|

The U.S. Labor Department reported its November nonfarm payrolls report on Friday, showing a seasonally adjusted increase of 178,000 jobs that slightly beat Wall Street economists' median forecast of a 175,000 gain. The government revised September’s number again from 191,000 to 208,000, while October's number was lowered to 142,000 from 161,000. The U.S. unemployment rate dipped to 4.6% in November, as the civilian labor force participation rate dropped to 62.7%, meaning some 95.06 million Americans are not in the labor force. The number of people who are not in the labor force but want a job now, decreased slightly to 5.88 million in November from 5.91 million registered in October.

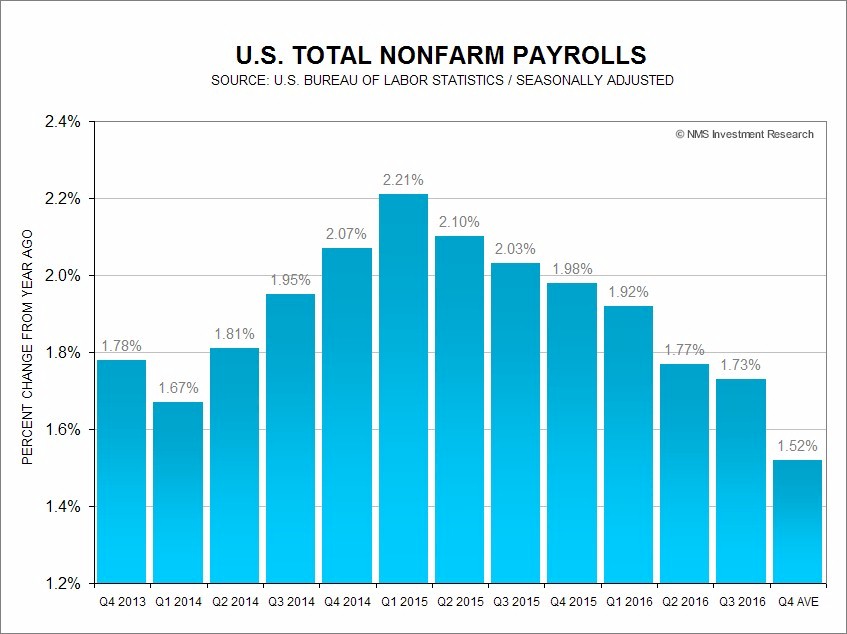

Total nonfarm payrolls growth now stands at 1.52% year-on-year, to 145.04 million in the fourth-quarter 2016, the slowest pace since the first-quarter 2013. One can argue that the slow growth in total nonfarm payrolls could be due to the lack of qualified workers, as the labor market approaches maximum employment. Nonetheless, at this rate, job growth could be well below 1% by next year.

This week’s economic news prompted the Federal Reserve Bank of New York to raise its fourth-quarter 2016 GDP forecast 30 basis points on Friday, to 2.7% from the previous 2.4%, citing positive data from GDI and the labor market, and only slightly negative figures from personal consumption expenditures. Taking the latest New York Fed forecast into account, the pace of U.S. GDP 2016 annual growth will be just 1.6% year-on-year and a compounded annual growth rate

(CAGR) of 2.1%, since the deep recession of 2009.

For the week, the U.S. Dollar index (DXY), essentially the USD/EUR exchange rate, pulled back 0.66% to close at 100.66, as the hype about a December Fed interest rate hike wanes. The yield of 10-year U.S. Treasury Notes gained 1.36% this week to close at 2.392% on Friday, while the yield spread between the 10-year and 2-year U.S. Treasury Notes widen to 1.29 percentage points. The 10-year U.S. Treasury yield is bumping into the trendline resistance at about 2.41%, but could pull back sharply if it fails to break out. The 10-year JGB yield jumped 8.11% to 0.04% at the close on Friday, while the 10-year German bund yield surged 16.18%, to close at 0.28%.

|