|

The U.S. Commerce Department said on Wednesday that core retail sales excluding automobiles, gasoline, building materials and food services fell 0.4% last month after a 0.6% rise in November, the largest decline in 11 months. Economists had expected an increase of 0.4%.

Sales fell almost across the board, despite American consumers saving an estimated U.S. $14 billion on gasoline costs last year. Economists were way off the mark with their forecasts of retail sales. Some of them already started trimming their Q4 2014 GDP growth forecasts by as much as 0.3%. The mean GDP growth forecast is now printed at between a 3.0 and 3.4% annual pace.

The Q4 U.S. GDP could potentially dip below 3.0% if capex spending and investment cuts announced by the companies in the energy and industrial sectors are included.

December's decline in retail sales took down the broader U.S. equity markets along with it. The S&P 500 consumer discretionary sector dipped 1.66% for the week as investors rotated out of that sector and into defensive sectors. Investors were buying the consumer staples, healthcare and utilities sectors as they see a deceleration of the U.S. economy ahead.

Three out of the four biggest U.S. banks, J.P. Morgan Chase & Co. [NYSE:JPM], Bank of America [NYSE:BAC] and Citigroup [NYSE:C] posted disappointing results this week, citing falling profits and sluggish revenue that missed analysts’ estimates. Only Wells Fargo & Company [NYSE:WFC] reported rising profits and revenue that beat estimates.

Investors decided to get out the financials sector and rotated elsewhere, as it is still unknown about the actions of the Swiss National Bank (SNB) to discontinue its exchange rate of 1.20 Swiss francs per euro.

The market is questioning whether the highly anticipated QE announcement by ECB President Mario Draghi will come through at the next ECB policy meeting on January 22. S&P 500 financials sold off 2.61% for the week and is now the worst performing sector in the S&P 500 year to date.

Overall, the S&P 500 index was extremely volatile as it was an option-expiration week, meaning the third week of the month when stock options expire after the market closed on the Friday.

The S&P 500 energy sector, which trades along with the crude oil prices, slid 1.46% for the week as the crude oil prices gyrated with option-expiration on Wednesday and short coverage on Friday, as Monday is a U.S. holiday.

The U.S. Dollar index (DXY “Dixie”) surged to 93.57 and took out the 92.22 technical resistance, the highest reading since the end of 2004. The 10-year U.S. Treasury yield tumbled to 1.77% before bouncing back and closed at 1.83%. Just a reminder, the 10-year U.S. Treasury yielded between 1.50% and 2.00% during the 2012 Greek government-debt crisis.

The Volatility Index, or VIX, traded on the Chicago Board Options Exchange (CBOE), surged to 23.43 on Friday before pulling back and closed at 20.95. Although the VIX isn’t even near the 2012 Greek government-debt crisis level, meaning 40.00 or higher, the current VIX level is considered to be elevated. The next resistance for VIX is 24.5. So, tighten your seat belts and prepare for more volatility.

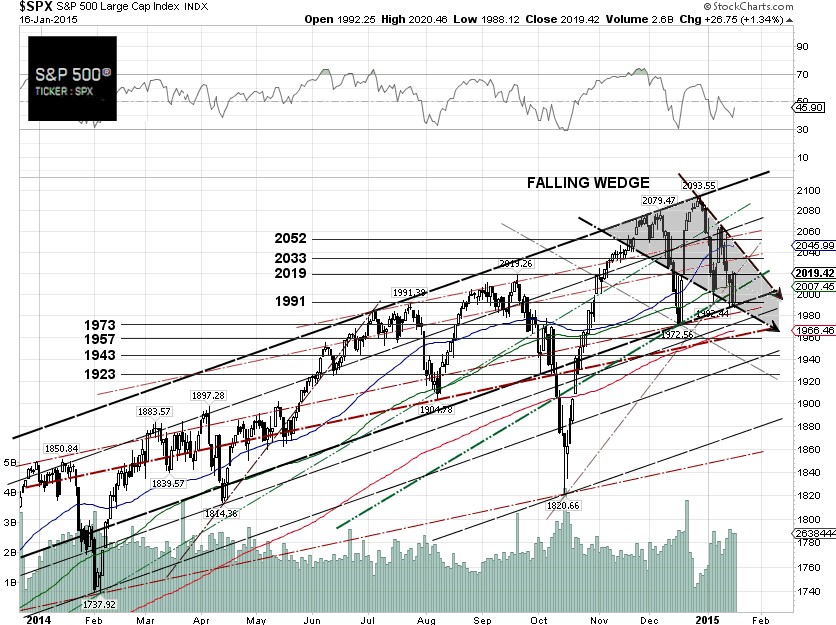

The bullish falling wedge is now emerging. In the case of a S&P 500 rebound next week, the technical head resistances are 2033 and 2052. If the S&P 500 continues to slide, the next support levels are 1966.46 (200-day SMA), 1957.46 (1-year 38.2% Fibonacci retracement), 1943 and 1923.

S&P 500

Summary: –3.1% YTD as of 01/30/15

Outperforming Sectors: Utilities 2.34% YTD, Healthcare 1.17% YTD, Consumer staples –1.27% YTD, Materials –1.99% YTD and Telecommunication services –2.24% YTD.

Underperforming Sectors: Consumer discretionary –3.14% YTD, Industrials –3.69% YTD, Information technology –3.91% YTD, Energy –4.88% YTD and Financials –6.99%

YTD. |