|

The International Monetary Fund (IMF) trimmed the 2015 global growth forecast on Wednesday by 0.3% to 3.5%, citing deflation and a slowdown in consumer spending. The IMF revised the U.S. economic growth forecast upwards to 3.6%, citing improved real incomes and consumer sentiment, boosted by cheap oil. If the IMF forecast is correct, it will be the highest U.S. GDP reading since 2005.

One may want to be cautious with the IMF forecast as U.S. core retail sales excluding automobiles, gasoline, building materials and food services, fell 0.4% in December, the largest decline in 11 months, despite cheaper gasoline prices.

The nearly 60% drop in crude oil prices, since June, has prompted companies in energy related sectors to cut capital expenditure spending and to layoff workers. One of the largest U.S. oil & gas service companies, Baker Hughes [NYSE:BHI], announced last week that they will layoff 7,000 workers, or 11% of its work force, due to lack of demand. The cuts in capex spending and mounting layoffs may not yet be calculated in many of the economic forecasts for GDP.

The European Central Bank (ECB) announced an aggressive open-ended government bond-purchasing program on Thursday, worth about 60 billion euros per month, starting in March 2015 and continuing through September 2016, or until inflation rates in the Eurozone are close to 2%.

As part of the plan, the ECB would purchase up to 20% of the bonds while the central banks of the Eurozone countries would buy the rest. According to Bloomberg after the ECB annoucement, Bundesbank President Jens Weidmann and Executive Board member Sabine Lautenschlaeger privately said that they were against implementing such a plan now.

One shouldn’t count on anything just yet since, in theory, it is still possible that the German Federal Constitutional Court in Karlruhe could instruct the German Bundesbank not to cooperate with the ECB bond-purchasing program.

A conservative Bavarian politician and lawyer, Peter Gauweiter, is already preparing a legal complaint against the ECB bond-purchasing program. Other legal cases could mount, similar to that of the middle of the European debt crisis in 2012.

Quantitative easing (QE) may help boost the economy in the short term. Nonetheless, the long-term effectiveness of such a program remains to be seen at this point.

Despite the announcement of an aggressive open-ended government bond-purchasing program by the ECB, investors are still viewing the S&P 500 consumer staples, healthcare and utilities sectors as “Safe Havens”. The consumer discretionary and financials sectors are doing poorly as a deceleration of the U.S. and global economy still remains a major concern.

Notable large cap, multi-national, U.S. corporations including UPS [NYSE:UPS], Kimberly-Clark [NYSE:KMB] and McDonald’s [NYSE:MCD] posted disappointing results this week, citing falling profits and sluggish revenue that missed analysts’ estimates. UPS, KMB and MCD are S&P 500 component stocks in the industrials, consumer staples and consumer discretionary sectors, respectively.

The U.S. Dollar index (DXY pronounced “Dixie”) surged to 94.76, the highest reading since August 2003. The DXY next resistance will be at 96.27, or 50% Fibonacci retracement. Currency traders believe the DXY could retest the 100 level in the near future.

The strong U.S. dollar is not doing any good for U.S. corporations such as Johnson & Johnson [NYSE: JNJ], McDonald’s and Kimberly-Clark as their sales and profits got hit last quarter by unfavorable foreign-currency exchange rates.

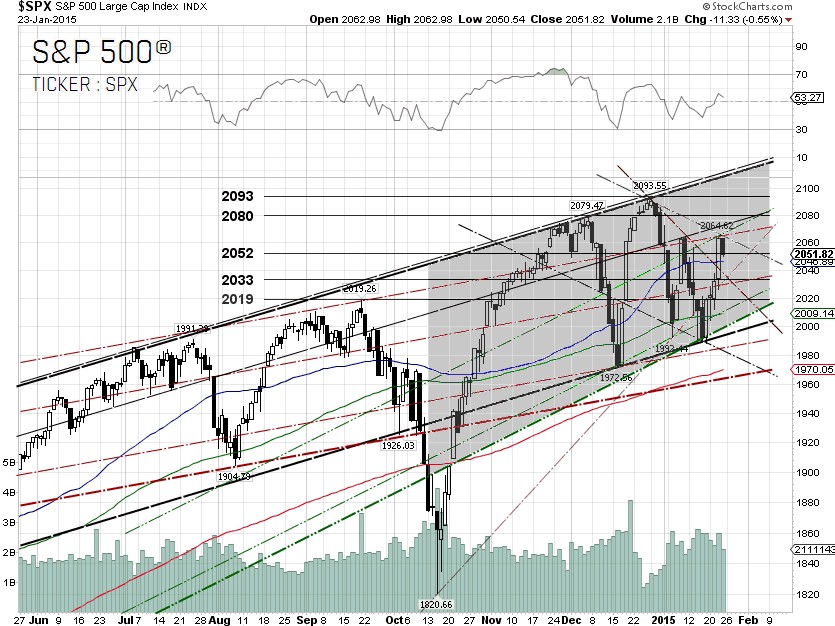

The S&P 500 rebounded off the trend line and broke out of the falling wedge before pulling back to close on Friday at the 2052 support level. The next head resistances are 2080 and 2093, or the S&P 500’s all-time high.

It looks like we might be heading into a rough ride next week as the anti-austerity, Syriza party, won the Greek election. It is possible that Greece could exit the Eurozone if they don’t comply with the 2012 bailout agreement. Let’s see how this Greece saga goes.

Lower-than-expected earnings, an unfavorable outcome from the Federal Reserve meeting and a weaker-than-forecasted Q4 U.S. GDP, to be reported on Friday, could push the S&P 500 back to the support levels of 2033, 2019 and 1991.

S&P 500

Summary: –0.34% YTD as of 01/23/15

Outperforming Sectors: Utilities 4.17% YTD, Healthcare 3.71% YTD, Consumer staples 2.28% YTD, Telecommunication services 0.13% YTD and Information technology 0.22% YTD.

Underperforming Sectors: Materials –0.79% YTD, Industrials –1.2% YTD, Consumer discretionary –1.83% YTD, Energy –3.12% YTD and Financials –3.84%

YTD. |