|

The S&P 500 surged 2.05% on Friday, driven by the better-than-expected job reports, less-hawish comments from European Central Bank President (ECB) Mario Draghi and technical buys/short covering after the index broke the 200-day moving average head resistance. The U.S. Labor Department released the nonfarm payrolls report for November on Friday showing 211,000 jobs were added to the economy, while the U-3 headline unemployment rate held at 5.0%. Wall Street economists’ consensus expectations were only for a 200,000 jobs gain with the unemployment rate remaining at 5.0%. The August and September figures were revised by a combined 35,000 more than previously reported.

The U-6 rate, that includes all the jobless plus people marginally attached to the workforce and those employed part-time because of a weak economy, inched up 0.1 percentage point to 9.9%. The labor force participation rate in November also bumped up 0.1 percentage point to 62.5% to a level near a 38-year low, meaning about 94.45 million Americans, 16 years and older, did not have a job and were not actively trying to find one. The labor force participation rate of 62.4% in September and October was the lowest in 38 years.

The index also received additional support on Friday afternoon after ECB President Mario Draghi delivered a less-hawkish speech at the Economic Club of New York, saying that "there is no particular limit to how we can deploy any of our tools.", meaning the ECB could step up their stimulus efforts if necessary.

Just a day earlier, the ECB announced at its Governing Council meeting in Frankfurt that they would cut the overnight deposit rate to minus 0.3% from minus 0.2%, and leave its key lending rate unchanged at 0.05%. The ECB also said it decided to extend purchases of government bonds and other assets from the September 2016 target date through at least March 2017.

The markets had expected the ECB to drop the overnight rate to minus 0.4% and the key lending rate to zero from 0.05%, as well as to expand its 1.1 trillion euro bond-buying program by 360 billion euros.

Earlier in the week on Tuesday, the Institute for Supply Management (ISM) reported that its manufacturing index for the U.S. was 48.6 in November, its lowest level since June 2009, a decrease of 1.5 percentage points from the October reading of 50.1. A reading below 50 indicates contraction in the manufacturing sector. The index missed the expected 50.5 reading of economists surveyed by Reuters.

The weak ISM manufacturing index data came on the heels of a sharp drop in MNI's Chicago purchasing manager's index (PMI) on Monday, an indicator of business manufacturing and overall business activity in the Midwestern U.S., which plunged to 48.7 in November from 56.2 in October, missing Bloomberg economists’ estimate of 54. The strong dollar has reduced overseas demand for U.S. manufactured products. Some analysts, including Peter Boockvar, chief market analyst at The Lindsey Group, told CNBC that "We're in manufacturing recession.”

The Fed committee, including Federal Reserve Chair Janet Yellen, is now convinced that they are ready to raise rates at the next FOMC meeting in less than two weeks, despite the mixed bag of U.S. economic data of late, and an industrial sector that is already heading into a technical recession. In her speech delivered at the Economic Club in Washington on Wednesday, Dr. Yellen laid the groundwork for an interest rate liftoff as she put it, “Holding the federal funds rate at its current level for too long could also encourage excessive risk-taking and thus undermine financial stability,”.

The federal funds futures, traded on the Chicago Mercantile Exchange and commonly used to estimate the market’s views on the likelihood of changes in U.S. monetary policy, dropped to 21.0% for a quarter-point rate hike at the Fed’s FOMC meeting on December 15-16 while the odds for a half-point rate hike jumped to 79.1%, according to data from the CME Group as of December 4.

According to the Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) for the week ended December 1, there are 144,596 short positions of S&P 500 consolidated futures, traded on the Chicago Mercantile Exchange (CME) by leveraged funds, a decrease of 3,091 short positions from the previous week. This is compared to about 76,721 long positions, up 4,458 from the previous week.

The data suggested that hedge funds continued to cut back their short positions resulting in an increase in a net long positions of 7,549 contracts, worth about $3.9 billion, where contracts of S&P 500 futures are traded in units of $250.00 x S&P 500 index. Two months ago, hedge funds held a total of 192,998 short positions of S&P 500 consolidated futures.

