|

The economic data for the U.S. and UK are still a mixed bag at

best. Last week, market research group Markit said its UK

manufacturing purchasing managers' index (PMI) fell to 51.5 in

August, down from 51.9 in July, while the August services PMI

dropped to 55.6 from a reading of 57.4 in July. Analysts had

expected the services index to rise to 57.6 in August. For the

index, a level above 50.0 indicates expansion in the industry,

below 50.0 indicates contraction.

As of September 8, there are 39,446 short positions of British

pound sterling (CME:6B), traded on the Chicago Mercantile

Exchange (CME), by leveraged funds, a week-over-week increase of

7,718 short positions. This is compared to about 53,722 long

positions, down 14,569 from the previous week, according to the

Commitment of Traders (COT) data released by the Commodity

Futures Trading Commission (CFTC) each Friday.

Hedge funds have decreased their net long positions about 22,287

contracts from the previous week, where British pound sterling

contracts are traded in units of 62,500 GBP. The reduction in

the net long positions reflected the GBP/USD price movement last

week.

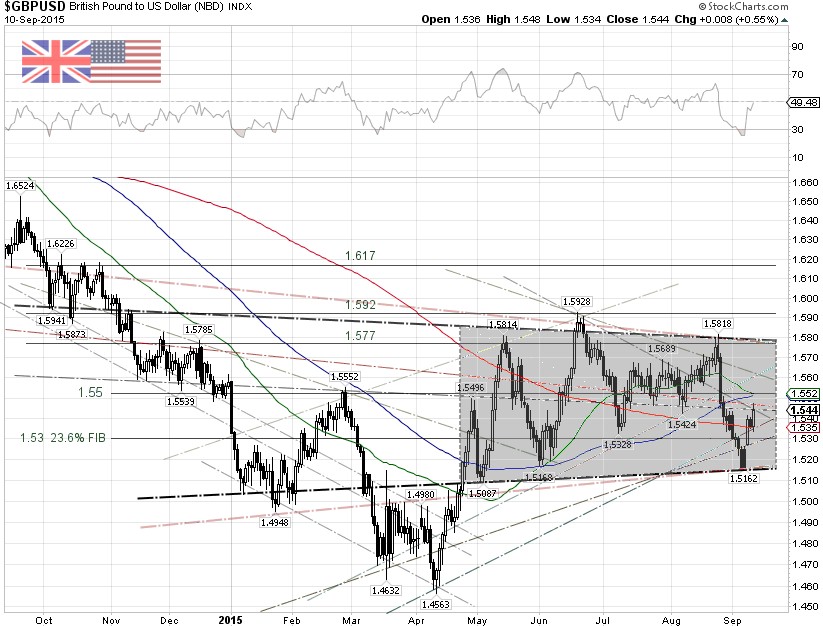

Technically, the GBP/USD has been trading in a symmetrical

triangle, a trading band, between 1.515 and 1.581 dollars per

British pound since late April. Although a golden cross was

triggered at the end of June, where the 50-day SMA crosses above

the 200-day SMA, the indicator seems to be unreliable as the

currency pair still struggled within the trading range.

The direction in which the cable will be heading next could well

depend upon the Federal Reserve rate hike decision on September

17. Concerns about China’s economic hard landing and turmoil

in global financial markets, which have sent the Japanese yen

skyrocketing, could return after the Federal Reserve meeting. |