|

The Bureau of Labor Statistics, a unit of U.S. Department of Labor, said on Friday that employers added 257,000 jobs in January, beating the economists’ forecast for 235,000 job gains. The labor force participation rate rose to 62.9%, from 58.8% a year ago, while the average hourly earnings growth rate is now 2.2% year-over-year.

The unemployment rate was up slightly to 5.7%. The U6 unemployment rate — which includes people who are working part time for economic reasons as well as people marginally attached to the labor force — did move up slightly from 11.2% to 11.5%. The November and December numbers were revised upward. Surprisingly, the biggest hiring industry in January was retail trade with 46,000 jobs added.

The upward revision for the December jobs number, from 252,000 to 329,000, seems not to be coherent with the consumer spending report by the U.S. Commerce Department on Monday, showing a decline of 0.3% in December, the largest decline since September 2009. Economists had expected a decline of 0.2%.

Economists do not seem to have a good answer to why discretionary spending is still on the decline despite a pick-up in the U.S. job market, upbeat consumer confidence, and cheaper gas prices.

The 10-year U.S. Treasury yield surged 8.96% to close at 1.95% on Friday. The U.S. Treasury yield curve flattened as Wall Street increased its bets that the Fed could bump up its rate hike timetable to between June and September. The hedge funds sold gold, the euro and yen and bought U.S. dollars in anticipation of a strong U.S. economy and more monetary easing ahead from the central banks around the world.

The S&P 500 initially ran up after the jobs report, but took a U-turn after the Standard & Poor’s credit ratings agency came out and cut its rating on Greece from B to B-, just a notch above junk level. In the statement, S&P warned that a further downgrade is possible if Greece draws out negotiations for a bailout plan that could badly hurt Greece’s economy.

After the U.S. markets closed on Friday, Moody's also announced that their agency put the Greece government bond ratings on review for downgrades.

The S&P downgrade and Moody’s warning came after the newly-appointed Greece Finance Minister, Yanis Varoufakis, was unsuccessful on Wednesday in convincing the European Central Bank (ECB) and Germany’s Finance Minister, Wolfgang Schäuble, to accept his debt swap deal.

Instead, the ECB told Mr. Yanis Varoufakis that the Greek banks can no longer use the country’s sovereign debt as collateral for ECB-provided liquidity, meaning Greece may be “weeks” away from running out of money unless its government strikes a deal with the ECB.

S&P 500 Telecommunication services was the best sector performer, up over 6% for the week, as Mr. Tom Wheeler, head of the Federal Communications Commission, announced his proposal on Wednesday to regulate Internet service providers as utilities.

The market interpretated Mr. Wheeler’s proposal as good news for the telecommunications companies as it contained no language regarding price regulations, tariffs or requirements to give competitors access to their networks.

Internet Service Provider (ISP) stocks, such as Comcast [NASDAQ:CMCSA], Time Warner Cable [NYSE:TWC], Charter Communications [NASDAQ:CHTR] and Cablevision Systems Corp. [NYSE:CVC] were up 5-6% across the board.

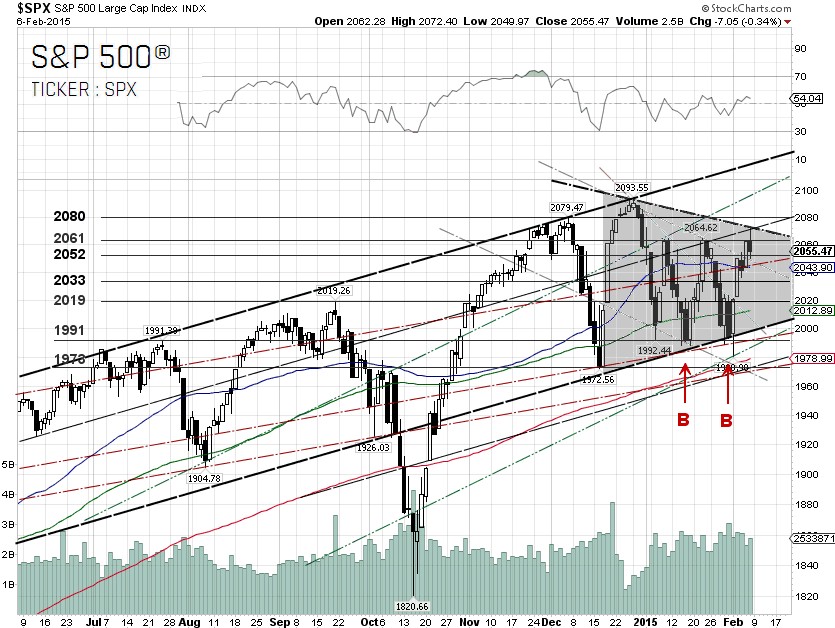

The S&P 500 bounced off the 1991 support level and formed a potential double bottom. A symmetrical triangle has now emerged. A symmetrical triangle breakout will confirm the double bottom and could push the S&P 500 to the 2100 level.

Of course, the S&P 500 could pull back and retest the ~ 2000 level again, as Greece’s debt drama continues to unfold next week. The newly-elected Greek prime minister, Alexis Tsipras, is due to attend the EU leaders' summit in Brussels on February 12. No one can predict what might happen. We hope that he at least wears a necktie!

S&P 500 Summary: –0.16% YTD as of 02/06/15

Outperforming Sectors: Telecommunication services 4.55% YTD, Materials 2.60% YTD, Healthcare 1.87% YTD, Consumer discretionary 0.96% YTD, Consumer staples 0.93% YTD, and Energy 0.24% YTD.

Underperforming Sectors: Industrials –0.78% YTD, Utilities –1.48% YTD, Information technology –1.51% YTD and Financials –2.52%

YTD. |