|

The SET gained 0.43% for the week, to close at 1,400.72 on Friday, up 8.75% year-to-date. The USD/THB exchange rate was quoted at 35.17 baht per dollar on Friday, down 2.39% since the beginning of the year, while the CNY/THB has declined 2.51% year-to-date, to close at 5.4272 baht per yuan.

The Thailand 10-year bond yield plunged 11.17%, to a record low of 1.67% at the close on Friday, down 33.73% year-to-date. The yield spread between the Thailand 10-year bond and the benchmark U.S. 10-year Treasury Note, yielding at 1.774% on Friday, is –0.104 percentage points, meaning investors are willing not to be paid a premium to hold a Thailand 10-year bond over a U.S. 10-year Treasury Note, which is typically perceived as safer.

Thai banks, government pension funds and currency speculators are now piling onto sovereign bonds. According to Bloomberg, deposits at Thai commercial banks have reached 12.3 trillion baht at the end of January and the money needs to be parked somewhere. “As long as excess deposits continue to build in the banking system and loan demand doesn’t pick up, Thai bonds are likely to see continued interest,” said Manu George, a Singapore-based Asian fixed-income investment director at Schroder Investment Management Ltd.

The yield spread between the Thailand benchmark interest rate, at 1.5%, and the Thailand 10-year bond is now at 0.17 percentage points. If the trend continues, the yield curve of the Thai bonds will be inverted.

The Asian Development Bank (ADB) slashed Thailand's economic growth outlook on Thursday for this year to 3.0% from 3.5%, citing gloomy global prospects, according to Bangkok Post. Last week, the Bank of Thailand cut its 2016 economic growth estimate to 3.1% from 3.5% as the bank saw that exports contracted to 2.0%, coupled with slow growth in private consumption and investment. Last Friday, the University of the Thai Chamber of Commerce (UTCC) said escalating drought conditions could knock down economic growth to only 2.7% - 2.9% this year, from the 3.0% - 3.5% growth previously forecasted.

The WTI crude oil price closed down 7.48% for the week, at $36.63 per barrel on Friday, after another bearish Energy Information Administration (EIA) inventory report showed a build of 2.39 million barrels, compared to analysts’ expectations for a 2.0 million barrel build. Adding to the volatility was a comment from Saudi Arabia’s deputy crown prince, Mohammed bin Salman, in an interview with Bloomberg that his country will freeze its oil output only if Iran and other major producers agree to curb theirs.

Thus far, Iran said that they would attend the meeting between OPEC and non-OPEC producers in Doha on April 17 to discuss a deal to freeze output. It however, does not mean that Iran will take part in negotiations over production freezes, according to CNBC.

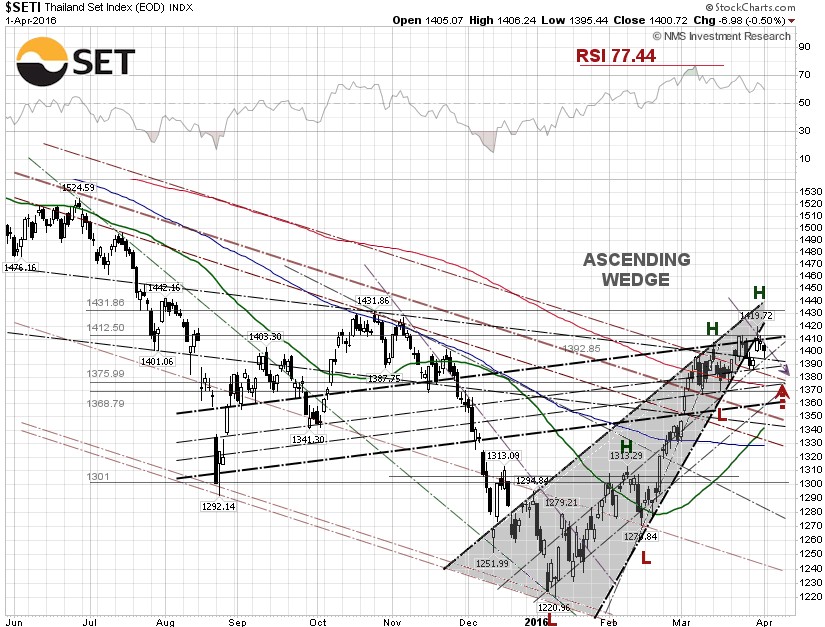

From our technical viewpoint, the SET continues to inch higher despite that the technical indicators are deteriorating. The RSI topped out at 77.44 on March 7, the highest level in 20 months. The Moving Average Convergence Divergence (MACD) runs below the signal line, meaning it may be time to be cautious and lighten up. Some traders and quant funds may continue chasing the market performance, as the 50-day SMA (green line) just managed to cross over the 100-day SMA (blue line) and the higher high chart pattern is still intact. On a cautious note, a rounding top may be forming. The next support level is between 1,384 and 1,376, if the SET pulls back.

Hot money may continue to flow into emerging market funds, as the federal funds futures, traded on the Chicago Mercantile Exchange and commonly used to estimate the market’s views on the likelihood of changes in U.S. monetary policy, indicate just 5% odds for a rate hike at the Fed’s FOMC meeting on April 26-27, while the odds are 51% for the September 20-21 meeting, according to data from the CME Group as of April 1. The market signaled that the Fed’s next move is more likely at the September meeting.

|