|

The S&P 500 inched up 0.43% to an intra-day high of 2,131.78 on Monday after the news came across the Bloomberg financial terminals that, “Evans Repeats Fed Shouldn’t Begin Raising Rates Until 2016”. Federal Reserve Bank of Chicago President Charles Evans, in a speech prepared for delivery to a conference in Stockholm, Sweden, repeated his call to hold interest rates near zero until early 2016 and raise them only gradually thereafter, because inflation is still too far below the Fed’s goal.

The S&P 500 Information technology sector got some lift as Carl Icahn, in an open letter to Apple Chief Executive Officer Tim Cook published on the Shareholders' Square Table website on Monday, said Apple should be trading at $240 as the company was poised to enter and dominate the television market by 2016 and the automobile market by 2020. According to a Securities and Exchange Commission (SEC) 13F filing, Mr. Icahn, activist investor and founder of Icahn Capital LP, owned about 53 million Apple shares at the end of the first quarter, worth around $6.8 billion.

On Tuesday, the S&P 500 was dragged down by the increasingly strong dollar, up 1.36% at an intra-day high, after European Central Bank (ECB) Executive Board member Benoit Coeure announced that the ECB will frontload the quantitative easing (QE) 60 billion euro monthly bond buying, in May and June, in order for the central bank not to disrupt the market when trading volumes are lower in the summer.

Trading was sluggish the rest of the week as the global markets were anticipating more information regarding the monetary policies from the minutes of the last Federal Open Market Committee (FOMC) meeting, scheduled for release on Wednesday, and important speeches from ECB president Mario Draghi and Fed Chair Janet Yellen on Friday.

Many Wall Street strategists believe that a Fed rate hike may be off the table for now as a mixed bag of weak U.S. economic data has prompted analysts and the Fed to revise their first-quarter U.S. GDP estimate and second-quarter forecasts downward.

According to MarketWatch, former Fed Vice Chairman Donald Kohn thinks that a June rate hike is too early, following weaker-than-expected April retail sales. Some Wall Street strategists believe that the Fed may begin hiking the rate later this year, or in early 2016.

Federal Reserve Chairwoman Janet Yellen, in her speech on Friday in Providence, R.I. appeared to be confident that the central bank is on track to raise interest rates this year, but will likely proceed cautiously because the job market hasn’t fully healed, inflation is low, and economic growth has again disappointed.

Prior to Yellen’s speech, the Bureau of Labor Statistics, the U.S. Department of Labor, said that the core Consumer Price Index (CPI) for all items less food and energy rose by 1.8% in April over the last year, while the food index rose 2.0%. The CPI for All Urban Consumers (CPI-U) increased 0.1%, in line with economists’ forecasts, and decreased 0.2% in unadjusted annual basis ended April 2015.

Unless the Fed is moving its goalposts, the Federal Reserve no longer emphasizes the consumer price index (CPI) as its official 2.0% inflation target. Instead, it has adopted the personal consumption expenditures (PCE) index, particularly the core PCE with the volatile prices of food and energy stripped out, because it is more real-time economic data and covers a wide range of household spending.

According to the April 30 report from the Bureau of Economic Analysis (BEA), the U.S. Department of Commerce, the March core PCE price index, excluding food and energy, increased 1.3 percent from March a year ago, well below the Fed’s inflation target of 2.0%.

It will be a reality check on May 29 when the second estimate of the first-quarter GDP will be released. The Fed’s Yellen expects the U.S. economy to strengthen while Wall Street economists forecast the first-quarter GDP second reading to contract 0.9%, compared to the initial reading of 0.2% growth.

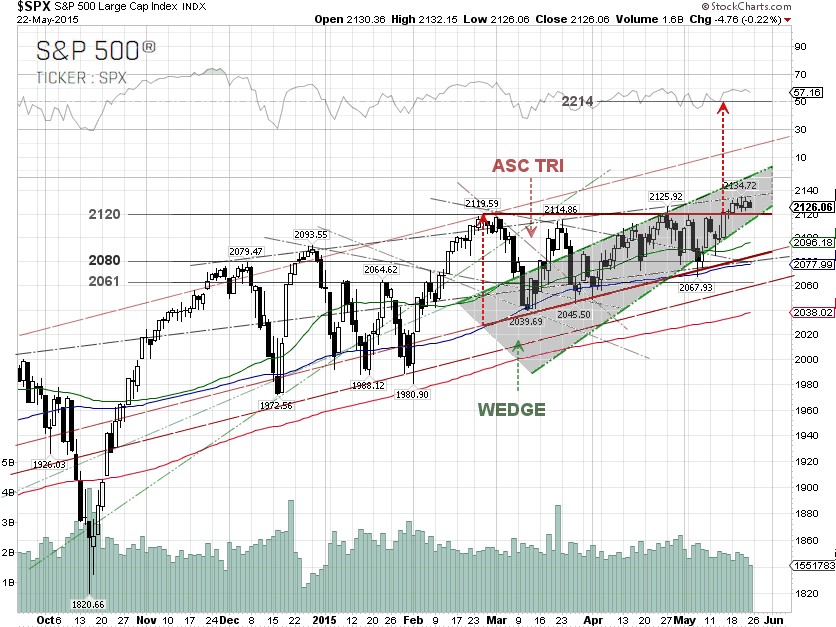

For the week, the U.S. dollar index surged 3.14% to close at 96.11 on Friday, while the 10-year U.S. Treasury bond yield gained 3.27% for the week and printed at 2.21% at the close on Friday. Despite a mixed bag of weak global economic data and a strong U.S. dollar that weighed on market sentiment, the S&P 500 hit an all-time closing high on Thursday and managed to close up 0.16% for the week, at 2,126.06 on Friday.

The best performing S&P 500 sector for the week was Healthcare, up 0.94%, as the hedge funds are getting out of the energy-healthcare trade. The worst performing sectors for the week were Consumer Staples, Materials and Energy, down 1.17%, 0.81% and 0.77%, respectively. Wal-Mart Stores [NYSE:WMT], one of the largest S&P Consumer staples stocks, tanked 4.27% for the week after the company reported a 7% drop in first-quarter profits, citing the strong dollar and a rise in the minimum wages for its hourly workers, to $9 per hour in April.

From our technical viewpoint, the S&P 500 could continue its consolidation due to a lack of clarity for when the Fed will actually begin hiking the rate, and thus raising the U.S dollar. The S&P 500 could pull back further as the U.S. dollar is continuing to gain upward momentum. The next major technical head resistances are 2,135, 2147 and 2,180 while 2,120 becomes the near-term support.

S&P 500 Summary: +3.26% YTD as of 05/22/15

Barclay Hedge Fund Index: +3.69% YTD

Outperforming Sectors: Healthcare +9.21% YTD, Consumer discretionary +6.46% YTD, Information technology +5.06% YTD, Materials +4.81% YTD, and Telecommunication services +3.47% YTD.

Underperforming Sectors: Consumer staples +1.02% YTD. Industrials +0.5% YTD, Financials +0.19% YTD, Energy –0.54% YTD and Utilities –6.17%

YTD. |