|

The S&P 500 sank another 0.86% this week and closed on Friday at 2053.40 as the U.S. dollar index (DXY) broke out the psychological head resistance level of 100

for the first time in over 12 years. The DXY, a weighted geometric index of the value of the U.S. dollar relative to a basket of six major currencies, closed at 99.411, up 1.78% for the week. The market is increasingly concerned about the adverse impacts of the strengthening dollar on corporate profits.

The strength in the DXY reflects the signs of an improved U.S. labor market as the U.S. Department of Labor’s Job Openings and Labor Turnover Survey (JOLTS) report, released on Tuesday, showed that U.S. companies had 5 million job openings at the end of January, the highest level since January 2001.

The strong job openings report came on the heels of the previous Friday’s release of the February U.S. employment report by the Bureau of Labor Statistics (BLS), the U.S. Department of Labor, showing that the U.S. economy added 295,000 jobs and the unemployment rate ticked down to 5.5% in February, exceeding economists’ expectations of a 240,000 jobs gain and an unemployment rate of 5.6%.

Bullish DXY bets are also coming from currency traders who are anticipating that the EUR/USD will head to parity as the markets are in doubt that the latest ECB QE bond purchase program will prompt any meaningful economic recovery or counter the threat of deflation as the ECB hopes. Greece’s debt crisis is on the front burner again as Greece’s government is using tactics to slow down negotiations.

The worst performing sectors for the week were S&P 500 Energy and Information technology, down 2.69 and 2.44%, respectively. Hedge funds are increasingly bearish as crude oil prices fell below the key technical support level of U.S. $48.64 per barrel. Crude oil futures for delivery in April 15 [CLJ15.NYM] plunged almost 9.6% to close on Friday at U.S. $45 per barrel on the New York Mercantile Exchange (NYMEX).

On Thursday, Intel [NASDAQ: INTC] issued a revenue warning for the first quarter of 2015. The company lowered first-quarter revenue guidance to U.S. $12.8 billion from the prior guidance of U.S. $13.7 billion, citing weak PC demand, as small businesses put off upgrading their personal computers, and adverse impacts of the strengthening dollar. INTC plunged 6.81% to close at U.S. $30.93 per share for the week.

Bank of America Merrill Lynch came out and reiterated its underperform rating on Microsoft [NASDAQ:MSFT] stock following Intel’s warning, sending the stock down 2.31% for the week. Microsoft and Intel are in the top five constituents of the S&P 500 Information technology.

The best performing sectors for the week were S&P 500 Healthcare and Financials, up 0.47 and 0.4%, respectively. The money managers shifted their assets into the S&P 500 Financials again, after the release of the Federal Reserve’s results of “the second round of the stress tests”. U.S. branches of Germany’s Deutsche Bank and Spain’s Banco Santander flunked the tests, while Bank of America only got a conditional pass and will need to submit a new capital plan by September.

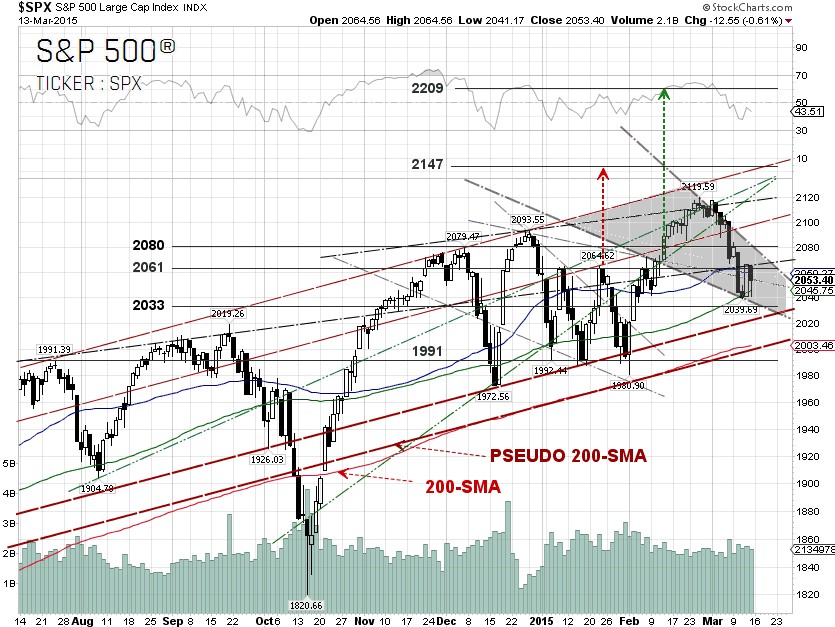

From our technical viewpoint, the S&P 500 bounced off the 100-day SMA and a bullish falling wedge pattern has now emerged. We believe that the Federal Reserve will think twice before making any major moves as the strong U.S. dollar could drive the crude oil prices lower, hurt U.S. corporate profits and keep inflation even further away from the Federal Reserve’s target.

A breakout of the falling wedge could take the S&P 500 to our projected target at 2147. There are two technical resistances at 2080 and at 2120. A further pullback could send the S&P 500 to retest the 2033 and 200-day SMA, respectively. In the chart pattern, the pseudo 200-SMA, according to our definition, refers to the trendline which runs in parallel to the actual 200-SMA.

The next headline risk is the Federal Open Market Committee (FOMC) meeting on March 17 and 18. The Fed may remove the term "patient" from its Fed monetary statement which might spook the global financial markets, particularly the emerging markets.

As the Fed said, the interest rate hike decision will be determined "on a meeting-by-meeting” basis depending if they are "reasonably confident" that inflation will pick up towards the Fed's annual 2.0% target.

One should pay attention to Greece’s debt crisis. Greece is again on the front burner as Greece’s government is using tactics to slow down negotiations and it is still possible that Greece will be booted out of the eurozone. This could send the DXY to close above the 100 psychological resistance and

probably retest the 102.16, or 61.8% Fibonacci retracement level.

S&P 500 Summary: –0.27% YTD as of 03/13/15

Outperforming Sectors: Healthcare +4.61% YTD, Consumer discretionary +3.87% YTD, Materials +2.2% YTD, Telecommunication services +0.69% YTD and Information technology –0.24% YTD.

Underperforming Sectors: Consumer staples –1.11% YTD. Industrials –1.28% YTD, Financials –1.88% YTD, Energy –7.11% YTD and Utilities –8.61%

YTD. |