|

The SET managed to close up 0.35% for the week at 1,370.75 despite weak economic news from China, the U.S. and EU. The resiliency in the Thailand stock market could be due in part to the government stimulus package, and in part because the Shanghai Stock Exchange was closed on Thursday and Friday. The foreign investors were still selling, with the net sells so far this month of about 3.04 billion baht. The year-to-date foreign investors’ net sells now top 89.4 billion baht, up over 2000% from the same period last year.

The Thai baht was weak and traded as low as 36.206 baht per dollar during the week. One should pay attention to the THB/JPY exchange rate, as the currency pair is now traded at 3.3085 yen per baht, down 2.57% in one week.

Deputy Finance Minister Wisut Srisuphan told reporters on Tuesday that the government of Thailand approved a 136 billion baht stimulus package, or about 1% of the Thai GDP in 2014. According to Bangkok Post, the Thai government will spend about 35 billlion baht for construction and repair works on small villages nationwide, meaning the big winner could be companies such as Siam Cement [SET:SCC].

Concerns about China’s economic hard landing have been raised throughout the week as the data from China were weak. The Chinese Government said on Tuesday that China’s official manufacturing purchasing managers index (PMI) fell to 49.7 in August from 50 a month ago, missing the market forecasts of 49.8. A PMI reading below 50 indicates contraction in the sector and a reading above 50 indicates expansion. The government’s non-manufacturing PMI also released on Tuesday, fell to 53.4 from 53.9 in July.

Separately, the final Caixin China Manufacturing Purchasing Managers’ index came in on Tuesday at a more than six-year low of 47.3 in August, from 47.8 in July, according to publisher Caixin Media Co. and research firm Markit, which compiles the index. The Caixin China Services Purchasing Managers’ index fell to 51.5 in August, from 53.8 in July, the slowest increase in 13 months..

The Institute for Supply Management (ISM) said on Tuesday that its U.S. Manufacturing Purchasing Managers index fell to 51.1 in August from 52.7 in July, the weakest reading since May 2013. Economists surveyed by The Wall Street Journal had expected the August PMI to hold steady at 52.7. So, it is a miss.

The Federal Reserve seems to be rosy on the U.S. economy as their Beige Book, which is practically a summarized report on current economic conditions in each of the Fed’s 12 districts, said Wednesday that the U.S. economy expanded across most regions and industries in July and August as tighter labor markets boosted wages for some workers.

The University of the Thai Chamber of Commerce said on Thursday that its consumer confidence index dropped to 72.3 in August from 73.4 in July, the lowest reading since May 2014, citing weak exports and the deadly bomb blast in Bangkok last month as the reasons for the dip. The University said the stimulus could boost economic growth by 0.7-1.0 percentage point this year, but maintains its growth forecast of 2.5-2.9% for 2015.

On Thursday, the European Central Bank (ECB) downgraded its inflation forecast for next year to 1.1%, from its June forecast of 1.5%, and the eurozone GDP growth in 2016 to 1.7%, from its June forecast of 1.9%. ECB President Mario Draghi said the central bank could extend the 60 billion euro monthly bond-buying or quantitative easing (QE) program beyond its original deadline of September 2016.

The U.S. Labor Department said on Friday that the U.S. non-farm payrolls came in at 174,000 for August, well below Wall Street economists' expectations of 222,000. The jobs reports missed expectations for three months straight.

The U.S. unemployment rate fell to 5.1%, from 5.3%, the lowest since early 2008, as more than 261,000 people left the labor force in August, pushing the labor force participation rate to a 38-year low at 62.6%, meaning 94 million Americans, 16 years and older, did not have a job and were not actively trying to find one.

There could be a spillover to the Asian markets on Monday as the S&P 500 tumbled 1.51% on Friday, after the disappointing non-farm payrolls report. The U.S. 10-Year Treasury Note yield dipped 2.29% while the U.S. dollar was weak. Currency traders were selling the U.S. dollar, British pound and euro and moved their cash into the Japanese yen as a safe-haven trade. The USD/JPY currency pair tumbled 1.22%, to as low as 118.61 yen per dollar, while the EUR/JPY dipped 1% to an intraday low of 132.23 yen per euro on Friday,

It seems that the market is now questioning whether the U.S. economy is strong enough to take a Federal Reserve rate hike if they decide to do it on September 17.

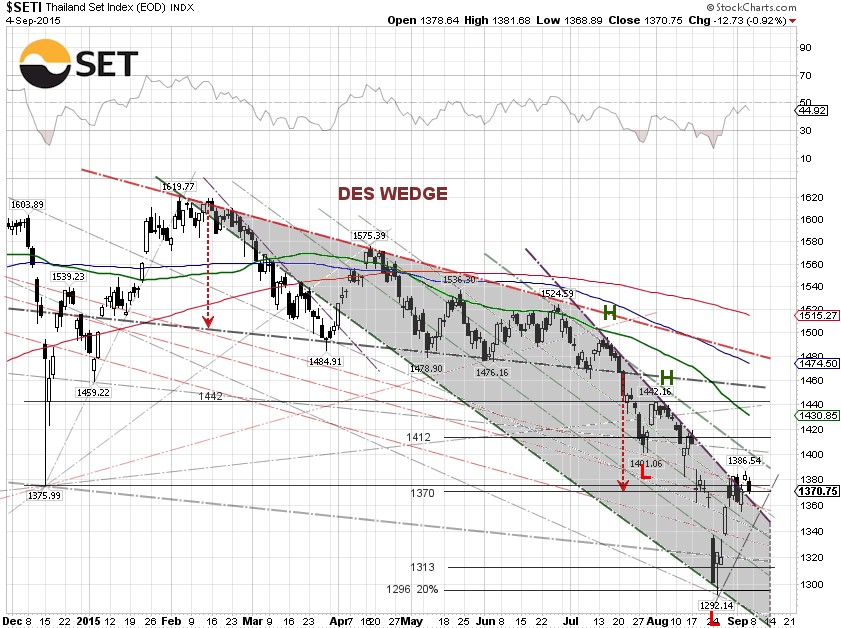

Technically, the SET broke out the trendline resistance of the descending wedge, but is stuck at the 1,370 support level. The breakout could be a false breakout if the SET pulls back below the trendline resistance in the coming days.

The SET still continues moving in a lower high (L-H) chart pattern, meaning every high is lower than the previous high while every low is lower than the previous low. This lower high chart pattern signals a continuous bearish downtrend, unless the SET breaks out the 1,440 level. The next head resistances are at 1,390 and 1,400.

One should keep an eye on China’s trade data on Tuesday and inflation on Thursday. The G20 meeting in Istanbul is probably another dog-and-pony show. |