|

The WTI crude price tumbled 4.23% for the week, to close at $48.70 per barrel on Friday, while the Brent crude spot price tanked 2.41% to close at $50.67 per barrel, as OPEC is not getting closer to reaching a consensus about freezing output. According to Reuters, Ministers from Saudi Arabia, Kuwait, Bahrain, Qatar and the United Arab Emirates told their Russian Energy Minister counterpart this week that they are willing to reduce peak oil output by 4%, while Iraq, Libya, Nigeria and Iran have called for an exemption because their output had been hit by wars and sanctions.

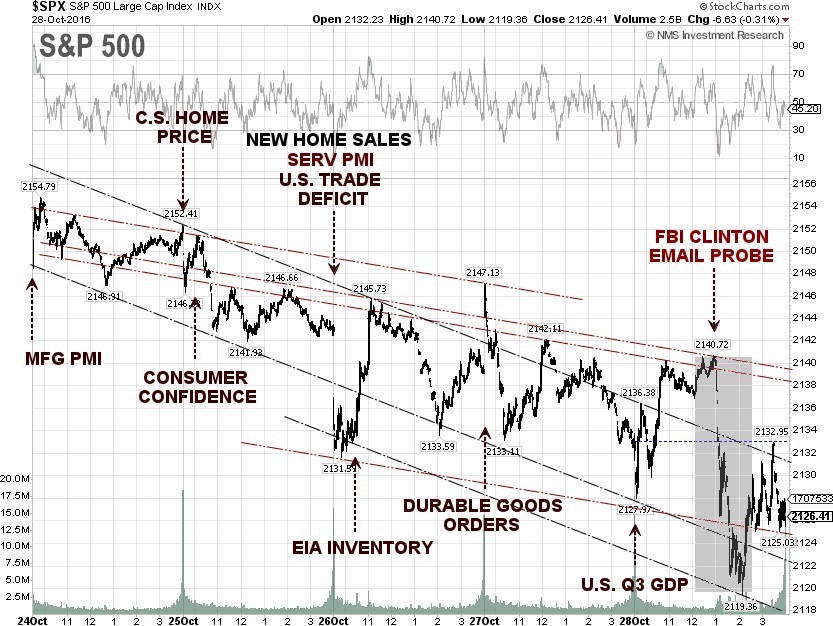

The EIA weekly U.S. oil inventory report on Wednesday showed that domestic crude supplies dropped by 0.6 million barrels to 468.2 million barrels, excluding the Strategic Petroleum Reserve, in the week ending October 21, compared to S&P Global Platts analysts’ expectations for a rise of 0.4 million barrels. The American Petroleum Institute (API) inventory data on Tuesday showed a U.S. crude inventory increase of 4.8 million barrels.

Separately, the EIA said the weekly U.S. crude oil production increased by 40,000 barrels per day (bpd) for the week ending October 21, to 8.504 million bpd. Weekly U.S. crude oil output has fallen about 11.51% from the peak level of 9.61 million bpd during the week ending June 5, 2015. Houston-based oilfield services company Baker Hughes Inc. said on Friday that the U.S. oil rig count declined by 2 to 441, compared to 316, when the rig count hit the low on June 6, 2016.

The best performing S&P 500 sectors for the week were Consumer staples and Utilities, up 0.97% and 0.86%, respectively. The worst performing sectors for the week were Real Estate and Healthcare down 3.40% and 2.78%, respectively.

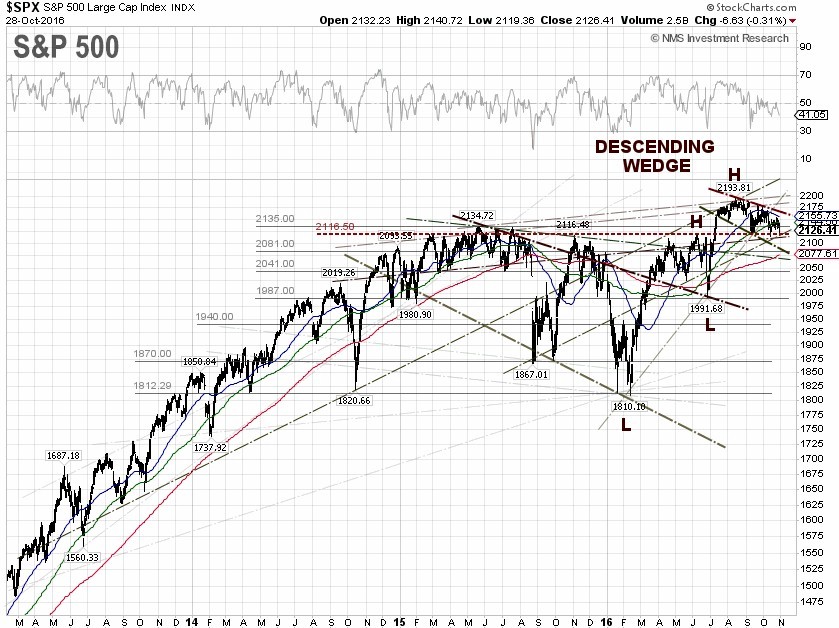

S&P 500 Summary: +4.03% YTD as of 10/28/16

Barclay Hedge Fund Index: +4.28% YTD

Outperforming Sectors: Energy +13.90% YTD, Utilities +11.80% YTD, Information technology +10.97% YTD, Materials +7.09% YTD, Industrials +6.49% YTD, Telecommunication services +5.31% YTD, and Consumer staples +4.19% YTD.

Underperforming Sectors: Financials +1.96% YTD, Consumer discretionary –0.22% YTD, Healthcare –6.02% YTD, and Real Estate –8.58%

YTD. |