|

The SET inched up 1.15% for the week, to close at 1509.13 on Friday, after Thai big banks, including Bangkok Bank

(SET:BBL), Krung Thai Bank (SET:KTB) and Kasikornbank (SET:KBANK), reported mixed quarterly earnings on Thursday, while shares of energy stocks, including PTT plc

(SET:PTT) and PTT Exploration and Production (SET:PTTEP), rose 4.59% and 1.8%, respectively, for the week despite falling crude oil prices. The SET index has decoupled from Brent crude prices since June 24, after the Brexit vote, so it might not matter that crude oil prices are heading south, until it matters.

The WTI crude oil spot price tumbled 4.52% for the week to close on Friday at $44.19 per barrel, while the Brent crude price took a 4.26% nosedive to close at $46.06 per barrel, following a bearish report from the Energy Information Administration

(EIA) showing that U.S. demand for gasoline is weak, while OPEC and Russia continue to extend the bear market for crude oil. About 50% of total U.S. liquid fuels consumption is gasoline.

The EIA weekly U.S. oil inventory report on Wednesday showed a decline of 2.34 million barrels to 519.5 million barrels, excluding strategic inventories, in the week ending July 15, compared to S&P Global Platts analysts’ expectations for a drawdown of 1.25 million barrels. The American Petroleum Institute (API) inventory data on Tuesday showed a U.S. crude inventory draw of 2.3 million barrels for the week.

There was another large build last week in U.S. gasoline supplies of 900,000 barrels, while distillate stockpiles, including jet fuel, diesel fuel and heating oil, dropped 200,000 barrels, according to the

EIA. Analysts were expecting the gasoline stocks to remain unchanged and a rise of 700,000 barrels for distillates.

Separately, the EIA said the weekly U.S. crude oil production decreased by 9,000 barrels per day (bpd) for the week ending July 15, 2016, to 8.494 million bpd. Weekly U.S. crude oil output has fallen about 11.61% from the peak level of 9.61 million bpd during the week ending June 6, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count was up another 14 from the previous week, to 371, compared to 316, when the rig count hit the low on June 6.

There are still no discussions between OPEC and Russia about oil output after a failed attempt to jointly maintain production levels earlier this year. OPEC’s monthly report stated that Saudi Arabia’s crude oil production rose by 66,500 bpd, to 10.3 million bpd in June 2016, compared to the previous month, while Iran’s crude oil production rose by 77,800 bpd, to 3.64 million bpd in June 2016, compared to May 2016. Iran almost doubled its exports since early 2016. Russia’s crude oil production also rose to 10.8 million bpd in June 2016, compared to the previous month, according to the Russian Energy Ministry.

The dollar bulls took the U.S. Dollar index to a four-month high at 97.516 on Friday, up 0.99% for the week, after the July preliminary U.S. Markit Manufacturing PMI index came in at 52.9, much better than the analyst consensus estimate of 51.6, and news of the Munich attack that killed at least 9 people. Surprisingly, the USD/THB exchange rate was quoted at 34.975 baht per dollar on Friday, unchanged for the week, while the THB/JPY printed at 3.0329 yen per baht, up 1.21% for the week. The USD/THB technical support is at 34.80 baht per dollar, while the THB/JPY technical resistance is at 3.07 yen per baht.

The Thailand 10-year bond yield jumped another 5.13% for the week, to close at 2.05% on Friday. The yield spread between the Thailand 10-year bond and the benchmark U.S. 10-year Treasury Note, yielding at 1.566% on Friday, widened to 0.484 percentage points. The global bond markets continued to be rattled from global uncertainty, as the 10-year Japanese government bond (JGB) yield stayed at negative 0.224% at the close on Friday, while the 10-year German bund yield is back to negative 0.023%.

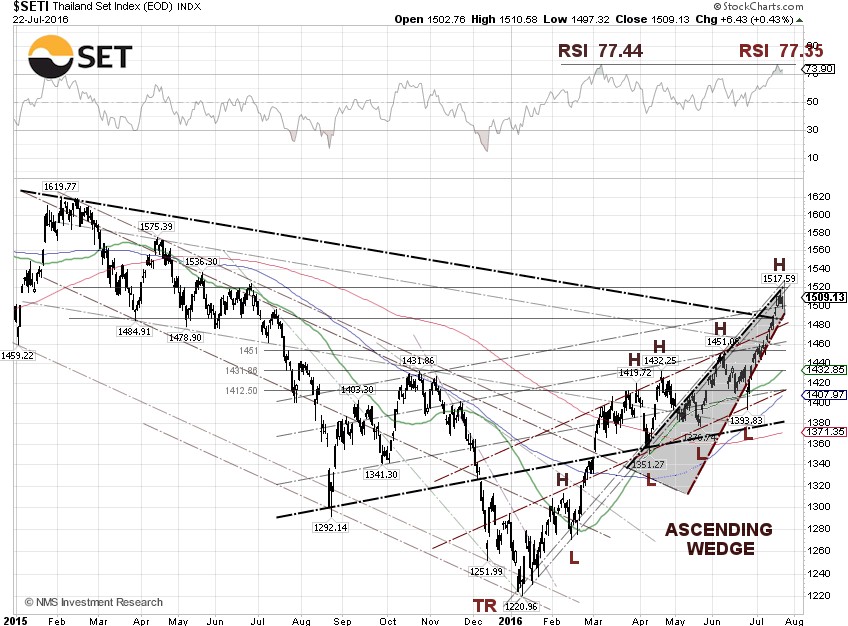

Technically, the SET pulled back to about the 1,500 level. The index could drop to the 1,480 level and should bounce from there if the breakout wasn’t a head fake. The bulls may still have control over the market, indicated by a higher high uptrend chart pattern. Nonetheless, the SET is entering overbought territory (RSI=77.35) and a RSI double top has emerged. While the MACD line still stays above the signal line, the upside momentum begins to weaken.

The probability of a 25 basis point rate hike at the next FOMC meeting on July 27 inched up to 2.4%, while the probability of a no rate hike dropped to 97.6%, according to data from the CME Group as of July 22. The U.S. Bureau of Economic Analysis will release the second-quarter GDP (advance estimate) on July 29. The current U.S. GDP forecast by the Federal Reserve Bank of New York is 2.2%, the lowest second-quarter GDP since 2014. |