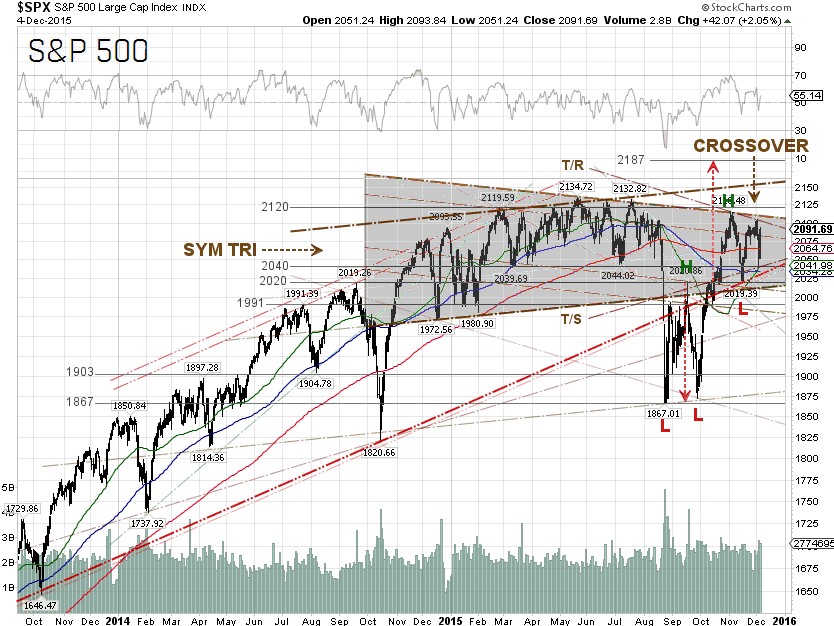

The S&P 500 closed at 2,091.69 on Friday, up 1.58 points for the week despite a weak performance in the S&P 500 Energy sector and the late-day selling on Wednesday, following the headline news of a terrorist attack in San Bernardino, California which resulted in 14 deaths and 21 injured. The best performing S&P 500 sectors for the week were Information Technology and Telecommunication Services, which jumped 1.59% and 1.29%, respectively. The worst performing S&P 500 sectors for the week were Energy and Industrials, which were down 4.54% and 0.86%, respectively.

The WTI crude price was down 3.9% for the week to close at $40.14 a barrel on Friday, after the U.S. Energy Information Administration (EIA) said on Wednesday that U.S. commercial crude oil inventories rose to 489.4 million barrels, up 1.2 million barrels in the week ending November 27. Analysts had expected an inventory draw of 668K barrels. The Organization of the Petroleum Exporting Countries (OPEC) meeting in Vienna on Friday was a non-event, as OPEC announced it had agreed to roll over its policy of maintaining crude production in order to retain market share. According to Reuters, OPEC supply rose in November to 31.77 million barrels per day (bpd) from 31.64 million bpd in October.

For the week ended December 2, Houston-based oilfield services company Baker Hughes Inc. reported the U.S. oil rig count fell another 10 from the previous week to 545, a 66.13% drop from the peak number of 1,609 in October 2014. Surprisingly, the U.S. crude oil field production is just down a mere 4.19% from a record high this summer. For the week ended November 27, 2015, the U.S. still produced 9.202 million bpd, compared to a 30-year record high of 9.604 million bpd reported in the week ended July 3, 2015. That could be one of the reasons why the Saudis may be reluctant to cut their production.

S&P 500 Summary: +1.59% YTD as of 12/04/15

Barclay Hedge Fund Index: +0.76% YTD

Outperforming Sectors: Consumer discretionary +12.34% YTD, Information technology +8.4% YTD, Healthcare +4.55% YTD, and Consumer staples +3.15% YTD.

Underperforming Sectors: Financials –0.13% YTD, Telecommunication services –2.47% YTD, Industrials –2.67% YTD, Materials –5.97% YTD, Utilities –10.76% YTD and Energy –19.2% YTD. |