|

The U.S. Labor Department said on Friday that the nonfarm payrolls for December surged by 252,000, beating economists’ forecasts of 240,000. The unemployment rate dropped to 5.6%. Although the headline number looks very decent, the underlying fundamentals of the job market are still weak.

First, hourly wages increased just 1.7% from a year ago, still lower than the wage inflation target of 3% that economists think the U.S. Federal Reserve would start hiking benchmark interest rates.

Second, the labor force participation rate dropped from 62.8% to 62.7% last month, a fresh 37-year low. That means over 90 million Americans, aged 16 and older, did not have a job or gave up looking for one in December.

Chicago Fed President Charles Evans, a voting member on the central bank's policymaking committee, told CNBC Friday morning that prices and wages need to rise to the Fed targets before he would feel better about the possibility of increasing rates. He practically repeated what was already published in the Fed minutes. Therefore, it was nothing new.

The U.S. Dollar index (DXY pronounced “Dixie”) surged to 92.4970, shy of the 52-week high at 92.5280, the highest reading since December 2005. The 10-year U.S. Treasury yield tumbled 2.46% to close at 1.98%. The next support for the 10-year U.S. Treasury yield is 1.77%. Just a reminder, the 10-year U.S. Treasury yielded between 1.50% and 2.00% during the 2012 Greek government-debt crisis.

The Volatility Index, or VIX, traded on the Chicago Board Options Exchange (CBOE), surged to 18.42 on Friday before pulling back and closed at 17.55. Although the VIX isn’t even near the 2012 Greek government-debt crisis level, meaning 40.00 or higher, the current VIX level is considered to be elevated. So, tighten your seat belts and prepare for more volatility.

Crude oil, which is traded in an inverse correlation with the US dollar, dropped to an intra-day low of U.S. $47.16 per barrel on Friday, before bouncing back. If the crude oil and energy sector goes, so goes the market.

Based upon Mr. Evans’ comments this morning, it is obviously not the U.S. nonfarm payrolls data that triggered the market sell off. The big decline on Friday in the 10-Year Treasury yield, as well as in the energy and financials sectors, suggests that the market is questioning whether the highly anticipated QE announcement by ECB President Mario Draghi will come through at the next ECB policy meeting on January 22.

In addition, Greece’s snap elections on January 25, which will determine whether Greece will stay or exit the Eurozone, could end up being another disaster for the global financial markets, similar to the European debt crisis in mid-2012.

As suggested by the VIX, volatility in the S&P 500 will be at an elevated level next week. On Wednesday, the Commerce Department will report U.S. retail sales for December and the U.S. Labor Department will report the CPI. Retailers will be announcing their same-store sales figures during the important holiday shopping season on Thursday. Decent numbers from these reports could calm the market down, or vice-versa. So be prepared!

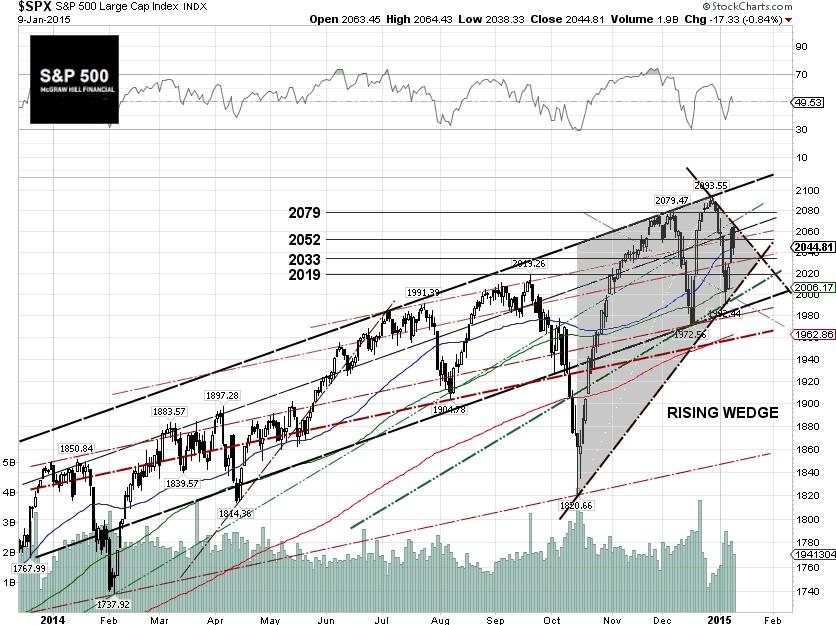

In the case that the S&P 500 continues to slide next week, the next support levels are 2033 and 2019.

S&P 500 Performance: -0.68% YTD (01/09/15)

Outperforming Sectors: Healthcare 2.68% YTD, Consumer staples 1.3%

YTD, Utilities 0.40% YTD, Information technology –0.33% YTD, Materials –0.40% YTD and Telecommunication services –0.62%

YTD.

Underperforming Sectors: Consumer discretionary –1.82 YTD, Industrials –2.18

YTD, Financials –2.39% YTD and Energy –3.18 YTD. |