|

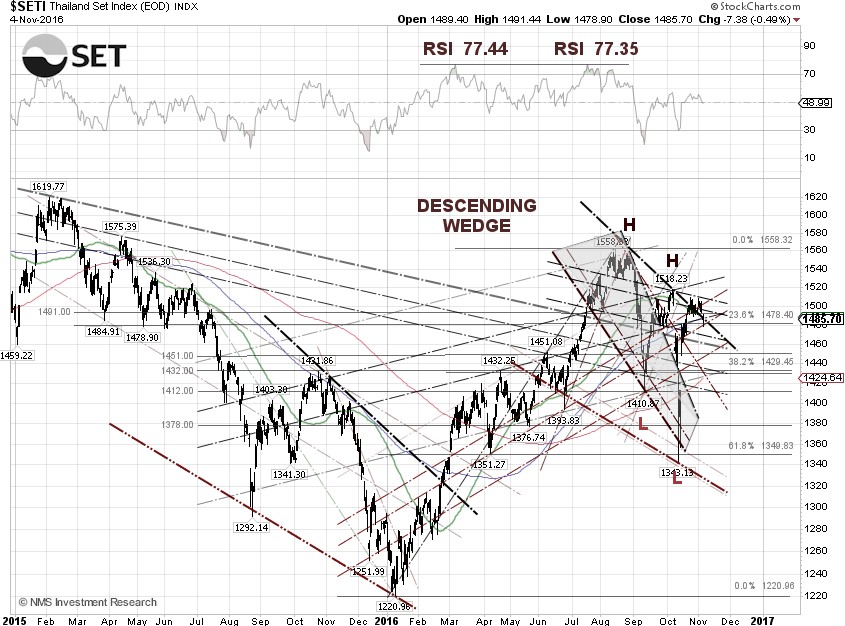

The SET index pulled back 0.59% for the week to close at 1,485.70 on Friday, after the index made a double top reversal at 1,507, with the Thai baht stabilizing at around 35 baht per dollar. The SET broke down the 23.6% Fibonacci retracement at 1,478.40 and bounced off the trendline support, as algorithmic trading continues to dominate the market.

The USD/THB currency pair dipped another 0.23% this week to close at 34.94 baht per dollar on Friday, while the U.S. dollar index tumbled 1.36%, to close at 97.088 on Friday. Foreign investor selling is accelerating at a rate of about 2.5 times higher than that in October, as net sells by foreign investors surged to 5.82 billion baht month-to-date.

The yield of Thailand 10-year government bonds inched up 0.90% for the week, to close at 2.19% on Friday. The yield spread between the Thailand 10-year bond and the benchmark U.S. 10-year Treasury Note, yielding at 1.778% on Friday, widened to 0.412 percentage points.

The widely traded Airports of Thailand PCL (SET:AOT) stock tumbled 4.18% for the week, to 367.00 baht per share on Friday, as concerns rise over air travel heading into the November and December peak season. Shares of PTT PCL

(SET:PTT) and PTT Exploration and Production PCL (SET:PTTEP) were down 3.45% and 1.2% for the week, along with crude oil prices.

The WTI crude price tumbled another 9.51% this week, to close at $44.07 per barrel on Friday, while the Brent crude spot price tanked 8.51% to close at $46.36 per barrel, after the EIA U.S. oil inventory report showed its largest weekly inventory build, a 34-year record high. Crude prices continued to move lower earlier Friday after Reuters reported that Saudi Arabia threatened to raise output if other members didn’t agree to cuts.

Technical talks between OPEC member top officials, at the OPEC Vienna headquarters on October 28 and 29, went nowhere and ended without reaching any deals. Ministers from the group will meet at the OPEC summit in Vienna on November 30 to finalize the agreement on an oil output freeze. According to Bloomberg, Goldman Sachs Group Inc. sees little probability of an agreement at the meeting, while Bank of America Merrill Lynch and Citigroup Inc. say an accord is likely.

The EIA weekly U.S. oil inventory report on Wednesday showed that domestic crude supplies increased by 14.4 million barrels to 482.6 million barrels, excluding the Strategic Petroleum Reserve, in the week ending October 28, compared to S&P Global Platts analysts’ expectations for a rise of 1.9 million barrels. The American Petroleum Institute (API) inventory data on Tuesday showed a U.S. crude inventory increase of 9.3 million barrels.

Separately, the EIA said the weekly U.S. crude oil production increased by 18,000 barrels per day (bpd) for the week ending October 28, to 8.522 million bpd. Weekly U.S. crude oil output has fallen about 11.32% from the peak level of 9.61 million bpd during the week ending June 5, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count rose by 9 to 450, compared to 316, when the rig count hit the low on June 6, 2016.

The WTI crude broke down the 50.0% Fibonacci retracement level at $44.32 per barrel on Friday and bounced off the 200-day SMA. The crude price could test the 38.2% Fibonacci retracement level at $40.00 per barrel next week if there is still no consensus on an output freeze from OPEC and Russia before the Doha meeting on November17.

|