top of a 8.79% surge on Monday, that pushed the yield upward from 0.486% to 0.699% in two days. The Thailand 10-year bond yield inched up just 1.42% on Tuesday.

The global bond sell-off could have been triggered by the previous Friday’s release of the second estimate of the first-quarter U.S. GDP by the U.S. Department of Commerce, showing that U.S. GDP contracted 0.7% in the first-quarter this year, instead of the initial reading of a 0.2% gain. The number still beat Wall Street economists’ forecast of a 0.9% contraction.

The Ministry of Commerce of Thailand said on Tuesday that the consumer price index (CPI) fell 1.27% year-on-year in May, missing the Reuters’ forecast of a 1.12% decline. The core inflation rate, which strips out food and energy prices, rose just 0.94% in May, compared to 1.02% in April. May’s headline CPI may give more room to the Bank of Thailand's monetary policy committee for more rate cuts to spur growth.

Finance Minister Sommai Phasee disputed the more rate hikes scenario, as he put it on Wednesday, that the country had no need for further rate cuts as the two recent ones were sufficient, according to Reuters. Last month, the ministry revised the full-year 2015 GDP downward to 3.5%, from 3.7%, the third GDP downward revision this year as the Thai economy has struggled to regain traction.

Thai consumer confidence remains weak as the consumer confidence index fell to 75.6 in May from 76.6 in April, the lowest reading since June last year, according to this week’s survey by the University of the Thai Chamber of Commerce. The Bank of Thailand committee meets next on June 10. Most analysts expect no policy change.

The EUR/THB exchange rate jumped 1.02% to an intra-day high of 37.974 baht per euro on Wednesday, after European Central Bank (ECB) President Mario Draghi said at their conference that the Eurosystem staff macroeconomic projections foresee annual Harmonised Indices of Consumer Prices (HICP) inflation at 0.3% in 2015, 1.5% in 2016 and 1.8% in 2017. In comparison with the last forecast in March, the inflation projections have been revised upwards for 2015 and remain unchanged for 2016 and 2017. HICP is the consumer price inflation measured in the eurozone.

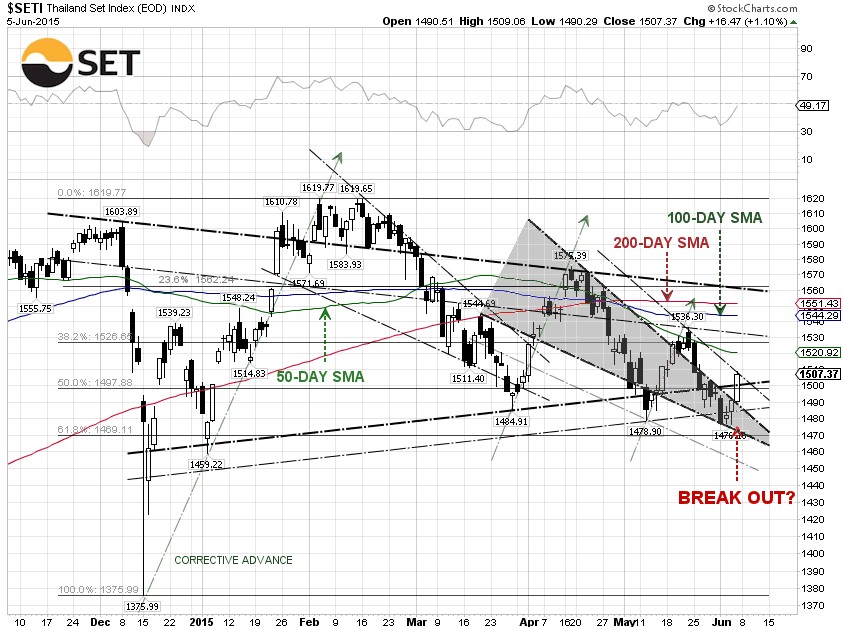

The USD/THB exchange rate ran up to an intra-day high of 33.96 baht per dollar on Friday, a fresh six-year high, before pulling back to close on Friday at 33.91 baht per dollar, up 0.62% for the week. The 10-year Thailand Government bond yield jumped 10.68% for the week to close at 3.11% on Friday. The yield spread between the U.S. 10-Year Treasury, yielding at 2.409%, and the Thailand 10-Year Government bond has narrowed to 0.701%. The SET closed at 1,507.37 above the psychological level of 1,500, up 0.76% for the week.

From our technical viewpoint, the SET appeared to bounce off the trendline support driven by the headline news after the ECB meeting that the ECB began to see inflation picking up in the eurozone. A weak baht makes Thai exports more competitive in the eurozone and around the globe. Rising Thailand bond yields could also give the financial sectors some tailwinds.

In order to continue its upward trend, the SET needs to break out the trendline resistance at 1,507. The next head resistances are the 50-day SMA at 1,521, 38.2% Fibonacchi level at 1,526.66 and the trendline resistance at the 1,530 level.

The headline risk when the SET opens on Monday is the U.S. non-farm payroll report, which came in better than expectations on Friday. The U.S. Bureau of Labor Statistics said that the U.S. government and private businesses added 280,000 jobs in May to the U.S. economy, above the 3-month average of 207,000 jobs and the 12-month average of 257,000 jobs, according to our data. More decent numbers like this in the June report could definitely trigger the first rate hike in September.

The negotiations between Greece, the ECB and IMF creditors are beginning to look like a “dog and pony” show, as the goalposts have moved several times, even though the expiration of its bailout program is June 30. Since Mr. Draghi said that he wants Greece to remain in the eurozone, we expect that the Greek debt negotiations will yield a positive outcome, despite tough talk from both sides. Nonetheless, a negative outcome could trigger a global market sell-off. |