|

The SET lost 0.75% for the week, to close at 1,382.96 on Friday, but up 7.37% for the year. The USD/THB exchange rate was quoted at 34.866 baht per dollar on Friday, down 3.23% since the beginning of the year, while the CNY/THB has declined 3.17% year-to-date, to close at 5.3909 baht per yuan. The USD/THB traded as low as 34.70 baht per dollar on Thursday, as FX currency traders were piling onto the Thai baht, ahead of the BoT monetary meeting on March 23.

The Thailand 10-year bond yield was 1.78% at the close on Friday, down 9.64% for the week and 29.37% year-to-date. The yield spread between the Thailand 10-year bond and the benchmark U.S. 10-year Treasury Note, yielding at 1.878% on Friday, is –0.098 percentage points, meaning investors are willing not to be paid a premium to hold a Thailand 10-year bond over a U.S. 10-year Treasury Note, which is typically perceived as safer.

The strong baht could be supported by comments from Bank of Thailand (BoT) Governor Veerathai Santiprabhob, who told reporters on March 8 that fiscal policy is a more effective tool than monetary policy, hinting to not expect a rate cut from the BoT anytime soon. The BoT also said that the bank plans to lower its 2016 economic growth forecast again, from the 3.5% stated in December, due to increased downside risks, according to Bangkok Post.

In December, the BoT cut its 2016 economic growth estimate to 3.5% from 3.7% as the bank saw no growth in exports. The central bank will review its economic forecasts at the monetary meeting on March 23 and will release the results by March 31. On Friday, ahead of the BoT’s announcement, TMB Bank Analytics already cut Thailand's economic growth forecast to 2.8% for 2016, citing continuation of exports contraction and constrained private consumption by high household debt, according to Bangkok Post.

Earlier in the week, the Bank of Japan (BOJ) said on Tuesday that they would keep its key interest rate unchanged, but downgraded their economic outlook. That means the probability increases for more asset purchases and rate cuts deeper into negative territory at the next policy meeting in April. The BOJ is currently buying 8 to 12 trillion yen of JGBs per month, more than issued by the Ministry of Finance. In late January, the bank applied a negative 0.1% interest on excess reserves (IOER) of financial institutions placed at the BOJ, forcing the banks to extend loans to businesses or to weaker lenders and hence, reducing borrowing costs and driving demand for loans.

As expected on Wednesday, following its two-day FOMC policy meeting, the U.S. Federal Reserve kept the key interest rate unchanged at between 0.25% and 0.5% and hinted that they may make only two rate increases by the end of the year, half the number that was forecasted at its December meeting. The Fed also trimmed its economic growth outlook for the year to 2.2%, from the previous forecast of 2.4% growth, and its forecast for inflation to 1.2% from 1.6%.

Fed Chair Janet Yellen sounded more dovish this time, compared to the December FOMC meeting press conference when she said, “Caution is appropriate,”. “Since the turn of the year, concerns about global economic prospects have led to increased market volatility and tighter financial conditions in the United States,”, added Yellen.

The WTI crude oil price surged another 6.88% for the week, after headline news said that OPEC and non-OPEC producers will meet in Doha on April 17 to discuss a deal to freeze output. So far, Iran has declined to participate. Jeffrey Currie, Goldman Sachs' head of commodities research, issued a report last Tuesday saying that the recent rally in commodities is just a "mirage". Crude oil April contracts (CLJ6) will expire on Monday. Volatility due to the rollover from the April to the May contracts (CLK6) may cause price swings in either direction.

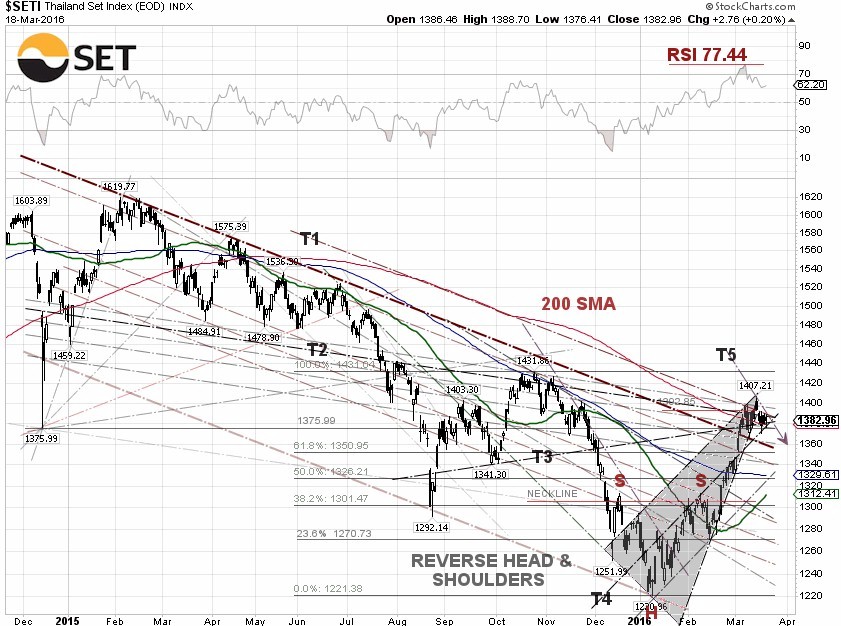

From our technical viewpoint, the SET still managed to close above the 200-day moving average. The RSI registered at 77.44 on March 7, the highest level in 20 months. The Moving Average Convergence Divergence (MACD) began to cross below the signal line, meaning it may be time to sell. Nonetheless, if market momentum and the Thai baht remain strong, the SET could bounce back and stay in overbought territory for a while. Money is still pouring in from overseas, as the foreign investor’s net buys are 15.4 billion baht since the beginning of March, according to the SET’s data. The next support level is between 1,358 and 1,350.95, if the SET continues to pull back.

|