|

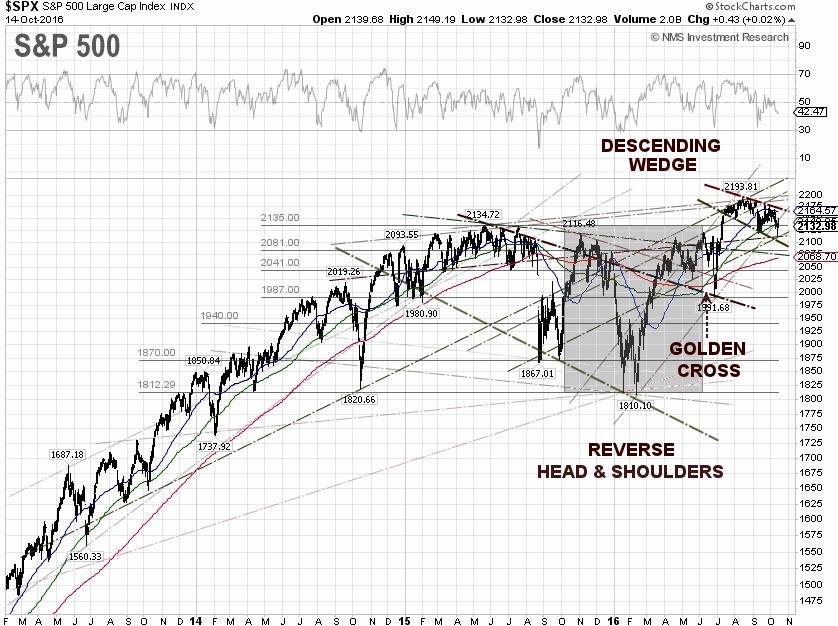

The S&P 500 traded 0.96% lower for the week, to close on Friday at 2,132.98, dragged down by the S&P 500 Healthcare sector and S&P 500 Biotechnology sub-sector, down 3.46% and 4.35%, respectively, on concerns over Democrats taking control of Congress after the November election. The S&P 500 Healthcare sector, which represents about 21.44% in the S&P 500 index, has been under selling pressures since September 2015, when Hillary Clinton, Democratic U.S. presidential candidate, went on a Twitter frenzy and sent out a tweet about “outrageous” price gouging by a pharmaceutical CEO.

To make matters worse, gene sequencing instrument maker Illumina Inc.

(NASDAQ:ILMN), a top constituent of the S&P 500 Biotechnology sub-sector, lowered its third-quarter revenue guidance, which sent its stock plunging 25%, while shares of St. Jude Medical Inc.

(NYSE:STJ) tumbled 3.5% after the company said that hundreds of thousands of its implanted defibrillators may stop working.

The minutes from the September 20-21 Federal Open Market Committee

(FOMC) meeting, released on Wednesday, revealed that among the voting members who supported waiting, the rate decision at the meeting was a close call as several said a rate hike was needed relatively soon if the labor market continued to improve and economic activity strengthened.

Three out of ten FOMC members, including Esther L. George, Loretta J.

Mester, and Eric Rosengren, dissented and preferred to increase the target range for the federal funds rate by 25 basis points at the meeting. George and Mester argued that the Fed could risk its credibility by waiting too long, while Rosengren believed that a failure to move now could require the committee to raise policy interest rates at a faster and more aggressive pace later on, which could shorten, rather than lengthen, the duration of the economic expansion.

Separately, the Labor Department said on Wednesday that their Job Openings and Labor Turnover Survey (JOLTS) showed a 6.7% drop in job openings to 5.44 million in August from 5.83 million in July. There is a warning sign of a weaker job market, as the decline in job openings, about 223,000, occurred mostly in the high-wage professional and business services sector. Job openings could have already been topping out since April 2016, when the job openings hit a record high of 5.85 million.

The Federal Reserve Bank of Atlanta came out on Friday and revised its third-quarter 2016 GDP forecast 20 basis points downward, to 1.9% from 2.1% previously, after cutting its forecast of third-quarter real personal consumption expenditures growth from 2.9% to 2.6%. The Atlanta Fed's action was prompted by the U.S. Census Bureau’s report on Friday showing that retail sales excluding food services rose 0.6% last month, compared to a 0.32% decline in August, but still missed economists' forecast, surveyed by

MarketWatch, of a 0.7% increase. On a quarterly basis, third-quarter 2016 retail sales declined 0.83 percentage points, to 0.65% from a 1.48% gain during the previous quarter.

Surprisingly, the Federal Reserve Bank of New York revised its fourth-quarter 2016 GDP forecast 30 basis points upward, to 1.6% from 1.3% previously, while it kept the third-quarter 2016 GDP forecast at 2.3%, citing higher than expected retail sales data that had the largest contribution, particularly for the fourth-quarter. Taking the latest Fed forecasts into account, the pace of U.S. GDP annual growth could be about 1.4% year-on-year, the slowest compounded annual growth rate (CAGR) since the end of the deep recession in 2009. The current blue chip consensus U.S. GDP 2016 forecast is 1.8%.

For the week, the U.S. dollar index jumped another 1.39%, to close at 97.997 on Friday. The yield of 10-year U.S. Treasury Notes surged 4.76% for the week to close at 1.805%, while the yield spread between the 10-year and 2-year U.S. Treasury Notes climbed to 0.96 percentage points. The 10-year JGB yield jumped 9.68% to negative 0.056% at the close on Friday, while the 10-year German bund yield skyrocketed over 200%, to close at 0.069%.

The WTI crude price jumped 1.89% for the week to close at $50.75 per barrel, while the Brent crude spot price inched up 0.62% to close at $52.00 per barrel, despite that Igor Sechin, Chief Executive Officer of Russia's state-controlled integrated oil company Rosneft, said his company will not cap oil production as part of a possible agreement between Russia and OPEC. According to Reuters, Sechin said he doubted that some OPEC countries, such as Iran, Saudi Arabia and Venezuela, would cut their output either.

The EIA weekly U.S. oil inventory report on Thursday, due to the Columbus Day holiday, showed that domestic crude supplies rose by 4.9 million barrels to 474 million barrels, excluding the Strategic Petroleum Reserve, in the week ending October 7, compared to S&P Global Platts analysts’ expectations for a rise of 250,000 barrels. The American Petroleum Institute (API) inventory data on Wednesday showed a U.S. crude inventory increase of 2.7 million barrels.

Separately, the EIA said the weekly U.S. crude oil production decreased by 17,000 barrels per day (bpd) for the week ending October 7, to 8.450 million bpd. Weekly U.S. crude oil output has fallen about 12.07% from the peak level of 9.61 million bpd during the week ending June 5, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count rose by 4 to 432, compared to 316, when the rig count hit the low on June 6, 2016.

The best performing S&P 500 sectors for the week were Utilities and Real Estate, up 1.33% and 1.22%, respectively. The worst performing sectors for the week were Healthcare, Materials and Energy down 3.27%, 1.19% and 1.16%, respectively.

S&P 500 Summary: +4.36% YTD as of 10/14/16

Barclay Hedge Fund Index: +4.27% YTD

Outperforming Sectors: Energy +14.68% YTD, Information technology +10.34% YTD, Utilities +10.23% YTD, Telecommunication services +10.14% YTD, Industrials +6.69% YTD, and Materials +6.24% YTD.

Underperforming Sectors: Consumer staples +3.63% YTD, Consumer discretionary +0.86% YTD, Financials +0.18% YTD, Healthcare –3.46% YTD, and Real Estate –5.88%

YTD. |