|

The S&P 500 gave up 2.23% for the week to close on Friday at 2061.02, barely positive for the year, after a batch of mixed economic data and the announcement by SanDisk [NASDAQ:SNDK], a flash memory maker, that the company slashed its sales outlook. The National Association of Realtors said on Monday that existing home sales rose 1.2% to an annual rate of 4.88 million units, missing economists’ forecasts for a 4.9 million unit pace.

The EUR/USD traded at 1.0969 euros per dollar, up 0.42% on Tuesday as Markit's flash composite Purchasing Managers' Index (PMI) showed that the eurozone’s recovery is gathering momentum. The surveys of more than 5,000 businesses across the eurozone said that the activity in the manufacturing and services sectors rose to a 46-month high of 54.1 in March, from 53.3 in February. A reading above 50.0 indicates activity is increasing.

The U.S. Census Bureau, the Commerce Department, said on Wednesday that the new orders for manufactured durable goods dropped 1.4% in February, missing expectations for a 0.4% gain. The January orders were revised downward to a 2.0% increase from a previously reported of 2.8% gain. Core durable goods orders, excluding transportation, dropped 0.4% in February, missing forecasts for a 0.3% gain, while the January orders were revised downward from a flat reading to a 0.7% decrease.

Shipments of core capital goods, which are used to calculate the gross domestic product (GDP), were up 0.2% in February, below forecasts for a 0.3% gain, while January numbers were revised downward from a decline of 0.3% to a 0.4% drop.

The soft durable goods orders report, particularly in the shipments category, prompted Barclays ADR [NYSE:BCS], JPMorgan Chase & Co [NYSE:JPM], Morgan Stanley [NYSE:MS] and Goldman Sachs [NYSE:GS] to downgrade its estimate of U.S. economic growth in the first quarter.

JPMorgan economist Michael Feroli revised his estimate downward for first-quarter U.S. GDP to 1.5% from 2.0%, while Goldman Sachs economist Kris Dawson lowered his forecast to 1.8% from 2.0%. The Bureau of Economic Analysis (BEA), the Commerce Department, will release the first-quarter GDP advance estimate on April 29.

The worst performing sectors for the week were S&P 500 Financials, Healthcare and Information technology. Investors rotated their assets out of the financial sector, as borrowers have a harder time making loan payments in a soft economy and banks have more non-performing assets. Biotech stocks, part of S&P 500 Healthcare, took a hit for the week due in part to a sector correction and in part to profit taking.

The semicondutor sector, part of S&P 500 Information technology, on the other hand, sold off after SanDisk announced that they lowered their sales forecast to U.S. $1.3 billion from previous guidance between U.S. $1.4 and 1.45 billion, citing product delays, lower-than-expected sales and lower pricing. The Information technology sector bounced back somewhat on Friday after a rumor that Intel [NASDAQ:INTC] may buy its foundry customer, Altera [NASDAQ:ALTR], for U.S. $10 billion.

The S&P 500 Energy sector dropped just 0.69% for the week, despite the U.S. Energy Information Administration (EIA) weekly report, early Wednesday, showing that crude oil inventories had a build of 8.17 million barrels to a total of 466.7 million barrels, the highest since the EIA began keeping a weekly record. Analysts had expected a build of about 5.17 million barrels. Speculators ran up the oil price 7.39% in four days, blaming the Yemen conflict for the reason.

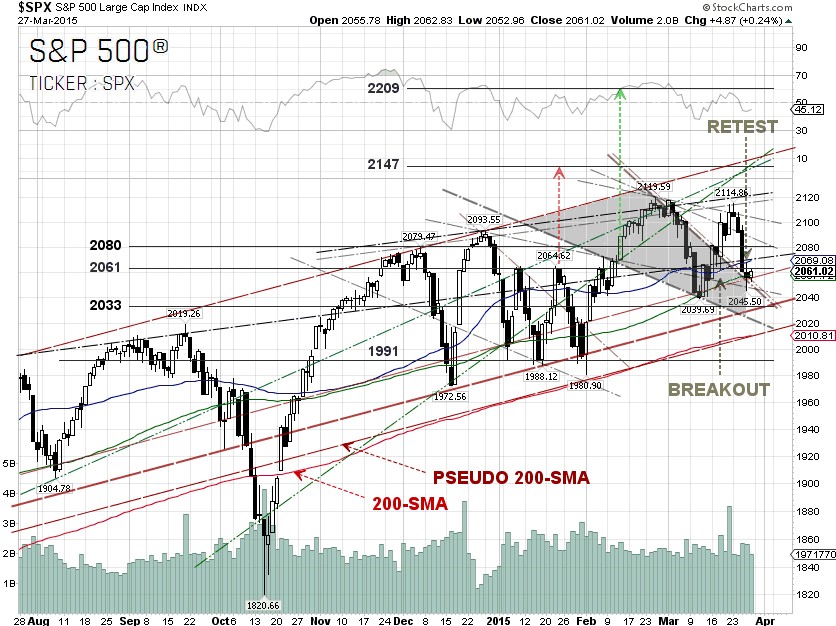

From the technical viewpoint, the S&P 500 pulled back to the trendline support at 2055 level after a batch of bad economic data. The Moving Average Convergence/Divergence (MACD), which now crossed below the signal line and formed a bearish crossover, may again be sending a sell signal. If the S&P manages to bounce off the trendline support next week and break out the 2080 level, the S&P could move higher towards our near-term projected target of 2147. There are technical supports at 2033 and 2020, if the S&P decides to pull back.

The headline risk for next week is the unemployment report, due to be released on Friday. If the unemployment rate inches lower towards 5%, the U.S. Federal Reserve may be forced to accept the fact that the Phillips curve doesn't work anymore. Hence, the Fed could gradually start to hike the rate despite that inflation is still below the 2% Fed target.

In economics, the Phillips curve is a historical inverse relationship between rates of unemployment and corresponding rates of inflation that result in an economy. That means decreased unemployment, or increased levels of employment, in an economy will correlate with higher rates of inflation.

S&P 500 Summary: +0.1% YTD as of 03/27/15

Outperforming Sectors: Healthcare +6.66% YTD, Consumer discretionary +3.82% YTD, Telecommunication services +0.32% YTD and Consumer staples +0.29% YTD.

Underperforming Sectors: Materials +0.02% YTD, Information technology –0.04% YTD, Industrials –1.79% YTD, Financials –3.15% YTD, Energy –4.66% YTD and Utilities % –7.18%

YTD. |