|

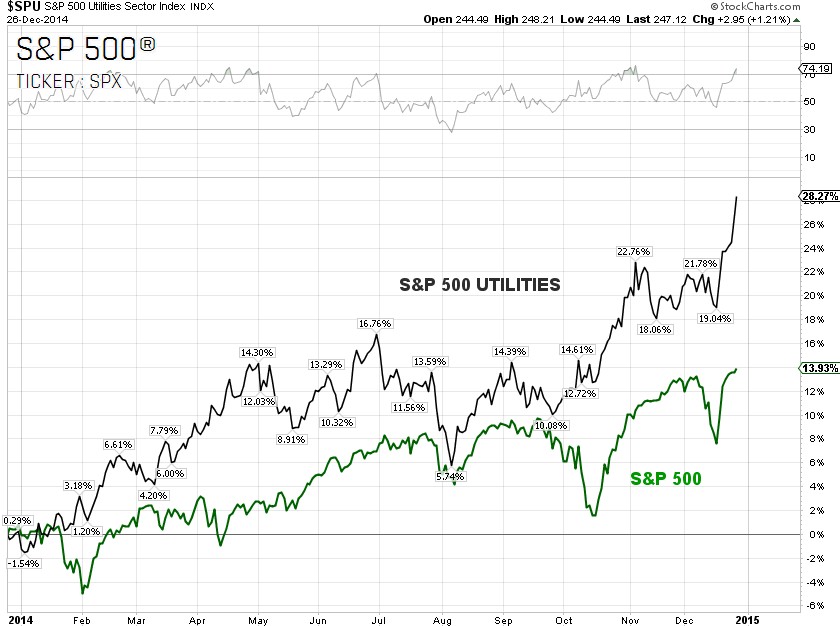

The hedge fund managers decided to take money out of the other S&P sectors and piled into the lower-risk, dividend paying utilities and consumer staples sectors. The S&P healthcare sector sold off over 4% for the week as “fear” from the news reports that Express Scripts [NASDAQ:ESRX], the largest manager of prescription drug plans for U.S. employers, is taking an increasingly aggressive stance in price negotiations with pharmaceutical companies.

These types of Wall Street “rumor and fear” tactics are commonly used as excuses to sell or short the stocks. So, there was actually no “new” news, per say.

I’m woundering what the hedge fund managers will do next week as the S&P utilities sector is now overbought and it is a short trading week. In the past two weeks, hedge fund managers were “bottom fishing” in the energy sectors but failed miserably.

According to the Barclay Hedge Fund Index, which measures the average return of all hedge funds (excepting Funds of Funds) in the Barclay database, the average year-to-date returns for hedge funds, until the end of November, is only 3.4%.

Just a reminder, a hedge fund uses a “2-20” fee structure, meaning the hedge fund managers charge a flat 2% of total asset value as a management fee and an additional 20% of any profits earned.

On Tuesday, the U.S. Bureau of Economic Analysis (BEA), the Commerce Department, revised its third-quarter real GDP from 3.9% reported last month to 5%, citing stronger consumer and business spending than it had previously factored in. Third-quarter inventories were revised higher, meaning there could be negative impact on the fourth-quarter real GDP, which is calculated on a quarter-to-quarter annualized basis.

One may want to pay attention to an increase in the third-quarter corporate profits adjusted for inventory valuation and capital consumption of U.S. $64.5 billion, or 3.1% quarter-to-quarter, compared with an increase of $164.1 billion or 8.4% quarter-to-quarter in second-quarter. The deceleration in the corporate profits of 60.7% quarter-to-quarter may be attributed to the strong U.S. dollar and decline in profit margins. Over the last 12 months, corporate profits rose just 1.4%.

The third estimate of the U.S. real GDP beat economists’ forecasts, polled by Reuters of 4.3%. The fourth-quarter real GDP estimates are currently at 2.5%. Standard & Poors just upwardly revised its full-year 2015 real U.S. GDP forecast to 3.1% from 3.0%, citing the decline in oil prices that may help boost consumer spending.

Plunging oil prices are prompting energy companies to cut capex and investment spending, by 25% or more, in 2015. The spending cuts and potential job losses in the U.S. energy related sectors may not yet be factored into most of real GDP estimates by economists.

The U.S. Commerce Department also reported that orders for non-defense, or core capital goods, were unchanged in November. Economists were expecting an increase of 1.5%. October’s numbers didn’t score much better as the orders for core capital goods unexpectedly fell 1.3%, missing economists’ forecasts of an increase of 1.0%. The bad reading of core capital goods orders in October and November could draft down the fourth-quarter real GDP.

As the Wall Street Journal described the mixed economic data on Tuesday, “The market got two early Christmas presents this morning – one a shiny new bike, the other a lump of coal.” Nonetheless, the U.S. 10-Year Treasury yield surged 4.6% and closed on Friday at 2.25%. The U.S. dollar index printed at 90.40 on Tuesday, the highest since March 2006. The U.S. dollar index has run up over 13% since the beginning of July this year.

On Friday, WTI crude oil closed on the Chicago Mercantile Exchange (CME) at U.S. $55.14 per barrel, a drop of 4.55% from last week’s close despite a report from the Libyan state-run National Oil Corp that fighting there has cut output to 352,000 barrels a day, or about half of November's average.

The crude oil market seemed to ignore supply interruptions in Libya and focused on the recently strengthened U.S. dollar index and the crude inventory buildup in the United States. On Wednesday, the U.S. Energy Information Administration (EIA) weekly report showed a 7.3 million barrel build in U.S. commercial crude inventories, the highest December level on record.The total U.S. commercial crude inventory now stands at 387.2 million barrels, well above the upper limit of the five-year range for this time of year.

One more sign that the crude oil price could head lower in the coming week is the CBOE Crude Oil Volatility Index (OVX). OVX, which spiked to a 52-week high of 58.43 during last week’s trading, printed at 54.68, or virtually unchanged from Friday’s close a week ago at 54.84. Just a reminder, high OVX readings mean traders see significant risks that crude oil prices will move sharply lower.

The next shoe to drop may be natural gas as Henry Hub natural gas futures, which are traded on the CME, fell below U.S. $3.00 per million British thermal units (mm Btu) this week for the first time since September 2012. The price of natural gas could still be under pressure as there is a 55% chance that the weather in the U.S. Midwest will be normal, or warmer than normal, in January and February 2015.

The next key technical support is U.S. $2.62 mm Btu.

S&P 500 TICKER: SPX 13.01%

YTD

Outperforming Sectors: Utilities 28.80% YTD, Healthcare 24.71%

YTD, Information technology 21.55% YTD, Consumer staples 15.73% YTD and Financials 14.45%

YTD.

Underperforming Sectors: Industrials 9.49% YTD, Consumer discretionary 8.58%

YTD, Materials 6.73% YTD, Telecommunication services 0.09% YTD and Energy (-8.43%)

YTD. |