|

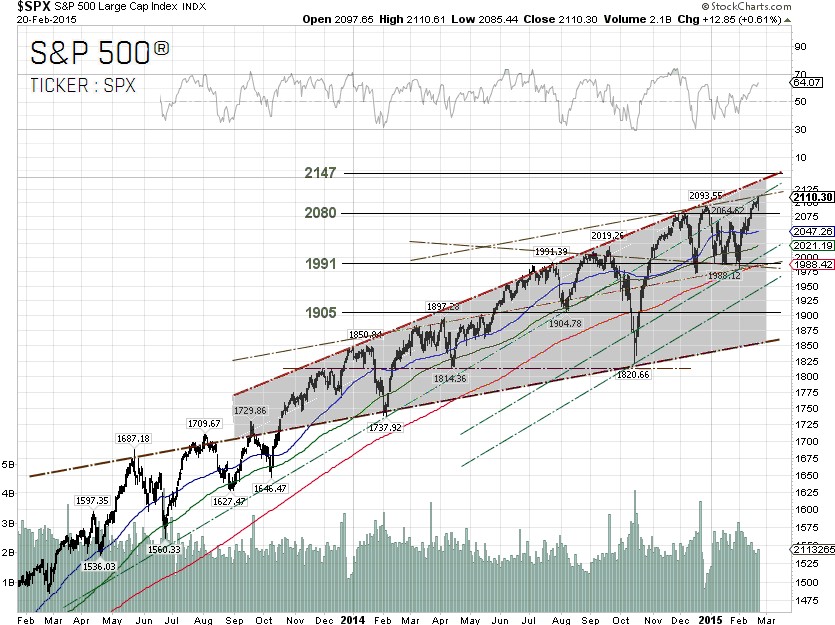

The S&P 500 closed at a record high of 2110.30 on Friday as Greek and European creditors agreed to a four month loan extension plan under the condition that the Greek government submits a preliminary list of proposed economic reforms by Monday night.

The proposed reform list will be used as the basis for negotiations until the end of April on a new financial settlement for Greece. If the EU rejects the Greek proposals on Monday, all bets would be off.

The 10-year U.S. Treasury yield has been on the rise, from 1.68% at the beginning of February to 2.13% at the close on Friday. The U.S. Treasury yield curve flattened as Wall Street increased its bets that the Fed could bump up its rate hike timetable to June. The Federal Reserve minutes, released on Wednesday, suggested otherwise, meaning that the Fed is thinking that it might be too soon to hike rates while the U.S. economy is still recovering.

Recent U.S. economic data supports the Fed’s argument as it shows no signs of a pick-up in consumer spending or retail sales, despite an improvement in the U.S. job market, upbeat consumer confidence, and cheaper gas prices.

The best performing sector for the week was S&P 500 Healthcare. Companies in the sector, including UnitedHealth Group [NYSE:UNH], Medtronic [NYSE:MDT], AbbVie [NYSE:ABBV] and Celgene [NYSE:CELG] were up between 2.91% to 6.52%.

S&P 500 Energy, the worst performing sector for the week, was down 2.45% as the WTIC crude oil price tumbled 3.65% for the week. Hedge funds have been counter-trading stocks in the healthcare sector and those in the energy sector since the crude oil debacle began.

It might be too early to try to catch a falling knife in the energy sector. The International Energy Agency (IEA) warned last week that the oil inventories of non-OPEC countries may approach a record 2.83 billion barrels by mid-2015, before cuts in capital expenditures begin to have a significant impact on production.

On Friday, Baker Hughes [NYSE:BHI], one of the world's largest oilfield services companies, issued its weekly report saying that the U.S. oil drilling rig count fell another 40 to 1,019 in the week ending February 20, down over 36% from the record highs of 1,609 set in October 2014.

No one knows whether the shutdown of over 600 rigs has had any significant impact on U.S. oil production, as the U.S. oil drilling rig count stood between 200 and 400 during the financial crisis in 2009.

The U.S. Energy Information Administration (EIA) said on Thursday that U.S. commercial crude oil inventories rose 7.7 million barrels last week to a record 425.6 million barrels, the sixth straight week of seasonal record levels. This massive build-up of crude oil inventory came on the heels of a reduction in the oil drilling rig count, capital expenditure cuts and layoffs.

From the technical viewpoint, the S&P 500 continues its up-trend in the bearish broadening ascending wedge pattern. The double bottom at around the 1991 level was confirmed last week and the technical projection for the S&P 500 is 2147. Of course, if the EU was to reject the Greek reform proposals on Monday, all bets would be off and the S&P 500 could have a major pullback.

The second headline risk from the Eurozone is ECB President Mario Draghi’s quantitative easing (QE), set to begin next month. As far as we understand, the ECB QE scheme is still facing some legal and political hurdles, largely from Germany.

In theory, it is still possible that the German Federal Constitutional Court in Karlsruhe could instruct the German Bundesbank not to cooperate with the ECB bond-purchasing program. The judges in Karlsruhe expressed serious doubts last year about the legality of the ECB’s bond-buying program, so-called Outright Monetary Transactions (OMT), as the OMT may exceed the ECB’s mandate.

Although the ECB QE launch date is several weeks away, there is no word yet from the German Constitutional Court on how they will decide as everyone is still waiting for the final OMT ruling from the European Court of Justice in Luxembourg.

S&P 500 Summary: 2.5% YTD as of 02/20/15

Outperforming Sectors: Materials 6.72% YTD, Healthcare 5.26% YTD, Consumer discretionary 4.42% YTD, Information technology 3.91% YTD and Telecommunication services 3.21% YTD.

Underperforming Sectors: Industrials 2.4% YTD, Consumer staples 2.0% YTD, Energy 0.42% YTD, Financials –1.24% YTD and Utilities –3.62%

YTD. |