|

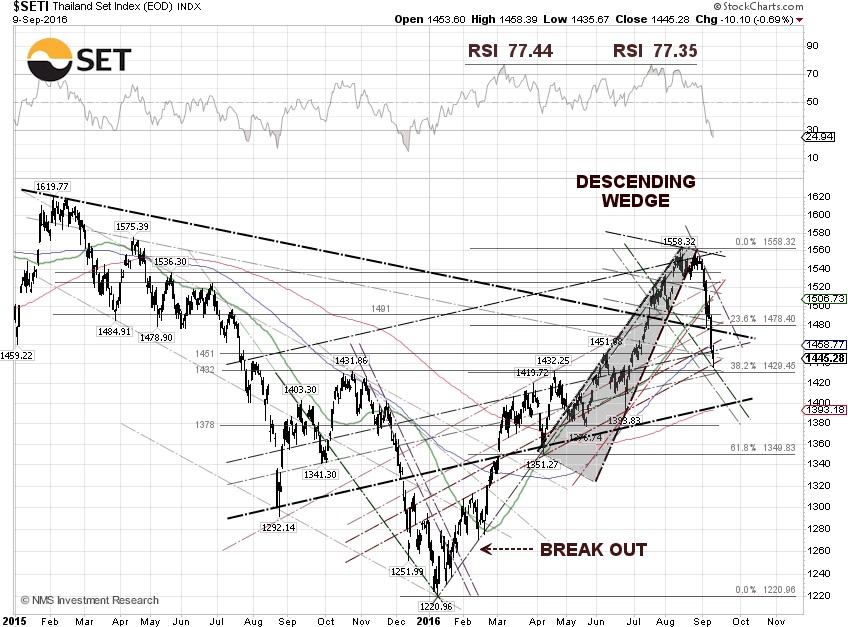

The SET index sold off for the second week in the row to close at 1,445.28 on Friday, down 5.1% for the week, as Thai institutions and proprietary trading firms continued dumping shares, according to the SET market data. The Thai market might have been spooked by unexpected baht depreciation, after the

USD/THB bounced off the 34.50 baht level. The currency pair has been trying, but failed, to break down the 34.50 baht support level since mid-August.

The SET index could get another jolt on Monday, following a big sell-off in the U.S. on Friday. U.S. markets were caught by surprise with the Fed's hawkish tone, despite weak U.S. economic data, after a number of officials came out during the week and expressed their opinions about the case for a rate hike before the Fed's blackout period begins on Tuesday.

A descending wedge chart pattern has now emerged for the SET index, where it can get some support. Nonetheless, if the key technical support at 1,429.35, or 32.8% Fibonacci

retracement, can’t hold and the baht continues to depreciate further, the index could be heading for a 1,400 level retest. According to a Bloomberg survey, the baht is expected to weaken to 35.4 baht per dollar by year-end, meaning one could see the year-end target for the SET index to be between 1,380 and 1,400.

The USD/THB exchange rate was quoted at 34.85 baht per dollar on Friday, up 0.64% for the week, while the

THB/JPY currency pair tanked 1.88% for the week to close at 2.9468 yen per

baht. The USD/THB broke out the technical resistance at 34.74 baht per dollar, or 23.6% Fibonacci

retracement, and the next stop could be at 35.0 baht per dollar.

The yield of Thailand 10-year government bond tumbled 5.19% for the week, to close at 2.19% on Friday. The yield spread between the Thailand 10-year bond and the benchmark U.S. 10-year Treasury Note, yielding at 1.675% on Friday, narrowed to 0.515 percentage points.

Shares of PTT Exploration and Production PCL (SET:PTTEP) and PTT PCL (SET:PTT), held up relatively well compared to the SET index, down just 0.31% and 2.99%, respectively for the week, as crude prices rebounded. The WTI crude spot price surged 3.24% for the week, to close on Friday at $45.88 per barrel, while Brent crude futures for November 16 jumped 2.52% to close at $48.01 per barrel, after the state-owned Russian news agency TASS reported on Monday that Saudi Arabia and Russia signed an agreement aimed at stabilizing the oil market.

A bullish weekly report from the Energy Information Administration (EIA) on Thursday, showing the second largest drop in U.S. crude oil inventory on record, sent the WTI crude price shooting up over 4%. The oil rally, however, faded on Friday after traders realized that the much larger-than-expected decline was probably a one-time event due to bad weather.

The EIA weekly U.S. oil inventory report on Thursday showed a decrease of 14.5 million barrels to 511.4 million barrels, excluding the Strategic Petroleum Reserve, in the week ending September 2, compared to S&P Global Platts analysts’ expectations for a rise of 425,000 barrels. The American Petroleum Institute (API) inventory data on Wednesday showed a U.S. crude inventory drawdown of 12.1 million.

Oil analysts attributed the big decline in crude inventory to Hurricane Hermine, that impacted operations along the U.S. Gulf Coast. The storm caused production to be taken offline and also contributed to Gulf Coast crude imports to drop as ships delayed offloading cargo in Texas and Louisiana.

Separately, the EIA said the weekly U.S. crude oil production decreased by 30,000 barrels per day (bpd) for the week ending September 2, 2016, to 8.458 million bpd. Weekly U.S. crude oil output has fallen about 11.99% from the peak level of 9.61 million bpd during the week ending June 5, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count rose by 7 to 414, compared to 316, when the rig count hit the low on June 6, 2016. |