|

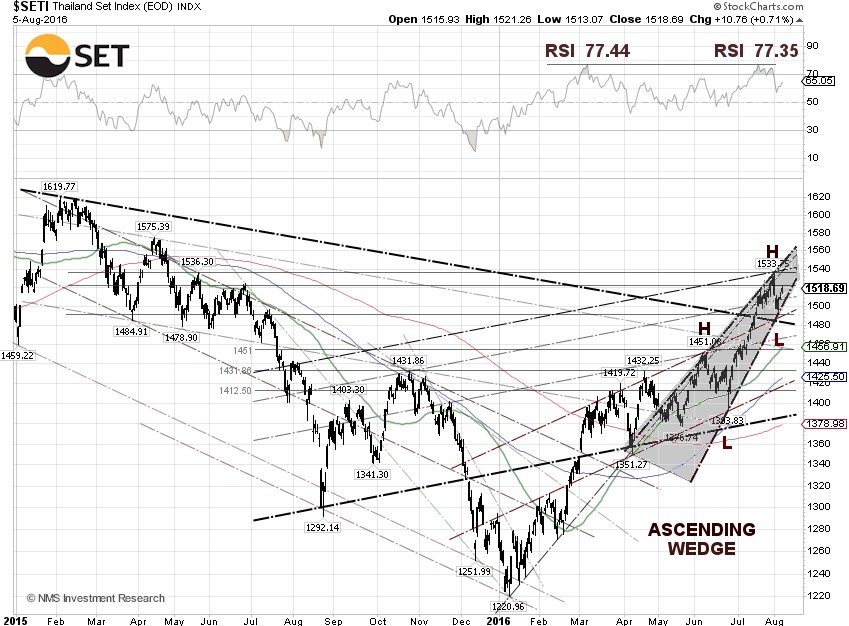

The SET pulled back to test the trendline support of the ascending wedge chart pattern and bounced off to close at 1,518.69 on Friday, down 0.35% for the week. The index traded along with crude oil prices, in tandem with other market moving economic events, including monetary policy decisions on interest rates by central banks. The market may have priced in a “YES” vote for the Thai Referendum to be held over the weekend, as the SET jumped 0.71% on Friday. Thai voters need to decide on August 7 whether or not to approve a draft constitution backed by the Junta government and whether or not the appointed senate should be allowed to join the lower house in selecting the prime minister.

There was good and bad news for the Japanese economy during the week. The good news was Japanese Prime Minister Shinzo Abe's cabinet approved a 13.5 trillion yen ($132 billion) government stimulus package on Tuesday that includes 7.5 trillion yen ($73 billion) in new spending to jump-start Japan’s sluggish economy. The Japanese yen surged 1.48% against the U.S. dollar as the market is skeptical whether the stimulus will work. The bad news was that most economists predict the stimulus will only modestly increase economic growth and could just pile up more debt without really boosting long-term growth.

Three key monetary policy decisions were announced by central banks this week. The Reserve Bank of Australia

(RBA) said on Tuesday that they cut its benchmark interest rate by 25 basis points to a record low of 1.50%, citing the global economy is continuing to grow at a lower-than-average pace, while business investment is declining significantly and inflation remains low.

Ahead of the Thai referendum, the Bank of Thailand

(BoT) kept its key interest rate unchanged on Wednesday, as expected, saying current monetary policy still supports the country's economic recovery and the referendum has no short-term impact on the economy. Some economists, including Krystal Tan at Capital Economics in Singapore, however, disagreed and expects growth to slow in the second half, according to the Bangkok Post.

As expected on Thursday, the Bank of England (BoE) cut interest rates for the first time since 2009, to 0.25% from 0.5%. The rates are now the lowest they have been in U.K. history. The BoE also said the bank is extending its asset-purchase facility to Ł435 billion from Ł375 billion to buy U.K. government bonds, which also includes a purchase of up to Ł10 billion of sterling-denominated corporate bonds, beginning in September. Skeptics believe that the BOE’s moves might not be enough to offset recessionary headwinds, however. Economists predict the U.K. economy will fall into recession in the second half of 2016, as uncertainty takes hold.

The

USD/THB exchange rate was quoted at 35.08 baht per dollar on Friday, up 0.89% for the week, while the

THB/JPY printed at 2.9022 yen per baht, down another 1.14% for the week. The

USD/THB technical support is at 34.80 baht per dollar, while the

THB/JPY technical resistance is at 3.07 yen per baht.

The Thailand 10-year bond yield tanked 3.35% for the week, to close at 2.02% on Friday. The yield spread between the Thailand 10-year bond and the benchmark U.S. 10-year Treasury Note, yielding at 1.59% on Friday, narrowed to 0.43 percentage points.

The WTI crude oil spot price inched up just $0.20 per barrel for the week, to close on Friday at $41.80 per barrel, while the Brent crude price jumped 2.54% for the week to close at $44.42 per barrel, following a volatile week. State-owned Saudi Arabian Oil Co. said on Sunday that it would cut Arab Light by $1.10 a barrel in September, below Asia’s regional benchmark, as the oil battle with Iran heats up.

Francisco Blanch, head of global commodity research at Bank of America Merrill Lynch, said on Bloomberg to buy this oil dip as he sees a rebound in oil prices by the end of the year. Global oil prices will average $57 a barrel in 2017, according to the median of at least 20 analyst estimates compiled by Bloomberg.

Crude oil prices got a boost by the weekly report from the Energy Information Administration (EIA) showing a larger-than-expected decline in U.S. gasoline inventory and reduction in U.S. crude oil production.

The EIA weekly U.S. oil inventory report on Wednesday showed an increase of 1.4 million barrels to 522.5 million barrels, excluding strategic inventories, in the week ending July 29, compared to S&P Global Platts analysts’ expectations for a drawdown of 1.9 million barrels. The American Petroleum Institute (API) inventory data on Tuesday showed a U.S. crude inventory draw of 1.3 million barrels for the week.

There was a large decline last week in U.S. gasoline supplies of 3.3 million barrels, while distillate stockpiles, including jet fuel, diesel fuel and heating oil, increased by 1.2 million barrels, according to the EIA. Analysts were expecting a drawdown of 400,000 barrels of gasoline stocks and a decline of 500,000 barrels for distillates.

Separately, the EIA said the weekly U.S. crude oil production dropped by 55,000 barrels per day (bpd) for the week ending July 29, 2016, to 8.46 million bpd. Weekly U.S. crude oil output has fallen about 11.97% from the peak level of 9.61 million bpd during the week ending June 6, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count was up another 7 from the previous week, to 381, compared to 316, when the rig count hit the low on June 6, 2016.

The Labor Department said on Friday, after the SET close, that U.S. nonfarm payrolls increased by seasonally adjusted 255,000 jobs last month, beating Wall Street economists' forecast of an 180,000 gain. If not seasonally adjusted, the nonfarm payrolls were 1.03 million jobs lost for July. The probability of a 25 basis point rate hike at the next FOMC meeting on September 21 jumped 9 percentage points from the previous day to 18.0%, while the probability of a no rate hike dropped to 82.0% from 91.0%, according to data from the CME Group as of August 5. The crude oil and the SET downside risks increase, as a Fed rate hike threat looms larger. |