|

The SET gained 0.85% for the week, to close at 1,394.78 on Friday, up 8.29% for the year. The USD/THB exchange rate was quoted at 35.293 baht per dollar on Friday, down 2.05% since the beginning of the year, while the CNY/THB has declined 2.59% year-to-date, to close at 5.423 baht per yuan. The USD/THB bounced off the 34.70 baht per dollar low last Thursday, as FX currency traders took profits after the Bank of Thailand (BoT) 's Monetary Policy Committee (MPC) kept its interest rate unchanged on Wednesday, but trimmed its GDP growth forecast to 3.1% in anticipation of exports contraction.

In December, the BoT cut its 2016 economic growth estimate to 3.5% from 3.7% as the bank saw no growth in exports. Last Friday, ahead of the BoT’s announcement, TMB Bank Analytics cut Thailand's economic growth forecast to 2.8% for 2016, citing a continuation of exports contraction and constrained private consumption by high household debt, according to Bangkok Post.

The Thailand 10-year bond yield was 1.88% at the close on Friday, up 5.62% for the week and 25.4% year-to-date. The yield spread between the Thailand 10-year bond and the benchmark U.S. 10-year Treasury Note, yielding at 1.90% on Friday, is –0.02 percentage points, meaning investors are willing not to be paid a premium to hold a Thailand 10-year bond over a U.S. 10-year Treasury Note, which is typically perceived as safer.

The WTI crude oil price closed down 3.74% for the week, below the $40 per barrel psychological level, after a bearish Energy Information Administration (EIA) inventory report showed a build of 9.36 million barrels, compared to analysts’ expectations for a 2.53 million barrel build. Adding to the volatility was the rollover from the April to the May contracts (CLK6), and comments from Federal Reserve Bank of St. Louis President James Bullard. Mr. Bullard told Bloomberg on Wednesday that policymakers should consider raising interest rates at their next meeting amid a broadly unchanged economic outlook and prospects of inflation and unemployment exceeding targets.

Mr. Bullard, one of the U.S. Federal Reserve's most prominent advocates of higher interest rates, looks like he now has second thoughts because in mid-February, he told Reuters that it was "unwise" to move any further in light of weak inflation and global volatility. Just last week, the Fed kept the key interest rate unchanged at between 0.25% and 0.5% and hinted that they may make only two rate increases by the end of the year, half the number that was forecasted at its December meeting. The Fed also trimmed its economic growth outlook for the year to 2.2%, from the previous forecast of 2.4% growth, and its forecast for inflation to 1.2% from 1.6%.

The federal funds futures, traded on the Chicago Mercantile Exchange and commonly used to estimate the market’s views on the likelihood of changes in U.S. monetary policy, moved to 12% odds for a rate hike at the Fed’s FOMC meeting on April 26-27, while the odds are now 55% for the July 26-27 meeting, according to data from the CME Group as of March 24. The market signaled that the Fed’s next move is more likely at the July meeting.

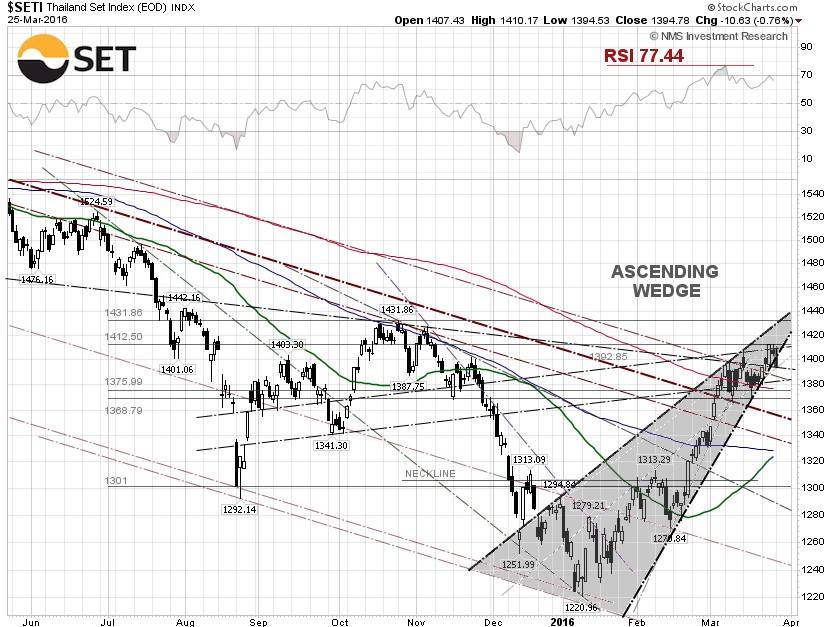

From our technical viewpoint, the SET continues to inch higher despite that the technical indicators are deteriorating. It is going to be a hit-and-miss activity, as one doesn’t know if the top is in until after the fact. The RSI registered at 77.44 on March 7, the highest level in 20 months. The Moving Average Convergence Divergence (MACD) runs below the signal line, meaning it may be time to be cautious and lighten up. The next support level is between 1,384 and 1,376, if the SET continues to pull back. Some traders may continue chasing the market performance, if the 50-day SMA manages to cross over the 100-day

SMA.

|