|

The S&P 500 pulled back 0.46% for the week to close at 2,108.29. The Federal Reserve signaled on Wednesday, after the Federal Open Market Committee (FOMC) meeting, that the central bank may have to wait until at least the third quarter to begin raising interest rates. Some Fed members, however, said they could raise interest rates at any meeting, despite the U.S. GDP barely growing in the first quarter this year.

The U.S. Bureau of Economic Analysis (BEA), the Commerce Department, said on Wednesday that its advance estimate of first-quarter real GDP increased at the rate of 0.2%, missing economists' expectations of 1.0%. Some economists cited weather-related slowdowns in consumer spending, west coast port disputes, the strong dollar and slow growth overseas, as reasons for the deceleration in the Q1 GDP. The underlying economy is weak as businesses slashed investment, exports tumbled and consumers showed signs of caution.

The strong dollar dented revenues and profits of multi-national corporations and makes U.S. exports become less competitive. Corporations do not add workers while their profits and margins are shrinking. The argument that U.S. consumers benefit from cheap imports with a strong dollar appears not to be working, as U.S. consumers aren't spending.

Just hours after the release of the U.S. GDP data, the Federal Reserve downgraded its view of the U.S. labor market and economy in a policy statement after the two-day FOMC meeting. The Fed suggested that weather-related slowdowns and west coast port disputes are transitory factors for the weak U.S. GDP and the central bank may wait to begin raising interest rates.

Nonetheless, two Federal Reserve officials, Cleveland Fed President Loretta Mester and San Francisco Fed President John Williams, said after the meeting that the central bank is ready to raise interest rates at any meeting as the economy picks up after the harsh winter.

The currency market seemed to take what the Fed did, and not what they said, in stride and started selling the U.S. dollar when no rate hike was announced. The U.S. dollar index tumbled 1.5% to an intra-day low of 94.47 on Wednesday. For the week, the U.S. dollar index lost 1.7% to close at 95.445 on Friday, while the 10-year U.S. Treasury bond yield skyrocketed 10.34% for the week and printed at 2.112% at the close on Friday.

The best performing S&P 500 sectors for the week were Materials and Energy, up 2.02% and 1.16%, respectively. Copper and WTIC oil, which are traded in an inverse correlation with the U.S. dollar, jumped 7.25% and 3.2%, respectively for the week.

Hedge funds remain bullish on copper and crude oil as they are expecting further economic stimulus measures from China, the top consumer of those commodities. Hedge funds are betting on crude oil production and stockpiles of stored inventories to shrink beginning this month until August, amid a record drop in U.S. oil drilling rigs. Both copper and crude oil remain in underlying surplus and the stockpiles could start to build again in the third quarter.

The worst performing sectors for the week were the S&P 500 Healthcare and Consumer discretionary sectors, down 2.49% and 1.73%, respectively, due partly to sector rotation.

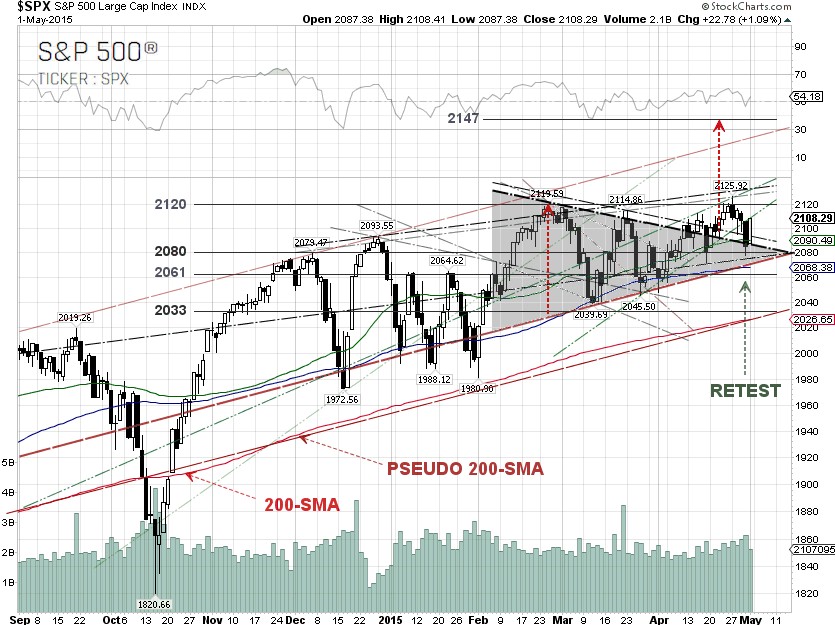

From our technical viewpoint, the S&P 500 pulled back during the week but managed to bounce off the upper trendline of the symmetrical triangle to close above the 50-day SMA. Our near-term projected target for the S&P 500 for the symmetrical triangle breakout event, remains 2,147, determined by adding the width at the top of the pattern to the point of breakout. The next major technical head resistances are 2,120 and 2,135.

Upcoming headline risks are if Greece misses the ECB and IMP payments, and the U.S. unemployment report on Friday.

S&P 500 Summary: +2.4% YTD as of 05/01/15

Barclay Hedge Fund Index: +3.49% YTD

Outperforming Sectors: Healthcare +6.06% YTD, Consumer discretionary +5.75% YTD, Materials +5.30% YTD, Telecommunication services +4.65% YTD, Information technology +3.96% YTD, and Energy +3.10% YTD.

Underperforming Sectors: Consumer staples +0.26% YTD, Industrials –0.30% YTD, Financials –1.66% YTD, and Utilities –5.95%

YTD. |