|

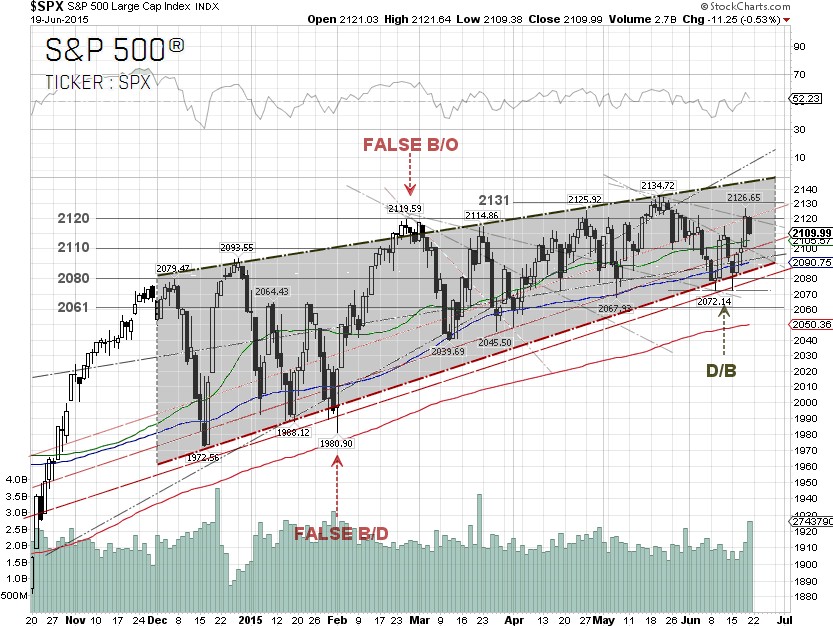

The S&P 500 sold-off 1.03% on Monday to an intra-day low of 2,072.49 before bouncing off the double-bottom as the previous day’s meeting in Brussels between Greece and its creditors crumbled after just 45 minutes. The U.S. Census Bureau released the May housing starts on Tuesday showing a drop in housing starts of 11.1%, to an annualized pace of 1.04 million. Economists had forecast housing starts to fall by 4%, to an annualized pace of 1.09 million in May. The market shrugged off the disappointing news from the housing sector and was focusing on the interest rate decision due from the U.S. Federal Reserve.

The U.S. Federal Reserve concluded its two-day Federal Open Market Committee (FOMC) meeting on Wednesday and announced that they sharply downgraded their economic forecast for this year to between 1.8% and 2.0%, from the previous forecast in March of between 2.3% to 2.7%. Fed Chair Janet Yellen, however, sounded hawkish at the press conference as she said the rate hikes are coming. Ms. Yellen insisted the timing will be dependent on statistics in real time.

On Thursday, the S&P 500 surged 1.25% to a intra-day high of 2,126.65 after the Bureau of Labor Statistics, the U.S. Department of Labor, said that the May Consumer Price Index (CPI) was unchanged from a year ago, in-line with Wall Street economists, according to Reuters. The core CPI for all items less food and energy rose by 1.7% in May over the last year, missing the forecast of 1.8% on a year-on-year basis. The market was confident that the Fed’s rate hike may be off the table for now as the CPI data came in weaker than expected.

Actually, the Federal Reserve no longer emphasizes the CPI as its official 2.0% inflation target. Instead, it has adopted the personal consumption expenditures (PCE) index, particularly the core PCE with the volatile prices of food and energy stripped out.

The Bureau of Economic Analysis (BEA), the U.S. Department of Commerce, will release the May personal income and outlays, including the PCE data, on June 25. The analysts at Bank of America Merrill Lynch expect the May core PCE price index, excluding food and energy, to increase 1.2% from a year ago, well below the Fed’s inflation target of 2.0%.

The S&P 500 pulled back 0.53% on Friday after the EU finance ministers in Luxembourg on Thursday, failed to bridge the gap between Greece’s leftist government and its lenders. On Friday, the ECB approved an increase of €1.75 billion in emergency loans to keep Greece’s banking system afloat. The market was very volatile on Friday, as it was the quadruple-witching options expiration after the close.

For the week, the U.S. dollar index inched 0.74% lower to close at 94.272 on Friday, down for the third straight week. The 10-year U.S. Treasury yield tumbled 5.44% for the week to close at 2.26% on Friday, down for the second straight week. The S&P 500 closed at 2,109.99 on Friday, up 0.76% for the week.

The best performing S&P 500 sectors for the week were Healthcare and Consumer discretionary up 2.18% and 1.66%, respectively. S&P 500 Healthcare has been the best outperforming sector this year, up 10.55% year-to-date. TripAdvisor [NASDAQ:TRIP], constituent of S&P 500 Consumer discretionary, jumped 19.49% for the week after a report about an Instant Booking deal with Marriott International [NASDAQ:MAR].

The worst performing sector for the week was Energy, down 0.44%. Although WTI crude dropped just 0.42% to $59.69 per barrel this week, shares of constituents of the S&P 500 Energy sector, including Baker Hughes [NYSE:BH] and ConocoPhillips [NYSE:COP] tumbled 3.45% and 1.83%, respectively.

From our technical viewpoint, a rising wedge chart pattern is still intact as the S&P 500 bounced off the short-term support level, at 2,072, on Monday, forming a short-term double-bottom. The S&P 500’s next move could also depend upon the yield of the U.S. 10-year Treasury note, which has been trading, of late, in an inverse correlation with the S&P 500. The 10-year Treasury yield failed to break through the head technical resistance at 2.5%, and is now on the descent.

If the 10-year yield continues to fall further, the next supports are at 2.23% and 2.04%, or the 50% and 61.8% Fibonacci retracement levels, respectively. For the S&P 500, the next trendline head resistances are 2,130 and 2,150.

The headline risks for next week are the Greek debt crisis and important U.S. economic data, including the GDP and the core PCE. The Greek debt crisis is now in full-blown mode. Greece needs the funds to make a €1.5 billion repayment to the International Monetary Fund by June 30. There will be an EU leaders emergency summit in Brussels on Monday, June 22. This could be the last ditch attempt to save Greece from falling into a default. Some eurozone officials believe Greek Prime Minister Alexis Tsipras may want to strike a deal at the summit.

The final reading of the first quarter U.S. GDP and the May personal income and outlays, including the PCE data, will be released on June 24 and June 25, respectively.

S&P 500 Summary: +2.48% YTD as of 06/19/15

Barclay Hedge Fund Index: +4.58% YTD

Outperforming Sectors: Healthcare +10.55% YTD, Consumer discretionary +7.47% YTD, Materials +3.46% YTD and Information technology +3.11% YTD.

Underperforming Sectors: Telecommunication services +1.38% YTD, Financials +0.83% YTD, Consumer staples + 0.22% YTD, Industrials –1.18% YTD, Energy –4.87% YTD and Utilities –9.42%

YTD. |