|

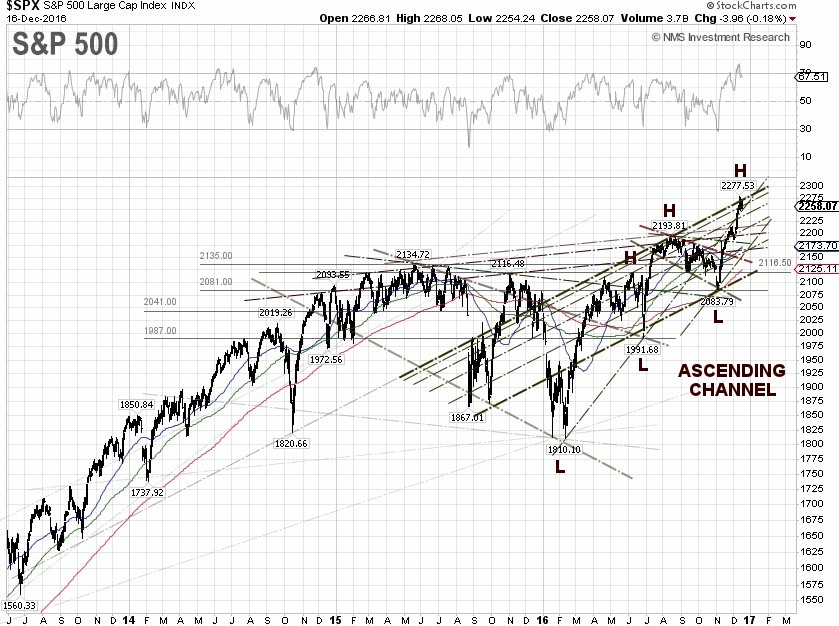

The S&P 500 declined 1.46 points for the week, to close on Friday at 2,258.07, after the Fed raised the target range for its federal funds rate by 25 basis points to 0.5% - 0.75% at the FOMC meeting on Wednesday, and signaled that there could be three more interest rate hikes in 2017. The market was surprised by the Fed’s hawkish stance, as only two quarter-point increases for next year were expected by most analysts.

The Fed’s Yellen seemed reluctant to endorse President-elect Trump's fiscal stimulus plan, as she said the following at the press conference after the FOMC meeting, “So, I would say at this point that fiscal policy is not obviously needed to provide stimulus to help us get back to full employment. But nevertheless, let me be careful that I'm not trying to provide advice to the new administration or to Congress as to what is the appropriate stance of policy.”

U.S. economic data reported this week was a mixed bag. The Department of Commerce said on Wednesday that both U.S. retail sales and core retail sales, excluding automobiles, gasoline, building materials and food services, edged up just 0.1%, missing economists' forecast of a 0.3% increase for overall retail sales and a 0.3% gain in core retail sales. The Department of Commerce also said on Friday that U.S. housing starts tumbled 18.7% in November to a seasonally adjusted annual rate of 1.09 million units, missing the forecast of 1.24 million units.

The weak U.S. economic data prompted the Federal Reserve Bank of New York to revise its fourth-quarter 2016 GDP forecast downward by 90 basis points on Friday, to 1.8% from the previous 2.7%, citing weak capacity utilization and industrial production, as well as housing data. Taking the latest New York Fed forecast into account, the pace of U.S. GDP 2016 annual growth will be just 1.55% year-on-year, the slowest annual growth in 8 years. The U.S. economy has grown at a compounded annual growth rate (CAGR) of 2.08%, since the deep recession of 2009. If the trend continues, the U.S. GDP 2017 could end up below 1%.

For the week, the U.S. Dollar index (DXY), essentially the USD/EUR exchange rate, rose another 1.4% to close at 102.92, despite the sluggish U.S. retail sales and weak housing data. The yield of 10-year U.S. Treasury Notes jumped another 5.39% this week to close at 2.599% on Friday, while the yield spread between the 10-year and 2-year U.S. Treasury Notes was unchanged at 1.32 percentage points.

The U.S. Department of Treasury’s monthly data of foreign holdings of U.S. Treasury securities for October 2016 showed that China continues dumping its U.S. debt holdings at a fast pace to keep the yuan afloat and now has just $1.1157 trillion, which is behind Japan at $1.1319 trillion. The yield of the 10-year U.S. Treasury Note is already trading at 2.6%, and it could move even higher if foreign central banks keep selling their U.S. Treasury securities. The 10-year JGB yield jumped another 43% to 0.08% at the close on Friday, while the 10-year German bund yield tumbled over 14%, to close at 0.314%.

The WTI crude price surged 2.82% this week, to close at $52.95 per barrel on Friday, while the Brent crude spot price gained 1.64% to close at $55.29 per barrel, where most of the gains came on Friday after OPEC members, including Kuwait, notified customers that cuts are coming, according to The Wall Street Journal.

Earlier in the week, the WTI crude price jumped 2.58% to close at $52.83 per barrel on Monday, after non-OPEC countries agreed on Sunday in Moscow to reduce production by 558,000 barrels a day (bpd). The market though, was expecting a deeper cut of 600,000 bpd from the non-OPEC countries in the first half of 2017. Crude Oil futures Jan 17 (CLF7), surged as high as $54.50 a barrel in electronic trading on Sunday evening in New York, following comments from Saudi Arabia’s Energy Minister Khalid al-Falih saying that the Kingdom would be cutting even more than it had committed to at the November 30 OPEC meeting in Vienna, meaning the Saudis could reduce its output below 10.058 million bpd.

The EIA weekly U.S. oil inventory report on Wednesday showed that domestic crude supplies fell by 2.6 million to 483.2 million barrels, excluding the Strategic Petroleum Reserve, in the week ending December 9, compared to The Wall Street Journal forecast for a stockpile decline of 1.7 million barrels. The American Petroleum Institute (API) inventory data on Tuesday showed a U.S. crude inventory increase of 4.7 million barrels.

Separately, the EIA said the weekly U.S. crude oil production jumped 990,000 bpd for the week ending December 9, to 8.796 million bpd. Weekly U.S. crude oil output has fallen about 8.5% from the peak level of 9.61 million bpd during the week ending June 5, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count jumped by 12 to 510, compared to 316, when the rig count hit the low on June 6, 2016.

The best performing S&P 500 sectors for the week were Telecommunication services and Utilities, up 2.26% and 1.854%, respectively. The worst performing sectors for the week were Industrials and Materials down 1.60% and 1.52%, respectively.

S&P 500 Summary: +10.48% YTD as of 12/16/16

Barclay Hedge Fund Index: +5.23% YTD

Outperforming Sectors: Energy +25.59% YTD, Financials +20.80% YTD, Industrials +16.83% YTD, Materials +15.90% YTD, Telecommunication services +15.68% YTD, Information technology +13.05% YTD, and Utilities +11.92% YTD.

Underperforming Sectors: Consumer discretionary +6.09% YTD, Consumer staples +3.40% YTD, Healthcare –3.32% YTD, and Real Estate –7.75%

YTD. |