|

The S&P 500 closed down slightly for the week at 2104.50 despite a downward-revised U.S. GDP, weak existing home sales and lower-than-expected core durable goods orders. The markets seemed to be more focused on the testimony of Federal Reserve Chair Janet Yellen, in remarks to U.S. Congressional Banking Committees this week, where she said that the Federal Reserve has no imminent plans for rate hikes.

The Fed’s Yellen, however, stated that the central bank may remove the term "patient" from its upcoming Fed monetary statement. The interest rate hike decision will be determined "on a meeting-by-meeting” basis depending if they are "reasonably confident" that inflation will pick up towards the Fed's annual 2.0% target.

One should be aware that the Federal Reserve no longer emphasizes the consumer price index (CPI) as its official 2.0% inflation target. Instead, it has adopted the personal consumption expenditures (PCE) index because it is more real-time economic data and covers a wide range of household spending.

The Fed is in a very tough position as Wall Street pundits are beating their drums for interest rate hikes, sooner rather than later. The Fed is at risk of losing its credibility if the U.S. economy falls backwards after a rate hike. Mr. William C. Dudley, president of the Federal Reserve Bank of New York, said on Friday that he sees reason for caution on how soon, or how quickly, to raise interest rates.

The National Association of Realtors (NAR) said on Monday that existing U.S. home sales declined 4.9% to an annual rate of 4.82 million units, the lowest level since last April, missing economists' expectations for a 4.97 million unit-pace. The NAR blamed a shortage of properties on the market as the primary reason for the sluggish home sales.

The U.S. Commerce Department said on Thursday that orders for durable goods rose 2.8% in January, beating the forecasts of 1.6%. The December orders were revised downward slightly from a decline of 3.4% to a decline of 3.7%.

Core durable goods orders, excluding volatile transportation items such as civilian aircraft, showed a more modest gain of 0.3 percent in January after a decline of 0.8% in December, missing forecasts of 0.5%.

Shipments of core durable goods, a number used to help determine the GDP each quarter, fell by 0.3% in January, missing the forecast of a 0.2% increase. A weak level of shipments would suggest slower growth in the first quarter than economists have projected.

The U.S. Bureau of Economic Analysis (BEA), the Commerce Department, said on Friday that the second estimate of real GDP in the fourth-quarter was revised downward from 2.6% to 2.2%, while the 2014 full-year real GDP was unchanged at 2.4%.

The revised fourth-quarter GDP beat the recent median forecast of 2.0%, based upon 83 economists surveyed by Bloomberg. It apparently didn’t mean much as just a month ago, the median forecast by Wall Street economists for the fourth-quarter GDP was 3.2%.

The worst performing sector for the week was S&P 500 Energy, down almost 2% for the week as crude oil prices tumbled 5.5% on Thursday, which prompted investors to dump energy companies. It might be too early to try to catch a falling knife in the energy sector as the crude oil prices have yet to find a bottom.

The U.S. Energy Information Administration said on Wednesday that the crude oil inventories increased by 8.4 million barrels to a total of 434.1 million barrels. Analysts had expected a build of about 3.6 million barrels. This is the seventh straight week of seasonal record levels. The massive build-up of crude oil inventory came on the heels of a reduction in the oil drilling rig count, capital expenditure cuts and layoffs.

On Friday, Baker Hughes [NYSE:BHI], one of the world's largest oilfield services companies, issued its weekly report saying that the U.S. oil drilling rig count fell another 33 to 986 in the week ending February 27, down over 38% from the record highs of 1,609 set in October 2014. No one knows whether the shutdown of over 600 rigs has had any significant impact on U.S. oil production.

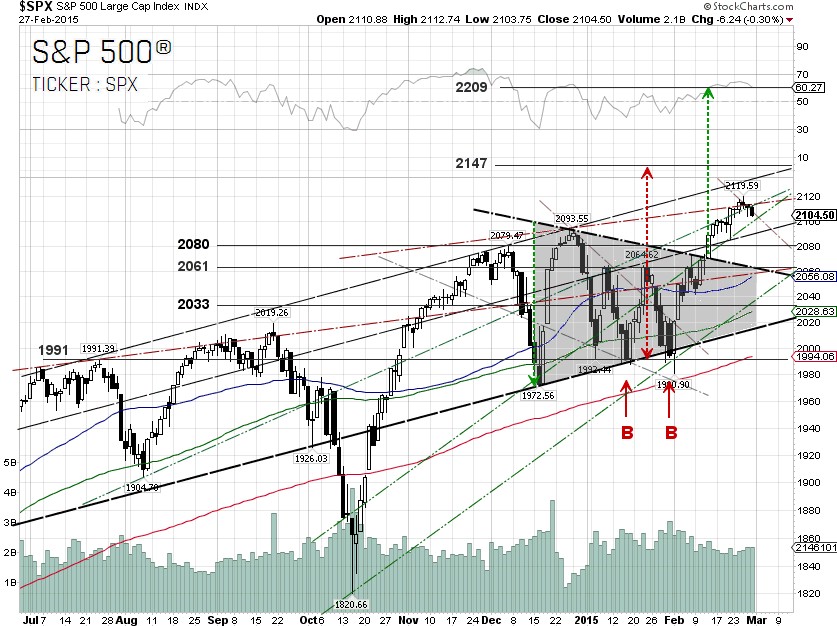

From the technical viewpoint, the S&P 500 continues its 16-month up-trend in the bearish broadening ascending wedge pattern. There are two near-term technical projections for the S&P 500. The first technical projection is 2147, based on the S&P 500’s confirmed double bottom at around the 1991 level about two weeks ago. The second technical projection, based on a symmetrical triangle breakout, is 2209.

According to Birinyi Associates, 22 Wall Street strategists are expecting the S&P 500 to gain an average of 8.2% this year and to finish at 2228.

The near-term headline risk is the jobs report on Friday. There are technical supports at 2080 and 2061, if the S&P decides to pull back.

S&P 500 Summary: 2.21% YTD as of 02/27/15

Outperforming Sectors: Materials 5.68% YTD, Healthcare 5.35% YTD, Consumer discretionary 5.06% YTD, Telecommunication services 4.2% YTD, Information technology 3.68% YTD and Consumer staples 2.85% YTD.

Underperforming Sectors: Industrials 1.32% YTD, Energy –1.55% YTD, Financials –1.74% YTD and Utilities –4.78%

YTD. |