|

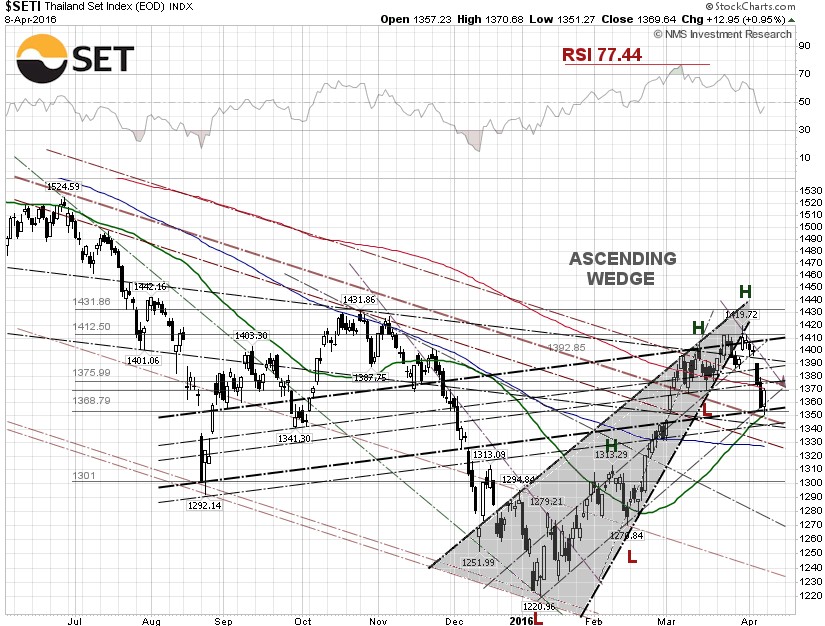

The SET took a 2.22% dive for the week, to close at 1,369.64 on Friday, but is still up 6.34% year-to-date. The USD/THB exchange rate was quoted at 35.102 baht per dollar on Friday, down 2.58% since the beginning of the year, while the CNY/THB has declined 2.50% year-to-date, to close at 5.4281 baht per yuan.

The Japanese yen surged against the Thai baht to an intraday low 3.0576 yen per baht on Thursday, with the THB/JPY exchange rate closing at 3.0817 yen per baht on Friday, down 7.72% year-to-date. Concerns about the weak global economy and that the Bank of Japan would push rates even deeper into negative territory has driven the USD/JPY exchange rate below the psychological support of 110 yen per dollar on Tuesday, a level not seen since November 2014.

The Thailand 10-year bond yield continued to move lower, as it closed at 1.665% on Friday, down 33.93% year-to-date, after plunging to a record low at 1.555% on Thursday. The yield spread between the Thailand 10-year bond and the benchmark U.S. 10-year Treasury Note, yielding at 1.717% on Friday, is –0.052 percentage points, meaning investors are willing not to be paid a premium to hold a Thailand 10-year bond over a U.S. 10-year Treasury Note, which is typically perceived as safer.

The yield spread between the Thailand benchmark interest rate, at 1.5%, and the Thailand 10-year bond is now at 0.165 percentage points. If the trend continues, the yield curve of the Thai bonds will be inverted.

The minutes of the March 15-16 U.S. Federal Open Market Committee meeting, released on Wednesday, revealed that many participants expressed concerns about appreciable downside risks of the global economic and financial situation, and that an April rate hike is unlikely. The European Central Bank (ECB) minutes released on Thursday, also signaled that several council members were willing to consider a deeper rate cut in March, and that future rate cuts also remain on the table. This was in contrast to ECB President Mario Draghi’s statement after the March monetary policy meeting that the central bank doesn't anticipate that it will be necessary to reduce rates further.

The WTI crude oil price closed up 8.27% for the week, at $39.66 per barrel on Friday, after closing down 7.48% last week. The Energy Information Administration (EIA) weekly inventory report showed a draw of 4.94 million barrels, compared to analysts’ expectations for a 3.2 million barrel build, according to Thomson Reuters. The larger-than-expected draw could be attributed to the shutdown due to “small leak” of the Keystone crude pipeline that delivers oil to Cushing, which contributed to about 480,000 barrels at the Oklahoma delivery point for U.S. crude futures.

Traders were encouraged by the EIA report, saying that weekly U.S. crude oil production fell for the tenth consecutive week to 9 million bpd (barrels per day) for the week ending April 1, 2016, the lowest level since November 14, 2014. Nonetheless, weekly U.S. crude oil output fell by just 6.35% from the peak level of 9.61 million bpd during the week ending June 6, 2015. Houston-based oilfield services company Baker Hughes Inc. reported on Friday that the U.S. oil rig count is now down to 354, a 77.8% drop from the peak number of 1,609 in October 2014. Obviously, there is no correlation between weekly crude oil production and the oil rig count.

From our technical viewpoint, the SET pulled back sharply this week and broke down the 200-day SMA (red line), as the technical indicators continue to deteriorate. The RSI topped out at 77.44 on March 7, the highest level in 20 months. The Moving Average Convergence Divergence (MACD) continues to run below the signal line. The SET did bounce off the 50-day SMA (green line), but the momentum is on the downside. The next technical supports are 1,340 and 1327.38, or 100-day SMA (blue line), if the SET continues to slide. The index could get some support on Monday next week from the surge in the WTI crude on Friday in New York.

|