|

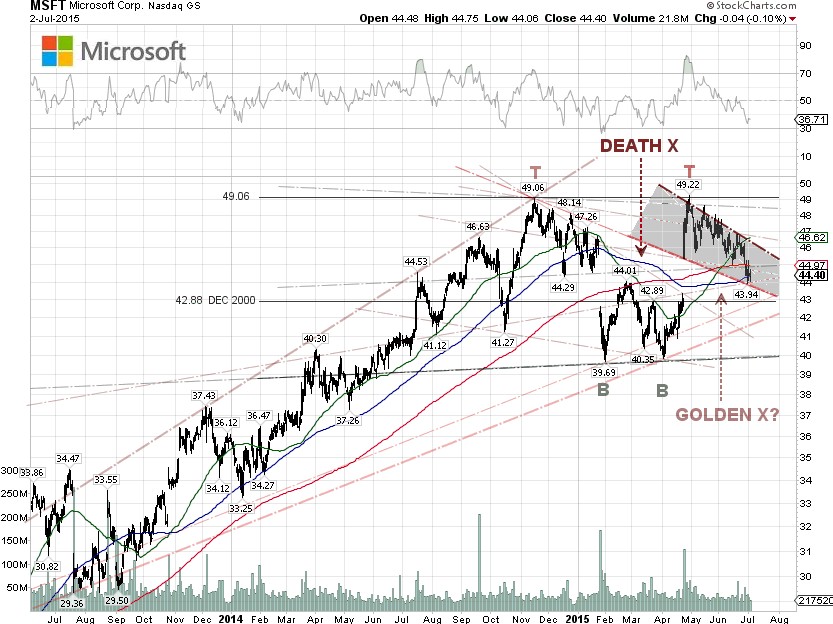

Microsoft [NASDAQ:MSFT] shares closed on Thursday at $44.40 a share, down 3.42% since Microsoft CEO Satya Nadella announced a major shakeup of his senior management team on June 17, compared to a 0.80% decline in the NASDAQ 100, the most actively traded U.S. technology companies listed on the Nasdaq stock exchange, during the same period. Since Mr. Nadella was appointed as Microsoft CEO on February 4, 2014 until this Thursday, MSFT shares have climbed just 26.07%, excluding their 3% plus dividend, about in-line with the performance of the NASDAQ 100, which registered a gain of 27.76% during the same period.

Investors have been exiting Microsoft shares of late, as the long-term downside risks of the stock increase. One of the downside risks stemmed from the news that Intel [NASDAQ:INTC] is laying off workers, based on poor outlook for the PC industry in 2015. According to the recent Gartner’s second quarter IT spending forecast, the release of Windows 10 could lead to a surge in PC sales until early 2016, but this won’t be enough to reverse the continued decline of the wider PC market.

Just weeks before the Windows 10 scheduled release date, Terry Myerson, a top lieutenant of Nadella and Windows boss, who leads the newly combined Windows and Devices Group (WDG), said that Windows 10 will now have a staggered rollout and the vast majority of upgraders will actually have to wait in line.

Based on real-time web analytics data from NetMarketshare, Windows 7's user share surged in June to 67.1% of all 1.5 billion Windows personal computers worldwide, meaning glitches in Windows 10 upgrade plans could spell disaster for Microsoft, as some users may decide to continue using Windows 7 until the problems are fixed.

According to Goldman Sachs analyst Heather Bellini, Microsoft will be facing currency headwinds and weakness in commercial licensing over the next three fiscal years. Microsoft's commercial licensing segment, which sells software and services like Office, Office 365, Exchange, and SQL Server to large corporations, and makes up more than a third of Microsoft's overall revenue, continued to see a downward trend in the fiscal third-quarter.

Many analysts, including Citi, believe that the direction downwards will continue as worldwide PC shipments are expected to fall again in 2015, for the fourth consecutive year. |