|

All eyes were on Greece, the Fed rate hike and the Russell Index annual rebalance at the close on Friday. Russell Investments adjusts the component companies in its Russell 1000, 2000 and 3000 indexes in June every year to keep up with the rise and fall of U.S. corporations. About $5 trillion in assets benchmark their performance to Russell's various indexes. Although Russell Investments announced its 2015 schedule for its annual reconstitution process in early March, the process may create additional U.S. market volatility in late June.

The probability of a September Fed rate hike increased somewhat after the Bureau of Economic Analysis (BEA), U.S. Commerce Department, said on Wednesday that the final reading of the U.S. first-quarter gross domestic product (GDP) was revised to a contraction of 0.2% at an annual rate, versus a previous estimated decline of 0.7%. The revision, in line with forecasts, was made as exports dropped less than previously estimated as well as a bigger increase in consumer spending.

The BEA said on Thursday that U.S. consumer spending surged a seasonally adjusted 0.9% in May, beating economists’ forecast of a 0.7% rise. The May core PCE price index, excluding food and energy, came in at a 1.2% increase from a year ago, in line with analysts at Bank of America Merrill Lynch, but well below the Fed’s inflation target of 2.0%.

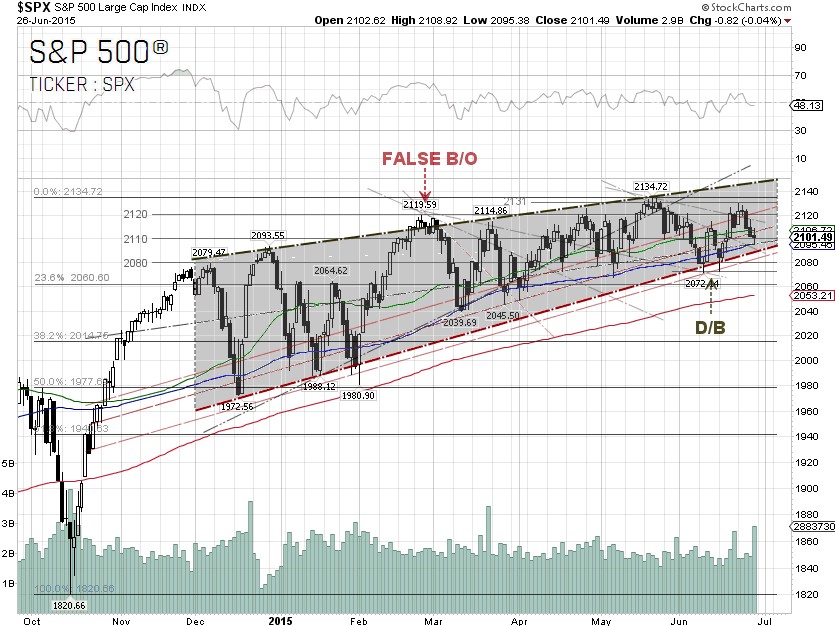

For the week, the U.S. dollar index surged 1.46% higher to close at 95.651 on Friday, after three straight weeks of declines. The U.S. dollar index is now trading underneath the 50-day SMA. The 10-year U.S. Treasury yield surged 10.18% for the week to close at 2.49% on Friday, bucking the two week downtrend. The S&P 500 closed at 2101.49 on Friday, down 0.4% for the week.

The best performing S&P 500 sectors for the week were Telecommunication services and Consumer discretionary, up 1.17% and 0.5%, respectively. Money managers could buy and sell shares of the stocks in both sectors to align their portfolios with the annual update of the Russell indexes.

The worst performing sectors for the week were Utilities and Materials, down 2.19% and 1.91%, respectively. E I Du Pont De Nemours [NYSE:DD] took a 6.07% a nosedive as DD was downgraded by JP Morgan. Monsanto [NYSE:MON] tumbled 6.59% after giving their third quarter outlook that was below consensus estimates. Both companies are S&P 500 Materials bellwethers. Utility stocks, including Duke Energy [NYSE:DUK] and Dominion Resources [NYSE:D], dropped 3.01% and 1.15%, respectively, as the bond yields rose.

From our technical viewpoint, a rising wedge chart pattern is still intact as the S&P 500 was unable to break through the 2,131 head resistance on Monday. The index, however, bounced off the 100-day SMA, on Friday as Greek default looms and the Russell Index Annual rebalanced. Nonetheless, the Greek debt drama seems to have no end in sight, despite the fact that Greece needs the funds to make a €1.5 billion repayment to the International Monetary Fund (IMF) by June 30.

Greece’s creditors, including the eurozone, European Central Bank (ECB) and the IMF, proposed a five-month bailout extension but it was rejected by Greek Prime Minister Alexis Tsipras. Mr. Tsipras accused the creditors of using “unacceptable” tactics employed by interlocutors representing foreign lenders at the EU, ECB and IMF. This might be a set-up for a sell-off next week.

In the event of a rising wedge breakdown, the projected price is around 1,980, or the 50% Fibonacci retracement level. There are several supports between 2,101.49 and 1,980. One should keep in mind that the risk that a crisis spreads into the global financial system and bond markets may be limited, as about 83% of Greek government debt is now held by official creditors, not by banks and private sector institutions.

S&P 500 Summary: +2.07% YTD as of 06/26/15

Barclay Hedge Fund Index: +4.48% YTD

Outperforming Sectors: Healthcare +10.89% YTD, Consumer discretionary +7.97% YTD and Telecommunication services +2.55% YTD.

Underperforming Sectors: Information technology +2.06% YTD, Materials +1.55% YTD, Financials +0.74% (+0.83%) YTD, Consumer staples –0.41% YTD, Industrials –2.36% YTD, Energy –4.99% YTD and Utilities –11.61%

YTD. |