|

The S&P 500 pulled back 0.65% on Monday after the market digested the U.S. non-farm payroll report released the previous Friday. The U.S. Bureau of Labor Statistics (BLS) said that the U.S. government and private businesses added 280,000 jobs in May to the U.S. economy, better than expectations. Economists had been expecting a gain of 225,000 jobs. Strong jobs reports in coming months could trigger the first rate hike by the U.S. Federal Reserve, sooner rather than later.

The U.S. Job Openings and Labor Turnover (JOLT) report released by the BLS on Tuesday said that the number of job openings rose to 5.4 million on the last business day of April, the highest since the series began in December 2000. Over the 12 months ending in April 2015, hires totaled 60.0 million and separations totaled 57.2 million, yielding a net employment gain of 2.8 million.

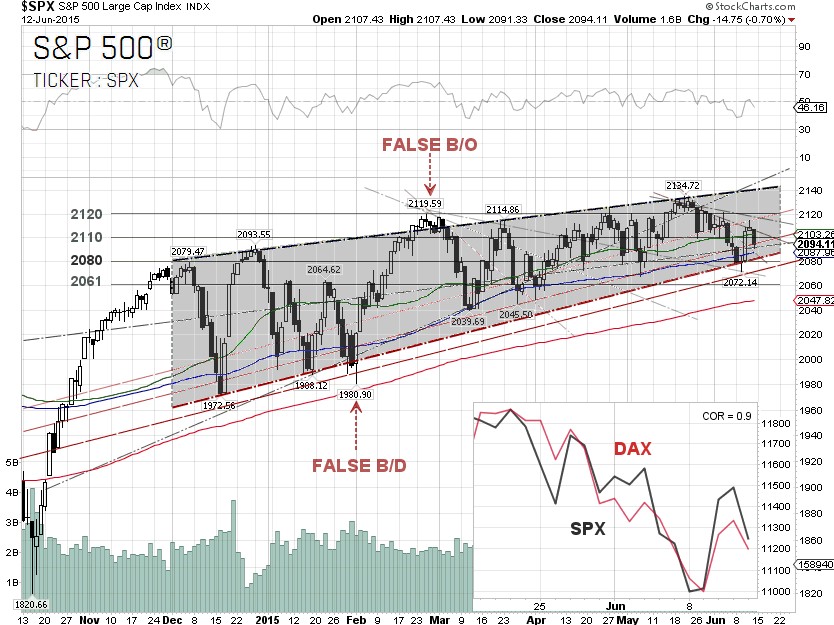

According to the BLS data, the U.S. government and private businesses added 3.62 million jobs in the past 12-months ended May 2015. The S&P 500 responded marginally to the JOLT report but managed to bounce off the trendline support and closed above the 2,080 technical support level.

Mr. Kaushik Basu, the World Bank's chief economist, said on Wednesday that they lowered the growth outlook for the United States to 2.7% this year, from 3.2% in January, and to 2.8% next year, from a previous forecast of 3%. He also said that the Federal Reserve should hold off on a rate hike until next year to avoid worsening exchange rate volatility and crimping global growth.

Last week, Ms. Christine Lagarde, the Managing Director of the International Monetary Fund (IMF), had also urged the Federal Reserve to delay raising interest rates until at least next year. The IMF had just lowered its forecast for growth in the U.S. to 2.5% in 2015, down from the previous forecast of 3.1% growth.

The S&P 500 shrugged off the World Bank’s downgrade and refocused its attention to German Chancellor Angela Merkel’s comment out of Brussels, saying “The goal is to keep Greece in the euro area.” According to Bloomberg, Germany’s negotiators might willing to accept just one large reform from Greece to unlock the €7.2 billion in bail-out funds. The S&P 500 rallied 1.2% as the markets bet that the standoff between Greece and its creditors was over.

The U.S. Commerce Department said on Thursday that May retail sales climbed a seasonally adjusted 1.2%, beating economists’ forecast of a 1.1% gain in a poll by Reuters. The core retail sales excluding automobiles, gasoline, building materials and food services increased 0.7% in May, also beating the expectations of a 0.5% gain. The S&P 500 responded to the retail sales data mutedly, as it gained just 3.66 points on Thursday.

