|

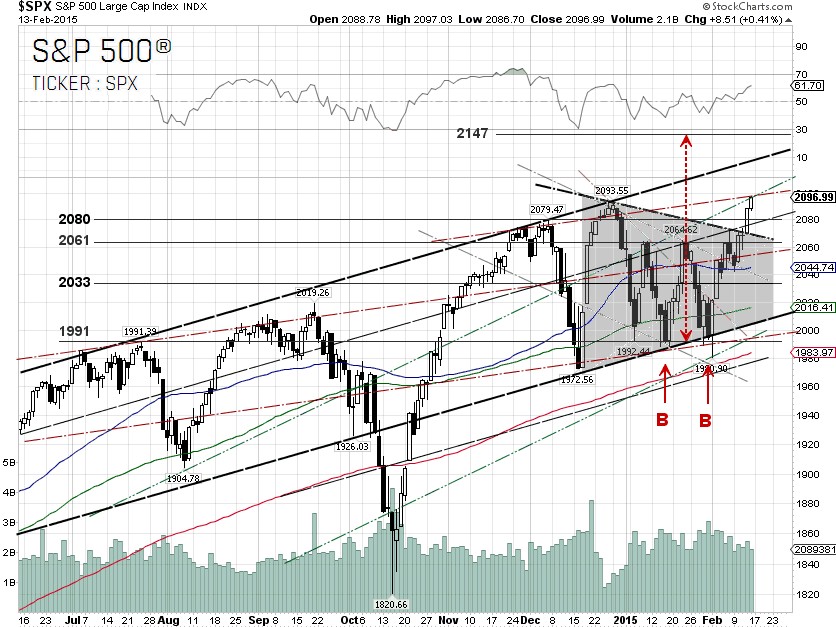

The S&P 500 broke out of the symmetrical triangle and closed on Friday at an all-time high of 2096.99. The S&P 500 was up 2.01% for the week, despite some mixed U.S. economic data. Companies like Apple [NASDAQ:AAPL] and Microsoft [NASDAQ:MSFT], which are weighted at about 4% and 1.92% of the S&P 500, respectively, were up 6.85% and 3.44% for the week.

The Bureau of Labor Statistics (BLS), the U.S. Department of Labor, said on Tuesday in their latest job openings and labor turnover survey, or JOLTS report, that U.S. job openings surged to more than 5 million in December. The strong number of job openings came on the heels of better-than-expected reports last week showing improvements in labor force participation rate and the average hourly earnings.

Despite a pick-up in the U.S. job market, upbeat consumer confidence, and cheaper gas prices, the Bureau of Economic Analysis, the U.S. Commerce Department, said on Thursday that the core retail sales excluding automobiles, gasoline, building materials and food services rose only 0.1% in January, missing economists’ expectations of a 0.4% increase.

According to Reuters, Barclays is trimming its first-quarter U.S. GDP growth estimate from 2.5% to 2.2% while J.P. Morgan cut its estimate from 3% to 2.5%. Thus far, the markets seemed to have completely ignored this news.

The markets took the job reports and increased their bets that the Fed could bump up its rate hike timetable to between June and September, based on the employment data. The 10-year U.S. Treasury yield tumbled 3.59% for the week and closed at 2.02%, just above the 50-day SMA at 2.01%.

The best performing sector was S&P 500 Materials. Companies in the sector, including PPG Industries [NYSE:PPG], Dow Chemical [NYSE:DOW], Freeport-McMoran Inc [NYSE:FCX] and Monsanto Co. [NYSE:MON] were up between 2.17% to 7.69% as the markets turned away from safer assets, such as S&P 500 Utilities and U.S. Treasuries, and shifted into riskier areas of the market. S&P 500 Utilities was down almost 3% for the week and is down 4.75% year-to-date.

Crude oil futures for delivery in March 15 [CLH15.NYM] surged 4.05% on Friday to an intraday high of U.S. $53.43 per barrel and closed at U.S. $52.65 per barrel on the New York Mercantile Exchange (NYMEX) after the leaders of Russia, Ukraine, France and Germany reached a ceasefire deal for the year-long Ukrainian conflict.

The S&P Energy sector gained over 3% for the week, despite that the crude oil price was only up 0.63%. The price gyrated throughout the week as the Organization of the Petroleum Exporting Countries (OPEC) and the International Energy Agency (IEA) sent out mixed messages regarding crude oil production and demand.

OPEC said on Monday that OPEC oil production will increase by 430,000 million barrels per day (bpd) from its previous forecast to 29.21 million bpd in 2015, as non-OPEC countries begin to cut their capital expenditures and production.

The IEA came out and warned on Tuesday that the oil inventories of non-OPEC countries may approach a record 2.83 billion barrels by mid-2015 before cuts in capital expenditures begin to have a significant impact on production. The markets seemed not to care either that the IEA’s forecast of global oil demand growth for 2015 is unchanged from last month's report, at 0.9 million bpd, bringing average demand for the year to 93.4 million bpd.

On Friday, Baker Hughes [NYSE:BHI], one of the world's largest oilfield services companies, issued its weekly report saying that the U.S. oil drilling rig count fell again to 1,056 in the week ending February 13, down over 34% from the record highs of 1,609 set in October 2014. For reference, the U.S. oil drilling rig count stood between 200 and 400 during the financial crisis in 2009.

Technically, the S&P 500 broke out of a symmetrical triangle and the 1991 double bottom was confirmed. The technical projection for the S&P 500 is 2147. Of course, the S&P 500 could pull back and retest the ~ 2000 level again, as Greece’s left-wing government is still negotiating with its creditors. The Greek government and Greek banks could be running out of money as early as next month if no agreement between Greece and the ECB can be reached.

ECB President Mario Draghi’s quantitative easing (QE), set to begin next month, is still facing some legal and political hurdles, largely from Germany. In theory, it is still possible that the German Federal Constitutional Court in

Karlsruhe could instruct the German Bundesbank not to cooperate with the ECB bond-purchasing program.

The judges in Karlsruhe expressed serious doubts last year about the legality of the ECB’s bond-buying program, so-called Outright Monetary Transactions (OMT), as the OMT may exceed the ECB’s mandate. Although the ECB QE launch date is several weeks away, there is no word yet from the German Constitutional Court on how they will decide.

QE may help boost the Eurozone’s economy in the short term. Nonetheless, the long-term effectiveness of such a program remains to be seen at this point. Some hedge funds do not seem to think highly about the success of Mr. Darghi’s QE and are anticipating the euro to be in parity with the U.S. dollar by the end of this year, or in early 2016.

S&P 500 Summary: 1.85% YTD as of 02/13/15

Outperforming Sectors: Materials 5.69% YTD, Telecommunication services 4.63% YTD, Consumer discretionary 3.62% YTD, Healthcare 3.26% YTD, Energy 2.87% YTD, Information technology 2.69% YTD and Consumer staples 1.89% YTD.

Underperforming Sectors: Industrials 0.79% YTD, Financials –1.34% YTD and Utilities –4.75%

YTD. |