|

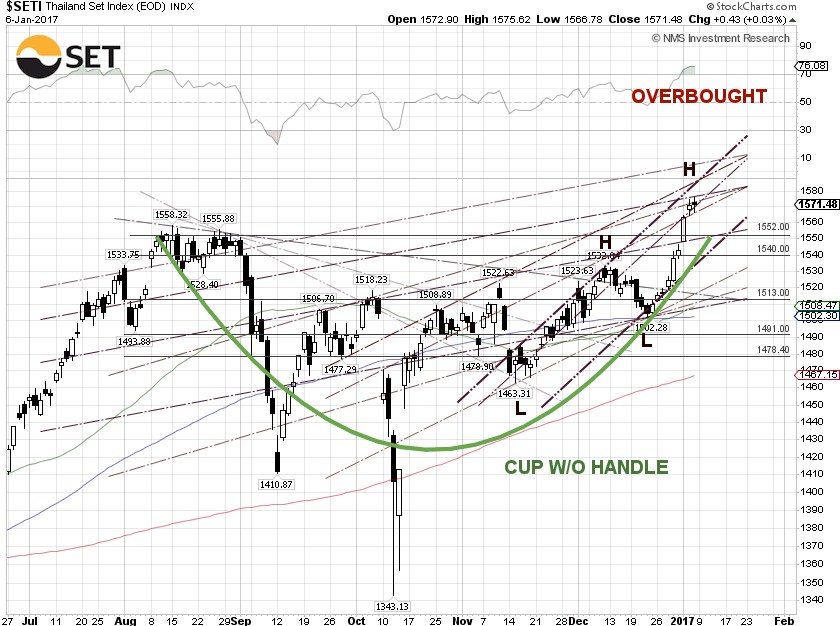

The SET index surged another 1.85% for the week, to close on Friday at 1,571.48, led by big cap energy stocks, including PTT PCL (SET:PTT) and PTT Exploration and Production PCL (SET:PTTEP), up 4.57% and 2.34%, respectively, despite that the Brent crude spot price remained practically unchanged, up just $0.05 for the week. The August high of 1,558.32 was taken out and the next head resistance will be 1,600. The RSI signals the index is overbought, but the MACD momentum indicator is still bullish. It will not be a surprise to see the SET index make a new all-time high, which currently stands at 1,643.43 on May 21, 2013, before any significant pullback happens.

HSBC raised its forecast for Thailand's 2017 economic growth to 3.2% from 2.8%, according to the Bangkok Post. The bank cited an increased outlook, as public investment remains the main growth driver, and a rebound in tourism. In late December, the Bank of Thailand maintained its economic growth forecasts for this year and next at 3.2%. Governor Veerathai Santiprabhob told the media after the rate decision that, "There are some positive factors that could enable the country's GDP to grow by more than 3.2%, … If the new U.S. president is able to deliver policies that help the economy grow better than expected, it might benefit Thailand through exports.", according to the Bangkok Post.

The USD/THB continues to pull back and closed on Friday at 35.74 baht per dollar, down 0.23% for the week. The U.S. Dollar index (DXY), a measure of the U.S. dollar value relative to a basket of foreign currencies, closed at 102.27, practically unchanged for the week, after the People's Bank of China (PBoC) began cracking down on offshore yuan speculators, sending the yuan soaring against the U.S. dollar on Thursday and Friday. The yield of Thailand 10-year government bonds remained unchanged for the week, to close at 2.70% on Friday. The yield spread between the Thailand 10-year bond and the benchmark U.S. 10-year Treasury Note, yielding at 2.421% on Friday, widened to 0.279 percentage points.

The WTI crude price gained 0.50% for the week to close at $53.99 per barrel on Friday, while the Brent crude spot price remained practically unchanged, up $0.05 for the week, to close at $56.87 per barrel, despite a sharp drawdown in inventory. Oil companies use tax mitigation strategies at the year-end by keeping their crude cargo offshore rather than bringing them onshore. The WTI crude price continues trading around the $53.96 resistance level, or 76.4% Fibonacci retracement, as the market is in a wait-and-see mode for the OPEC and non-OPEC production cut of 1.8 million barrels per day (bpd), beginning in January 2017.

The EIA weekly U.S. oil inventory report on Thursday showed that domestic crude supplies decreased by 7.1 million barrels to 479.0 million barrels, excluding the Strategic Petroleum Reserve, in the week ending December 30, compared to S&P Global Platts forecast for a stockpile decline of 1.7 million barrels. The American Petroleum Institute (API) inventory data on Wednesday showed a U.S. crude inventory decrease of 7.4 million barrels.

Separately, the EIA said the weekly U.S. crude oil production dropped 4,000 bpd for the week ending December 30, to 8.766 million bpd. Weekly U.S. crude oil output has fallen about 8.74% from the peak level of 9.61 million bpd during the week ending June 5, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count inched up another 4 to 529, compared to 316, when the rig count hit the low on June 6, 2016. |