|

The Saudis have ramped up production above 10 million bpd for the past few months. According to Bloomberg, the Saudis increased its production by 50,000 bpd to 10.276 million in October. In August, Saudi Arabia told OPEC that its June production of 10.564 million bpd was a record, exceeding a previous all-time high set in 1980. Bloomberg also reported that Saudi Arabias commercial petroleum stockpiles increased to 320 million barrels, the highest since at least 2002, from 319.5 million barrels in June, according to data on the Riyadh-based Joint Organisations Data Initiative's website in late September. As of November 3, there are 281,962 long positions of light sweet crude oil futures, traded on the New York Mercantile Exchange by managed money or hedge funds, an increase of 8,526 long positions from the previous week, according to the Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) each Friday.

This is compared to about 116,224 short positions, a decrease of 18,020 short positions from the previous week where light sweet crude oil contracts are traded in units of 1,000 barrels. Hedge funds have increased their net long positions by about 26,546 contracts, as they are doubling down on the crude oil bet.

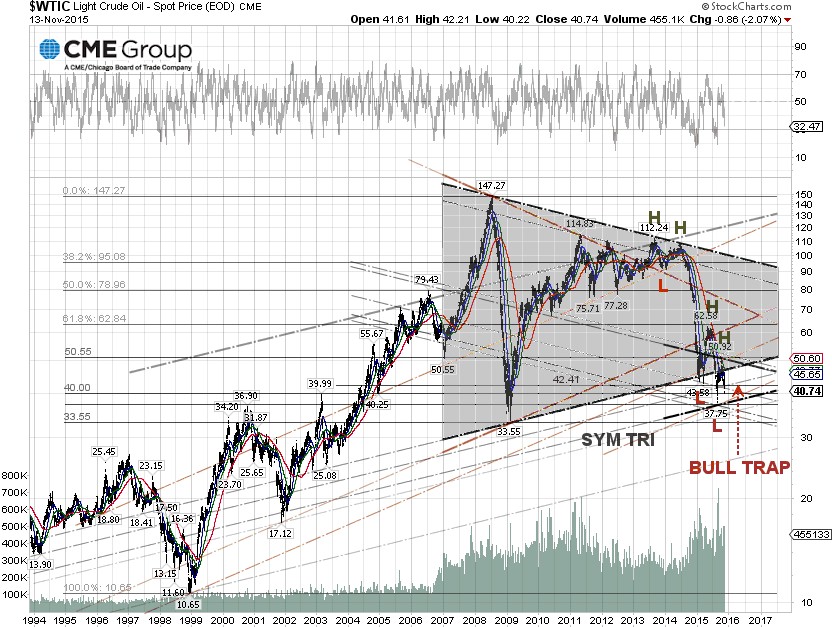

Technically, the crude oil price has been moving in a bearish lower low chart pattern since 2013. The increased probability of a Fed rate hike would put selling pressure on the crude oil price, in addition to the global oil glut. The federal funds futures, traded on the Chicago Mercantile Exchange and commonly used to estimate the markets views on the likelihood of changes in U.S. monetary policy, indicate 30.3% odds for a quarter-point rate hike and 69.8% odds for a half-point rate hike at the Fed's December FOMC meeting, according to data from the CME Group as of November 13.

We expect the crude price to pull back further as the glut continues, and the demand for heating oil in the northeastern U.S. to diminish due to the warmer winter temperatures that the El Niþo weather pattern brings. There are technical supports at around $40 per barrel and $37.75 per barrel, or the August low.

The near-term headline risks are the Governing Council of the European Central Bank (ECB), in Frankfurt on December 3. The ECB could announce the expansion and extension its 1.1 trillion euro bond-buying program. The move could bump up the U.S. dollar against the euro and put even more selling pressure on crude prices. The U.S. nonfarm payrolls report for November will be released by the Labor Department Friday, December 4. The OPEC ministers will also meet on December 4 in Vienna to review their current policy.

The long-term risk is that the crude oil price runs into a symmetrical triangle (SYM TRI) chart pattern between $50 and $35 per barrel, which we call the bull trap. If the crude price cant break out of the symmetrical triangle pattern, the price could bounce up and down until 2017, with a potential price target of $45 per barrel. |