|

The S&P 500 sold off 1.42% on Friday to close at 2071.26 as the Bureau of Labor Statistics (BLS), the U.S. Labor Department, said the U.S. economy added 295,000 jobs and the unemployment rate ticked down to 5.5% in February, exceeding economists’ expectations of a 240,000 jobs gain and an unemployment rate of 5.6%. For the week, the S&P 500 declined 1.57%.

Digging deeper into the jobs report, one may find that the underlying fundamentals of the job market are still weak as hourly wage growth in February increased just 2% from a year ago. The number is well below the 3.5-4.0% range that economists consider as the normal wage growth rate for the U.S. Federal Reserve to start hiking benchmark interest rates.

Although the labor force participation rate dropped from 62.9% last month to 62.8%, a record high 92.9 million Americans, aged 16 and older, still did not have a job or gave up looking for one in February, according to BLS data.

The Bureau of Economic Analysis (BEA), U.S. Commerce Department, said on Monday that personal spending fell 0.2% in January, worse than the expected decline of 0.1%. Weak consumer spending prompted analysts at Morgan Stanley to cut their first-quarter 2015 U.S. GDP growth estimate by five-tenths of a percentage point to a 2.3% annual pace, according to Reuters.

The BEA also said that the headline personal consumption expenditures (PCE) index for January increased only 0.2% year-on-year, compared to an increase of 0.7% in the previous month. The core PCE index came in at 1.3%, unchanged from the previous month, but well below the Federal Reserve’s inflation target of 2.0%.

One of the reasons for weak consumer spending, despite cheap oil prices, is because most of the U.S. job growth in the past several years is heavily concentrated in the low-wage service sector, like retail and food service.

The Wall Street pundits are beating their drums for interest rate hikes, sooner rather than later. We think that the Fed is at risk of losing its credibility if the U.S. economy falls backwards after a rate hike as the wage growth, consumer spending and inflation are still weak.

On Thursday, ECB president Mario Draghi unveiled the details of the 1 trillion-euro bond buying stimulus plan that will begin on Monday. The plan appeared to disappoint the currency market as the euro-dollar exchange rate dropped to an intraday low of 1.0986 dollars per euro after the announcement.

The euro-dollar exchange rate continued to reel on Friday after the release of the U.S. jobs report and traded at 1.0844 dollars per euro at the close on Friday, down 3.14% for the week. The currency traders are betting that the euro-dollar exchange rate heads to parity as the markets are in doubt that the latest ECB QE bond purchase program will prompt any meaningful economic recovery or counter the threat of deflation as the ECB hopes.

As of February 24, there are 266,552 short positions of euro FX

(CME.E6), traded on the Chicago Mercantile Exchange (CME), by asset manager/institutional and leveraged funds. This is compared to about 67,763 long positions, according to the Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) each Friday. Short positions have dropped about 4,242 contracts from the last report.

The U.S. dollar index (DXY) broke out the major technical head resistance at 96.2, or 50% Fibonacci retracement and closed on Friday at 97.67, up 2.46% for the week. The next major resistances are at 100, or a psychological resistance and 102.16, or 61.8% Fibonacci retracement. The strong U.S. dollar could drive the crude oil prices lower, hurt U.S. corporate profits and keep inflation even further away from the Federal Reserve’s target.

The worst performing sector for the week was S&P 500 Utilities, down almost 4% for the week as the bond yield rose. The 10-year U.S. Treasury yield surged 12% for the week to 2.24% or 50% Fibonacci retracement. The next major resistances are at 2.34% and 2.42%, or 38.2% Fibonacci retracement.

The money managers shifted their assets into the S&P 500 Financials after the release of the Federal Reserve’s “stress tests”. The nation’s largest banks appear to have the financial strength to be able to withstand the severely adverse economical and financial conditions set by the Federal Reserve.

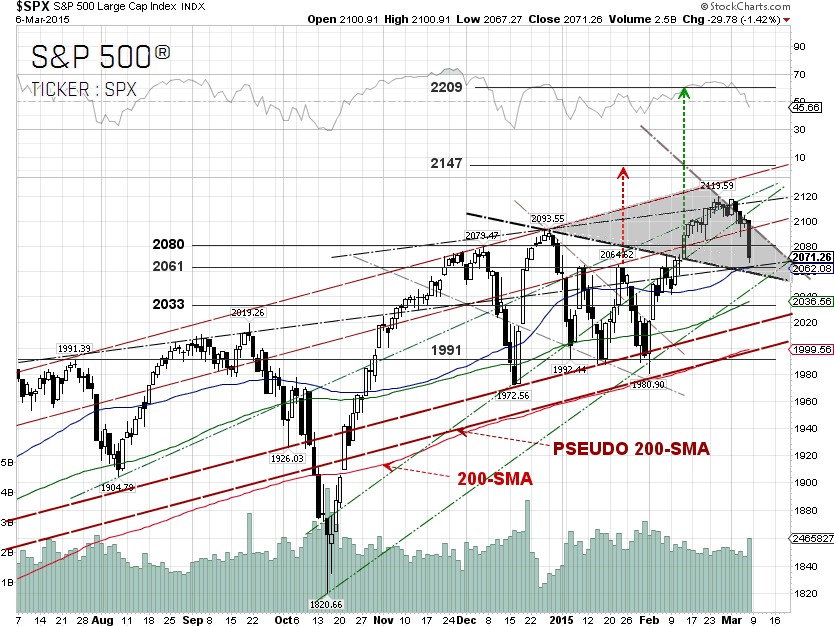

From the technical viewpoint, a falling wedge pattern may emerge in the S&P 500 chart pattern if the S&P 500 can bounce off the support trendline at around the 2056 level. A further pullback could send the S&P 500 to retest the 2033 level.

If market sentiment shifts from a potential June interest rate hike to September, the S&P 500 could bounce off one of the support trendlines at around the 2010 or 2000 levels. In the chart pattern, the pseudo 200-SMA, according to our definition, refers to the trendline which runs in parallel to the actual 200-SMA.

S&P 500 Summary: 0.6% YTD as of 03/06/15

Outperforming Sectors: Consumer discretionary 4.23% YTD, Healthcare 4.14% YTD, Materials 3.54% YTD, Information technology 2.2% YTD and Telecommunication services 1.28%

YTD.

Underperforming Sectors: Consumer staples 0.17% YTD, Industrials –0.55% YTD, Energy –4.42% YTD, Financials –2.28% YTD and Utilities –8.74%

YTD. |