|

In the fiscal third-quarter ended March 2015, Microsoft [NASDAQ:MSFT] reported revenues of $21.73 billion, up 6.5% year-over-year and diluted GAAP EPS of $0.61 per share, down 10.3% year-over-year. Wall Street was expecting earnings of $0.51 per share on revenues of $21.07 billion.

Microsoft said their revenues would have risen 9% and EPS would have declined 7% if not for the strengthening of the U.S. dollar compared to foreign currencies. The company introduced their constant currency methodology as a tool for assessing how their underlying businesses performed, excluding the effect of foreign currency rate fluctuations.

Microsoft’s consumer Windows OEM licensing segment logged revenue of $3.48 billion, down 24.4% year-over-year, while commercial licensing revenue declined 2.9% to $10.04 billion. Weak licensing revenue was offset by the commercial cloud revenue, which grew 106% year-over-year, as more businesses are paying to use software, including Office 365, Azure and Dynamics CRM Online, housed in Microsoft-managed data centers.

While the cloud business is becoming Microsoft’s fastest growing segment with an annualized revenue approaching $6.3 billion, Microsoft has not disclosed profit information as the Azure platform is facing fierce competitors, such as the Amazon Web Services (AWS).

The company said its search advertising revenue grew 21%, with Bing's U.S. market share at 20.1%, up 150 basis points year-on-year. Xbox Live usage grew over 30%, while the Surface revenue was $713 million, up 44%. Phone hardware revenue was $1.4 billion, with 8.6 million Lumia units sold.

Last month, Goldman Sachs analyst Heather Bellini sent out a research note telling her clients to sell shares of Microsoft, as the company faces currency headwinds and weakness in commercial licensing over the next three fiscal years. Ms. Bellini believes that MSFT will drop to $38 per share within the next 12 months.

Microsoft's commercial licensing segment, which sells software and services like Office, Office 365, Exchange, and SQL Server to large corporations, and makes up more than a third of Microsoft's overall revenue, continued to see a downward trend in the fiscal third-quarter. Many analysts, besides Goldman Sachs, believe that the direction downwards will continue as worldwide PC shipments are expected to fall again in 2015, for the fourth consecutive year.

According to NetMarketShare, Windows 7 users increased by 9.2% year-on-year, while Windows 8 and 8.1 users have increased by just 2.7%. Almost 17% of PC users are still hanging onto Windows XP.

Microsoft is planning to offer Windows 10 at steep discounts for manufacturers to use in lower-priced tablets and laptops. The company will also give away a free one year upgrade, from Windows 8.1 to Windows 10 when it launches, on Windows PC’s and devices, such as the Surface 3. Thus, Microsoft won't generate a lot of revenue from Windows 10 at least until fiscal year 2016.

Microsoft didn’t definitely say when the company will launch Windows 10 with new features for PCs and mobile devices. According to Kevin Turner, Chief Operating Officer of Microsoft in late 2014, the final version of Windows 10 could be shipped as soon as summer 2015. Meanwhile, Microsoft is being challenged by Google Inc. [NASDAQ:GOOGL], with the $149 Chromebook laptops in the low-priced computer market, and by Apple [NASDAQ:AAPL], with the $1,299 Apple MacBook in the high-end market.

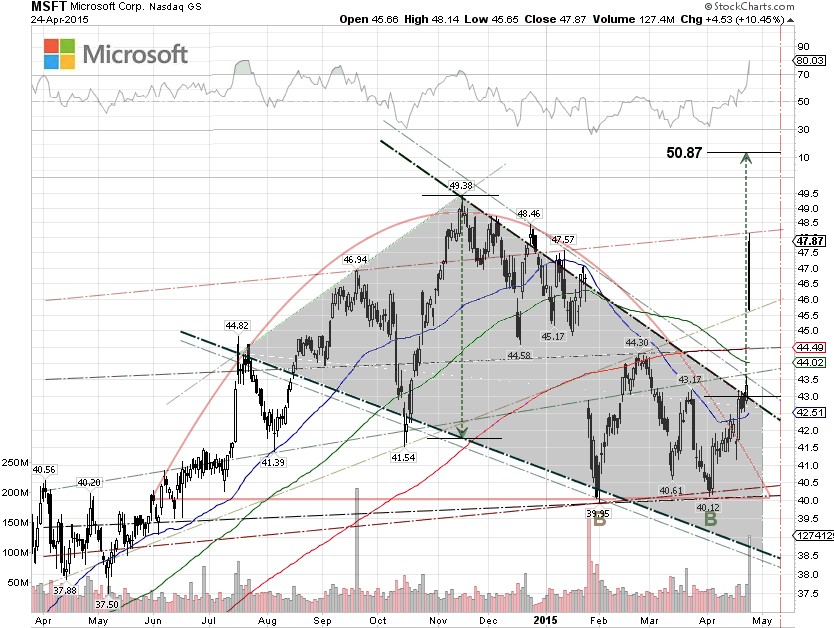

From our technical viewpoint, MSFT bounced off the $40.12 resistance level and made a double bottom as investor sentiment shifted. The stock broke out of the bullish falling wedge at $43, ahead of its earnings report on Thursday. The projected price after the falling wedge breakout, determined by adding the width of the pattern to the point of breakout, is about $50.38.

The MSFT shares had a 8.63% gap down on January 26 after reporting disappointing earnings. The gap is closed as the stock managed to finish at $47.87 on Friday, up 10.45% from the Thursday close of $43.34. The stock could pull back to the $46 level and consolidate, as it is now traded in overbought territory.

Analyst Rick Sherlund at Nomura Securities upped his rating on MSFT to Buy from Neutral on Friday and raised his price target to $50. Microsoft will report its next earnings on July 21. The revenue consensus is $22.68 billion, down 3%, and an EPS of $0.60, up 8% year-over-year.

Disclosure: No Positions in MSFT or GOOGL. Long position in AAPL.

|