|

The U.S. dollar index (DXY) pulled back 0.91% to close at 94.677 on Thursday, after the Federal Reserve decided to hold off a rate hike and maintain their zero interest rate policy after its Federal Open Market Committee (FOMC) Meeting, citing the economic slowdown in China and emerging markets as the reason for the delay. The Federal Reserve also revised U.S. GDP to 2.1% for 2015, up from the June forecast of 1.9%, and downgraded the 2016 GDP to 2.3% from the 2.5% projection in June. The Federal Reserve now sees inflation back to 2% by 2017, or later.

In late August, many Wall Street economists, including Barclays U.S. economists Michael Gapen and Rob Martin, projected the timing for the first Federal Reserve interest rate hike to be March 2016, citing volatile market conditions due to anxiety about the Chinese economy. According to data compiled by Bloomberg prior to the FOMC meeting, the odds of an increase in September had fallen this week to 26%, down from 40% when the survey was done at the end of July. So, the decision by the Federal Reserve not to hike the rate should have come as no surprise.

The dollar could be under selling pressure again as on October 1, when the 2016 fiscal year starts, the U.S. government will shut down unless Congress and the White House can agree on a bill that would keep money moving from the Department of the Treasury to the federal agencies and programs it funds. The Congress and the White House may have room to negotiate until between mid-November and early December as, according to the Congressional Budget Office, the Treasury Department will begin to run out of cash.

To put the current U.S. debt crisis into perspective, during the debt ceiling crisis in 2013, the U.S. dollar index sank to 79.06 in late October from a multi-year high of 84.96 in July, as President Obama and the Republicans disagreed on the terms of raising the nation’s debt limit, resulting in a 16-day partial government shutdown. That crisis began in January 2013, when the United States reached the debt ceiling of $16.394 trillion. As of Friday, September 18, 2015, U.S. debt has risen to $18.39 trillion. On January 20, 2009, the day President Obama was inaugurated, the federal debt stood at $10.62 trillion.

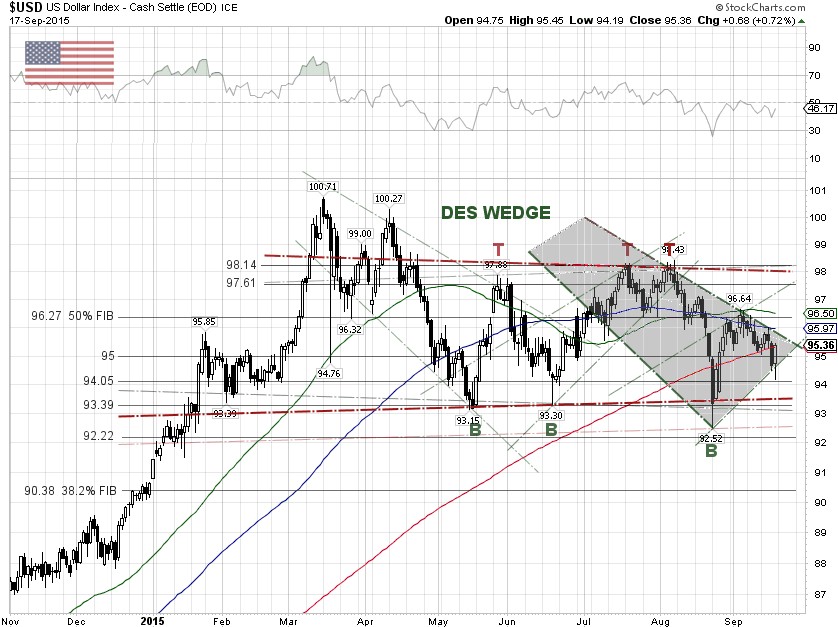

Technically, the DXY index has been trading in a symmetrical triangle, a trading band, between 93.39 and 98.14 since late April. In the short-term however, a bullish descending wedge has emerged. The volatility in the equity markets could drive the DXY higher with the breakout point of the descending wedge at about 95.50. If the dollar rally fails, the index could pull back to revisit the levels between 93.50 and 92.50, as the debt ceiling deadline looms. |