The global stock markets sold off on Friday as the International Monetary Fund (IMF) delegation left negotiations in Brussels late Thursday and flew home because of major differences with Athens. One of the differences was a long list of new demands from Greece, including funds from the European Stability Mechanism, to repay about €6.7 billion of bonds held by the ECB that come due in July and August.

The European Union is now telling Greek Prime Minister Alexis Tsipras to stop gambling. With all these new demands from Greece, the tensions are also rising in Berlin with a growing number of German lawmakers committed to voting against a third bailout for Athens.

For the week, the U.S. dollar index inched 1.43% lower to close at 94.987 on Friday. One of the reasons for the decline in the U.S. dollar index could be due to a Bloomberg news wire report on Monday saying that President Barack Obama had told a Group of Seven industrial nations summit that the strong dollar was a problem. A senior U.S. official, as well as Mr. Obama himself, later denied that the comment was made.

Nonetheless, the U.S. dollar index closed on Monday at 95.323, down 1.08% for the day, losing all of its 0.91% gain on the previous Friday, after the May U.S. non-farm payroll report. The 10-year U.S. Treasury yield dropped 0.83% for the week to close at 2.39% on Friday. The S&P 500 closed at 2,094.11 on Friday, up 1.28 points for the week.

The best performing S&P 500 sector for the week was again Financials, up 0.99% on the top of a 0.76% gain last week, as the profit margins for banks improve when the difference between short-term interest rates and long-term yields widens. The worst performing sectors for the week were Energy and Information Technology, down 0.9% and 0.75%, respectively. The Energy sector took a nose dive on Friday after Saudi Arabia said the kingdom is ready to raise oil output even further to meet demand. Saudi Arabia already increased its production in May to around 10.3 million barrels per day, its highest rate on record.

The Information Technology sector, including Apple [NASDAQ:AAPL] and Microsoft [NASDAQ:MSFT] were down 1.15% and 1.03%, respectively on Friday due to profit taking. eBay [NASDAQ:EBAY] was down 5.08% for the week after it issued its sales guidance for 2015 and 2016, which was below the Street's forecast. Yahoo! [NASDAQ:YHOO] was down 5.33% for the week after analysts said the proposed tax-free spin-off of Alibaba Group Holding [NYSE:BABA] is unlikely to be approved by the Internal Revenue Service and the Treasury Department.

The S&P 500 has been highly correlated with the German DAX, with correlation of 0.9, since mid-May as the Greece debt drama unfolds. Hard economic data seems to be marginally priced into the S&P 500. From our technical viewpoint, a rising wedge chart pattern has now emerged, as the S&P 500 bounced off the lower trendline support at 2,080. The index could make a pullback further next week, as the Greece debt negotiations seemed to fall apart and next week’s U.S. Federal Reserve meeting looms.

The S&P 500’s next move could also depend upon the yield of the U.S. 10-year Treasury note, which has been trading, of late, in an inverse correlation with the S&P 500. The 10-year Treasury yield broke out its trendline resistance at 2.41% and tested the head technical resistance at 2.5% on Wednesday. The next head resistance for the 10-year Treasury yield is 2.66%, or the 23.6% Fibonacci retracement level. The near-term technical supports for the S&P 500 are 2,092 and 2,084, or the 100-day SMA, 2,080, 2,070 and 2,061.

The headline risk when the market opens on Monday is the Greece debt drama. It seems like the negotiations between Greece, the ECB and IMF creditors are falling apart as the Greece government is acting irresponsible with new demands while holding the global financial markets hostage. The second headline risk is the two-day U.S. Federal Reserve meeting on Tuesday and Wednesday. With all the Greek drama and the wobbling U.S. economy, no one expects the Fed to increase the benchmark U.S. interest rate at this meeting.

Next week also has quadruple-witching options expiration in the U.S. equity markets where four types of standardized contracts, including stock options, stock index options, stock index futures, and single stock futures, all expire on Friday after the market close. It is typically very volatile, especially when the liquidity is low.

S&P 500 Summary: +1.71% YTD as of 06/12/15

Barclay Hedge Fund Index: +4.52% YTD

Outperforming Sectors: Healthcare +8.37% YTD, Consumer discretionary +5.81% YTD, Materials +2.85% YTD and Information technology +2.83% YTD.

Underperforming Sectors: Financials +.92% YTD, Telecommunication services +0.73% YTD, Industrials –1.20% YTD, Consumer staples –1.66% YTD, Energy –4.43% YTD and Utilities –10.73%

YTD. |