|

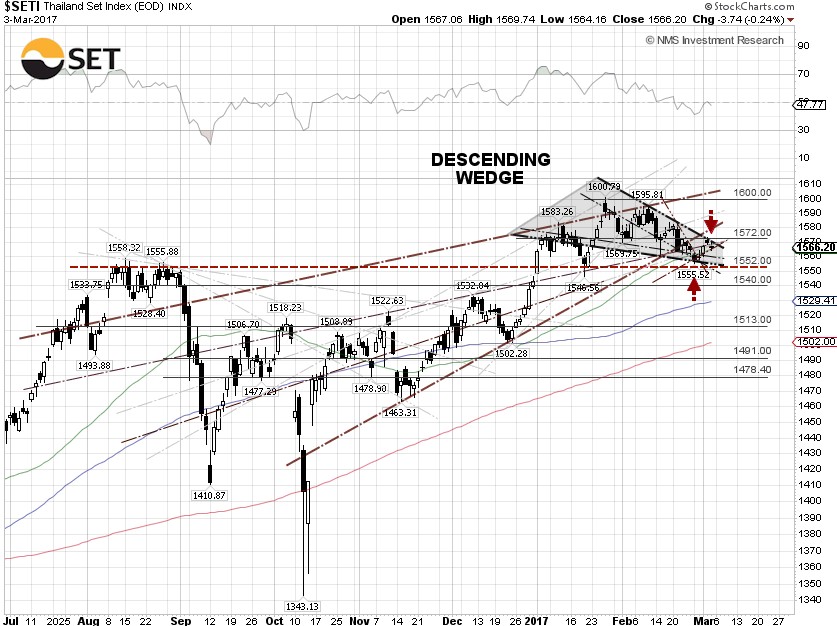

The SET index rebounded from the sell-off last week and gained 0.10% this week, to close on Friday at 1,566.20, while retail and foreign investors continued selling on concerns about an interest rate hikes at the March 14-15 FOMC meeting. The current probability of a quarter percentage point hike, in the target of the Federal funds rate to 75 and 100 basis points, is 79.7%, based on CME Group 30-Day Fed Fund futures prices. The odds that the Fed rate hike cycles will end up badly are also high. According to David Rosenberg at Gluskin Sheff, the U.S. economy landed in recession 10 out of 13 times the Fed hiked rates since WWII.

Investors were selling some currency sensitive stocks, including Airports of Thailand PCL (SET:AOT), Central Plaza Hotel PCL (SET:CENTEL) and Bangkok Dusit Medical Services PCL (SET:BDMS), which were down 1.29%, 2.1% and 2.44%, respectively, for the week. The SET index continues to look bearish, as it is still unable to break out the 1,572 resistance level.

The USD/THB exchange rate inched 0.69% higher for the week, to close on Friday at 35.079 baht per dollar, appreciating 2.08% year-to-date against the U.S. dollar. The Bank of Thailand, or BOT, said last week that they are tracking short-term capital inflows which are causing the baht currency to strengthen but the bank is not worried at this point, according to The Bangkok Post.

The yield of Thailand 10-year government bonds closed up 1.85% for the week, at 2.75% on Friday. The yield spread between the Thailand 10-year bond and the benchmark U.S. 10-year Treasury Note, yielding at 2.482% on Friday, narrowed to 0.268 percentage points. The spot gold price dropped 2.53% for the week, to close at U.S. $1,226.50 per ounce on Friday, while the Japanese yen was down 1.66% against the U.S. dollar.

The U.S. Dollar index (DXY), essentially the USD/EUR exchange rate, retested 102.16, or the 61.8% Fibonacci retracement level, on Thursday, before pulling back to close on Friday at 101.38, up 0.29% for the week, despite that New York Fed President William Dudley said on Wednesday that the case for raising U.S. interest rates has become "a lot more compelling" since the November election, given rising confidence and expectations for fiscal stimulus.

In fact, Trump’s “Phenomenal” Tax Bill could be pushed back until August, while President Trump and GOP leaders are reportedly considering punting on a major infrastructure package until 2018, as Congress wrestles with a crammed legislative calendar this year, according to The Hill.

The Federal Reserve Bank of Atlanta revised its U.S. first quarter GDP 2017 on Wednesday, to 1.8% from 2.5%, citing weak real personal consumption expenditures, or PCE, after the U.S. Bureau of Economic Analysis said the core PCE index rose by 1.74% year-over-year, below expectations of 1.8%. The currency and bond markets seem to be ignoring the fact that the core PCE index, the preferred inflation indicator for the Federal Reserve, is still well below the Fed target of 2%. The median and central tendency PCE inflation projections are 1.9% and 1.7 - 2.0%, respectively for 2017, according to the Fed economic projections at the December FOMC meeting.

The Fed may be pinning its hopes on the nonfarm payroll report due on March 10. At this point, we are not making a big bet on the U.S. dollar, as the DXY is forming a bearish head-and-shoulders chart pattern. The DXY could plunge if the Fed decides not to raise the Fed funds rate at the March FOMC meeting.

The Commerce Ministry of Thailand said on Monday that exports rose 8.8% year-on-year in January to US$17.1 billion (596 billion baht), boosted by recovering world trade, a gradual recovery of the global economy and higher oil and gold prices, according to the Bangkok Post. Exports, excluding oil and gold, were up 4.8%, while January imports rose 5.17% to $16.2 billion, resulting in a trade surplus of $826 million.

The WTI crude spot price declined 1.22% for the week, closing at $53.33 per barrel on Friday, while the Brent crude spot price also lost 2.26% for the week to close at $55.06 per barrel, after Reuters reported on Thursday that Russian is in weak compliance with the OPEC/non-OPEC crude oil production cut agreement. According to Reuters, Russia may have cut about 100,000 barrels per day, or bpd, so far, or only about a third of the levels pledged to cut under an agreement with OPEC. Speculative long positions in WTI crude oil futures contracts held by money managers totaled 429,168 contracts as of February 28, 2017, a decline of 19,678 contracts, according to data from the U.S. Commodity Futures Trading Commission, or CFTC.

The EIA weekly U.S. oil inventory report on Wednesday showed that domestic crude supplies increased by another 1.501 million barrels to a record 520.184 million barrels, excluding the Strategic Petroleum Reserve, in the week ending February 24, compared to the S&P Global Platts forecast for a stockpile increase of 2.1 million barrels. The American Petroleum Institute, or API, inventory data on Tuesday showed a U.S. crude inventory increase of 2.5 million barrels.

Separately, the EIA said the weekly U.S. crude oil production decreased 31,000 bpd, for the week ending February 24, to 9.032 million bpd. U.S. crude oil output increased 56,000 bpd to an average of 8.997 million bpd in February, compared to a January average of 8.942 million bpd. Output has fallen about 6.28% from the peak level of 9.60 million bpd in June 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count rose another 7 to 609, compared to 316, when the rig count hit the low on June 6, 2016.

|