|

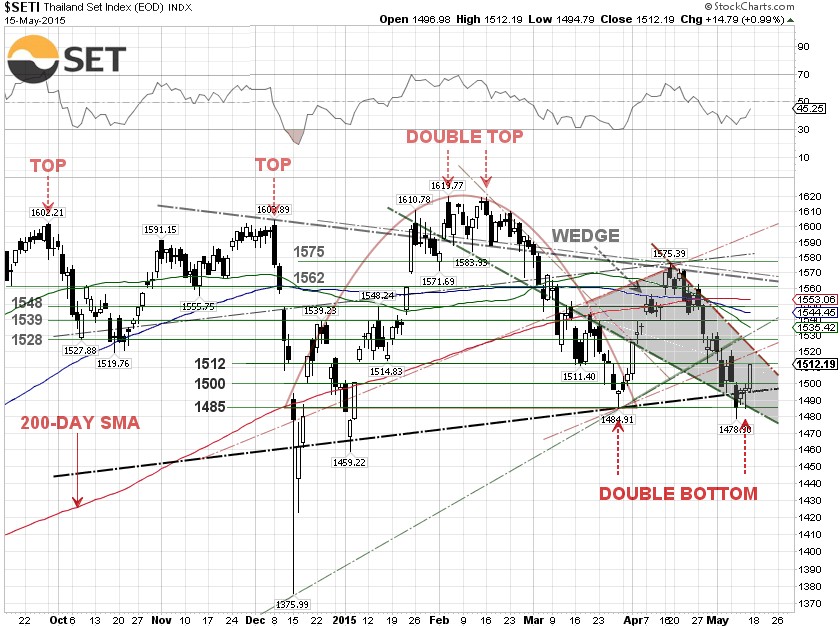

The Thailand SET bounced off the 1,485 support level on Thursday after Finance Minister Sommai Phasee said that he is lowering the growth forecast to 3.5%, from the 3.7% announced in late April. This will be the third GDP cut this year as the economy has struggled to regain traction. In late January, the Fiscal Policy Office (FPO), the Finance Ministry's think tank, made their first adjustment to the economic growth projection for 2015, down to just 3.9% from the previous 4% forecast in December 2014.

The Thailand SET, which is traded in an inverse correlation with the dollar-baht (USD/THB) exchange rate, took a 1.49% nose dive on Tuesday to an intra-day low of 1,478.90, after the USD/THB hit the intra-day high at 33.90 baht per dollar. The baht made an oversold bounce as the USD/THB pulled back from 33.85 baht per dollar, the trendline resistance. For the week, the USD/THB exchange rate dipped 0.21% from last week to close at 33.48 baht per dollar.

The Thailand 10-year Government bond yield climbed another 2.07% for the week to close at 2.96% on Friday, after the yield skyrocketed 17.89% last week. It should not come as a surprise as major government debt markets, including Germany, the U.S. and the U.K. have seen also a dramatic sell-off, sparking stark jumps in bond yields.

The sell-off in global sovereign bonds, lead by German Government bonds or Bunds, is either an unintended consequence of the quantitative-easing program or a result of growing optimism that the QE program is working and inflation is rebounding. Ordinarily, that would lead to higher bond yields.

Until mid-April, hedge funds were pushing the yield on the German 10-year Government bond to a record low of 0.049%. Hedge funds unwinding their positions could be responsible, in part, for the surge in the German 10-year Bund yield, which was 0.635% at the close on Friday. Paper losses across the spectrum of the global bond markets are roughly half a trillion dollars, according to Bloomberg.

|