|

The best performing S&P 500 sector for the week was Telecommunication services, up 1.39%. The worst performing sectors for the week were Healthcare and Information technology, which were down 2.09% and 1.95%, respectively. The S&P 500 Biotechnology subsector sold off again, down 3.26% for the week, as the political dark cloud hanging over prescription drug prices remains.

Presumptive nominees from both parties use their rhetoric against the pharmaceutical and biotechnology industries, while speculators have been using the political noise as a backdrop to take short positions against the sector. Fund managers continue to rotate out of other sectors into Utilities, up 16.73% year-to-date, in anticipation of a U.S. economic downturn.

Since August 2015, the S&P 500 has been positively correlated with the WTI crude oil price. Traders, including algorithmic and high-frequency traders (HFT), may be creating greater profit opportunities by coupling the volatility and price swings in the crude oil futures market with the S&P 500 index.

The WTI crude oil spot price was unchanged for the week, closing at $48.86 per barrel on Friday, while the Brent crude price was down 2.04% for the week to close at $49.36 per barrel, after mixed weekly crude oil inventory reports.

The Energy Information Administration (EIA) weekly U.S. oil inventory report on Wednesday showed a decline of 900,000 barrels to 531.5 million barrels in the week ending June 10, compared to analysts’ expectations for a drawdown of 2.26 million barrels. The American Petroleum Institute (API) inventory data on Tuesday showed U.S. crude inventories surprising increased by 1.52 million barrels.

The EIA said the weekly U.S. crude oil production decreased by 29,000 barrels per day (bpd) for the week ending June 10, 2016, to 8.716 million bpd. Weekly U.S. crude oil output has fallen about 9.3% from the peak level of 9.61 million bpd during the week ending June 6, 2015. Separately, the EIA said on Monday that oil output in the biggest producing shale areas in the U.S. is forecasted to decrease 118,000 bpd in July from June, to 4.723 million bpd, in line with the precipitous fall in oils rigs operating in U.S. shale.

Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count was up another 9 from the previous week, for the third straight week, at 337, but still down 79% from the peak number of 1,609 in October 2014. No one knows how many additional bpd will be produced, as there is no direct correlation between crude oil production and the number of rigs. One can imagine that the most productive ones would be brought back into operation first.

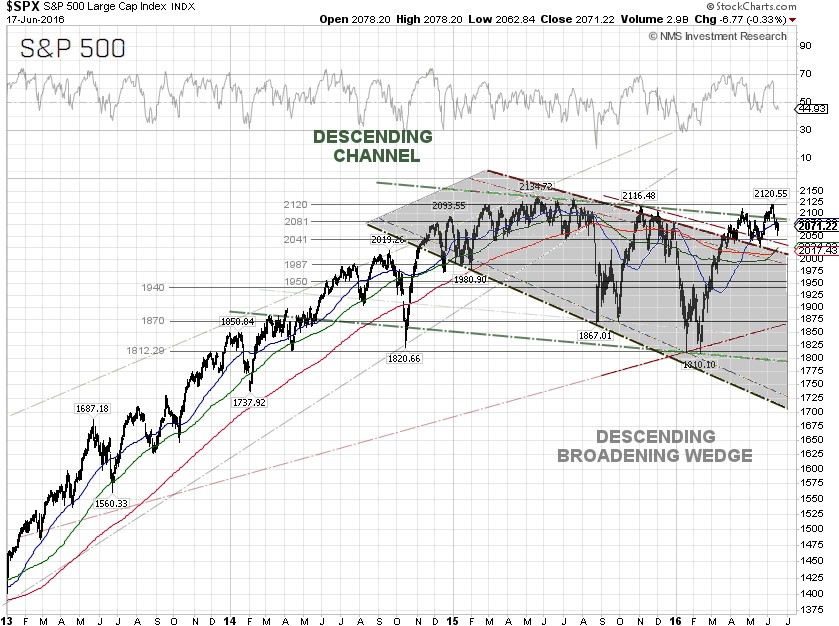

From our technical viewpoint, the S&P 500 fell back into the descending channel and below the 50-day moving average. There is a technical support at 2,041, if the index continues to pull back. In order to support the bull's case, the S&P 500 needs to close above 2,120, where a higher-high uptrend can be established.

S&P 500 Summary: +1.33% YTD as of 06/17/16

Barclay Hedge Fund Index: +0.82% YTD

Outperforming Sectors: Utilities +16.73% YTD, Telecommunication services +16.22% YTD, Energy +11.68% YTD, Materials +8.44% YTD, Consumer staples +5.85% YTD, and Industrials +4.47% YTD.

Underperforming Sectors: Consumer discretionary –0.24% YTD, Information technology –1.42% YTD, Healthcare – 2.81% YTD, and Financials –5.10%

YTD. |