|

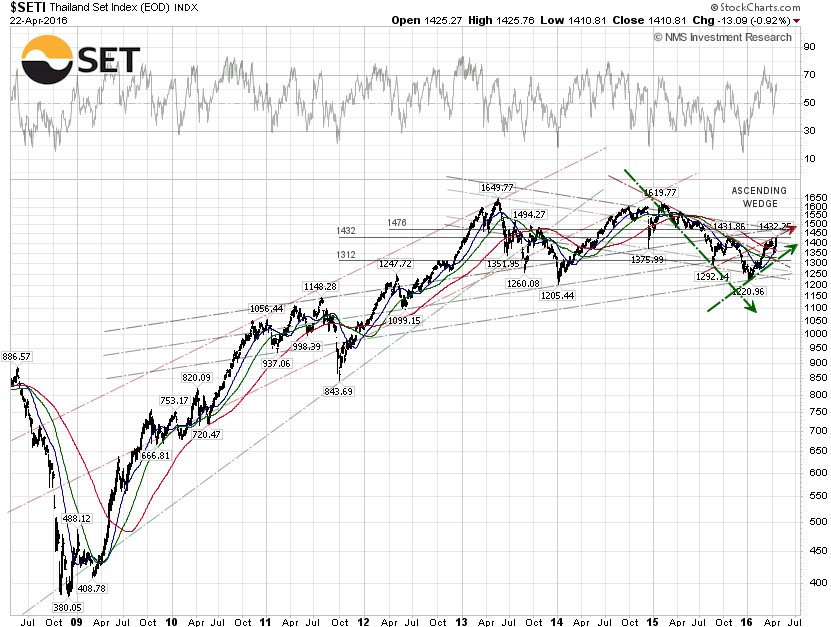

The SET jumped 1.83% for the week, after last week's three-day market holiday for Songkran, to close at 1,410.81 on Friday. The index is up 9.53% year-to-date. According to the SET data, the forward P/E ratio of SET is about 14.96 times, compared to the S&P 500 with a forward P/E ratio at 17.8 times. The USD/THB exchange rate was quoted at 35.07 baht per dollar on Friday, down 2.66% since the beginning of the year, while the CNY/THB has declined 3.04% year-to-date, to close at 5.398 baht per yuan.

The Thailand 10-year bond yield continued to move higher, as it closed at 1.82% on Friday, down 27.78% year-to-date, after plunging to a record low at 1.555% on April 7. The yield spread between the Thailand 10-year bond and the benchmark U.S. 10-year Treasury Note, yielding at 1.891% on Friday, is –0.071 percentage points, meaning investors are willing not to be paid a premium to hold a Thailand 10-year bond over a U.S. 10-year Treasury Note, which is typically perceived as safer.

Earnings reports from big Thai banks, including Bangkok Bank (SET:BBL) and Kasikornbank (SET:KBANK), were disappointing as net profits plunged 11.58% and 22.22%, respectively, due to rising non-performing loans (NPLs). There could be some headwinds for Thai banks, as the Moody’s ratings agency said earlier in April that the minimum lending rate (MLR) cut will hit the banks' net interest margins (NIMs). At the beginning of April, Siam Commercial Bank (SET:SCB) said it cut their MLR by 15 basis points, to 6.375%. An additional 10 basis points will follow, after other banks cut their minimum lending rate by 0.25 basis points.

The WTI crude oil spot price closed up another 4.79% for the week, at $43.75 per barrel on Friday, after closing up 5.27% last week. The Energy Information Administration (EIA) weekly U.S. oil inventory report on Wednesday showed a build of 2.1 million barrels in the week ending April 15, compared to analysts’ expectations for a 2.4 million barrel build. The American Petroleum Institute (API) inventory data on Tuesday showed a larger build of 3.1 million barrels.

Traders shrugged off the bearish reports from Doha and Kuwait. The Doha oil meeting between OPEC and non-OPEC producers ended last Sunday without a deal to freeze production. Iran, which did not attend the meeting, said it will crank up their oil production even more, as the sanctions are now lifted. The state-run Kuwait Petroleum Corp. said on Wednesday that the strike by thousands of Kuwait oil workers was over. In the company statement released on Thursday, it said the daily production in Kuwait, OPEC's fourth largest producer, is now at 2.9 million barrels per day (bpd), slightly off the normal capacity of 3.0 million bpd.

The EIA said the weekly U.S. crude oil production fell again for the twelfth consecutive week to 8.953 million bpd for the week ending April 15, 2016, the lowest level since November 14, 2014, at 9.004 million bpd. Weekly U.S. crude oil output, however, has fallen by just 6.84% from the peak level of 9.61 million bpd during the week ending June 6, 2015.

More bullish news for the oil market came from Houston-based oilfield services company Baker Hughes Inc., who said on Friday that the U.S. oil rig count is now down another 8 to 343, a 78.7% drop from the peak number of 1,609 in October 2014. Obviously, there is no correlation between weekly crude oil production and the oil rig count.

From our long-term technical viewpoint, the SET is now trading above the 200-day SMA and a bullish golden cross, or the 50-day and 200-day SMA crossover, may be emerging. The V-shaped bounce may be still at risk as long as the index stays under the 1,476 resistance level. The SET index and WTIC are positively correlated, with a 100-day correlation coefficient of 0.73, meaning the SET and WTIC move in the same direction, up or down. Hence, a breakout may require decoupling between the SET and WTIC. Although the current forward P/E ratio of the SET is about 14.96 times, be wary of chasing the market rally.

|