|

Based upon our analysis, the U.S. 10-year Treasury yield could move near-term to 2.5% and 2.66%, or the 23.6% Fibonacci retracement level, making the spread between the U.S. 10-Year Treasury and the 10-year Thailand Government bond yields even narrower. From mid-May until last week, the yield spread between the U.S. 10-Year Treasury and the Thailand 10-Year Government bond, was pegged between 0.70% and 0.72%.

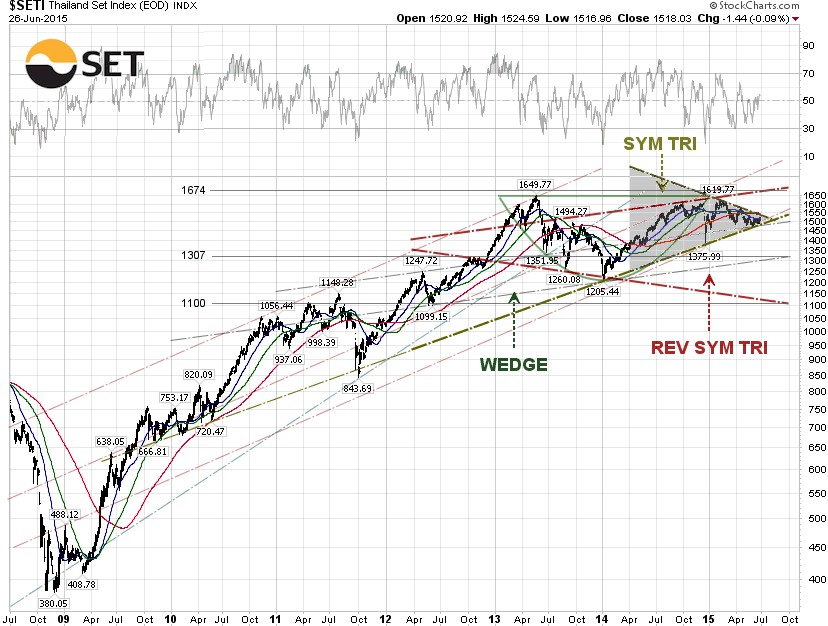

From a short-term technical viewpoint, the SET broke through the 50-day SMA and closed above the 50-day SMA for the first time since late April. The concern is still that the SET is moving in a short-term bearish lower high (L-H) chart pattern since it peaked in February, meaning every high is lower than the previous high while every low is lower than the previous low. This lower high chart pattern signals a bearish downtrend, unless the SET is able to close above the H4 level, or 1,518.44.

From the long-term technical viewpoint, the SET has been moving in a bearish rising wedge pattern since July 2013. In February, a symmetrical triangle emerged, in which the SET is now bouncing along the lower trendline support. From now until August, the market will have to decide in what direction it will move next. In the event of a symmetrical triangle breakdown, the supports are at 1,307 and 1,110. If the SET breaks out to the upside, the head resistances are 1,649.77 and 1,674.

The headline risk for next week is still the Greek debt drama. Greece needs the funds to make a €1.5 billion repayment to the International Monetary Fund (IMF) by June 30. Greece’s creditors, including the eurozone, European Central Bank (ECB) and the IMF, proposed a five-month bailout extension but it was rejected by Greek Prime Minister Alexis Tsipras. Mr. Tsipras accused the creditors of using “unacceptable” tactics employed by interlocutors representing foreign lenders at the EU, ECB and IMF.

The eurozone finance ministers and Greece’s creditors are now drawing up plans for emergency measures to ring fence Greece’s financial system, if Greek PM Tsipras refuses to give in. If Greece defaults next week, the risk that a crisis spreads into the global financial system and bond markets may be limited, as about 83% of Greek government debt is now held by official creditors, not by banks and private sector institutions.

Related Tickers [NYSE:THD] and [NYSE:TTF] |