|

The S&P 500 took a 3.62% nosedive for the week to close at 2,023.04 on Friday, as U.S. Federal Reserve rate hike fears began to set in. S&P 500 Energy got crushed after the U.S. Energy Information Administration

(EIA) said on Wednesday that U.S. commercial crude oil inventories rose to 482.81 million barrels, up 4.2 million barrels, for the week ending November 6. Analysts had expected an inventory build of 791K barrels.

The International Energy Agency (IEA) said in its November report released on Friday that global stockpiles of crude oil have reached a record 3 billion barrels and demand growth is forecasted to slow to 1.2 million barrels a day in 2016. Earlier in the week, IEA Executive Director Fatih Birol told CNBC that they could not rule out the scenario that crude oil prices would remain close to $50 a barrel until the end of 2020, before rising gradually back to $85 a barrel in 2040.

The Commerce Department said on Thursday that retail sales edged up just 0.1% in October, after being unchanged in September. Economists had forecasted sales increasing 0.3%. Sales of automobiles fell 0.5% last month, after rising 1.4% in September. Jennifer Lee, a senior economist at BMO Capital Markets told Reuters, "Admittedly, this is a not a great start to the fourth quarter, which is important as we head toward the holiday shopping season,".

The news of weak U.S. retail sales for October came on the heels of announcements this week from Macy’s and Nordstrom, two of the nation’s largest department store chains, that they cut their sales guidance for next quarter, which is the holiday shopping season. Wall Street has high hopes that people will migrate their holiday shopping to online sites such as

amazon.com. That is a wild guess, at best, as amazon.com never discloses exactly what they are selling in their earnings statements.

Things are beginning to fall apart in the United States economy. The CEO of U.S. Steel said last week that the company needs to close more plants to cut costs. Oil giants, Exxon and Chevron, just announced combined layoffs of 14,000 workers and cuts in their capital-spending budgets. On their October 13 earnings call, Daniel

Florness, CFO of Fastenal, the largest fastener distributor in North America, said the following, “The industrial environment is in a recession - I don’t care what anybody says, because nobody knows that market better than we do”.

Several Fed officials are now saying that they are ready to raise rates despite weak U.S. retail sales and an industrial sector that is heading into a technical recession. According to the New York Times, William C. Dudley, the president of the Federal Reserve Bank of New York, said on Thursday that he sees a stronger case for moving ahead as the risks of acting too soon and waiting too long as “nearly balanced.”

Federal Reserve Bank of St. Louis President James Bullard, said in a speech in Washington on Thursday that, “The U.S. economy is quite close to normal today based on an unemployment rate of 5 percent, which is essentially at the committee’s estimate of the long-run rate, and inflation net of the 2014 oil price shock only slightly below the committee’s target.”

It seems like the Fed is now banking on the U.S. unemployment rate at 5% to justify a rate hike at the next FOMC meeting on December 16. Just a reminder, Japan’s unemployment rate now stands at 3.4% and their economy likely fell into a technical recession in the third-quarter.

On Thursday, in a paper prepared for the upcoming Group of 20 meeting in Turkey, the International Monetary Fund (IMF) warned the U.S. Federal Reserve for the third time, or more, to wait and see for firm signs of rising inflation, as well as a stronger labor market before hiking benchmark interest rates.

The federal funds futures, traded on the Chicago Mercantile Exchange and commonly used to estimate the market’s views on the likelihood of changes in U.S. monetary policy, indicate 30.3% odds for a quarter-point rate hike and 69.8% odds for a half-point rate hike at the Fed's December FOMC meeting, according to data from the CME Group as of November 13.

The yield of the U.S. 10-Year Treasury Note pulled back 2.15% for the week to close at 2.275% on Friday, while the U.S. dollar index (DXY) inched down 0.16% from the previous week, to close at 99.097, after breaking out the key technical head resistance at 98.14 last week. The yield of the U.S. 2-Year Treasury Note tanked 4.38% to close at 0.851% on Friday, driving the yield spread between the 10-year and 2-year Treasury Notes down 1.11% to 1.424 percentage points for the week.

The yield spread between the 10-year and 2-year Treasury Notes fell on October 29 to 1.37 percentage points, the lowest in six months. Falling spreads may indicate worsening economic conditions in the future, resulting in a flattening yield curve. A very low or negative spread could signal an upcoming recession.

The best performing S&P 500 sector for the week was Utilities, which inched up 0.35%, despite that the S&P 500 was down 3.62%. The worst performing S&P 500 sectors for the week were Energy, Information technology and Consumer discretionary, which were down 5.59%, 4.60% and 4.57%, respectively.

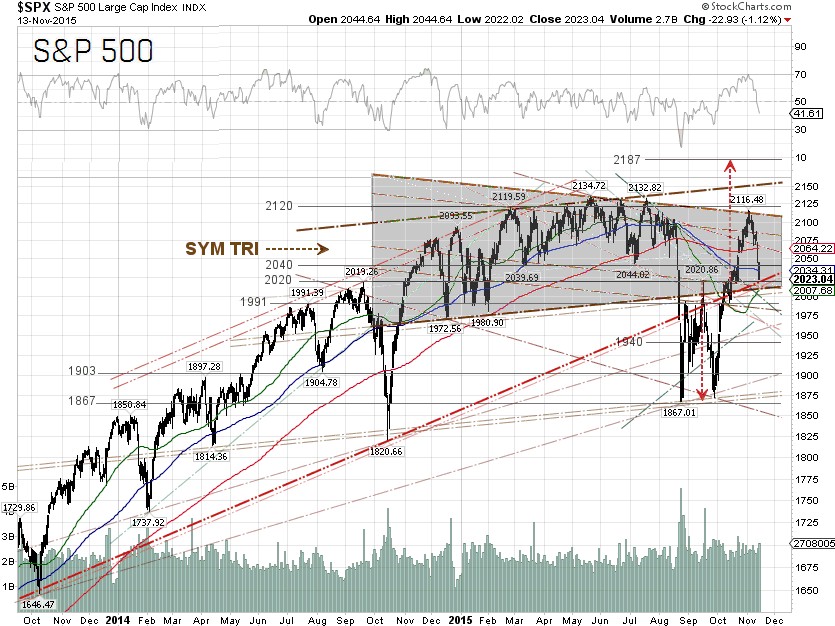

Technically, the S&P 500 pulled back further from the upper trendline resistance of the symmetrical triangle (SYM TRI) chart pattern and broke down through the 100-day and 200-day SMAs. The index is now supported by a long-term trendline, that goes back to late-2013. The Paris terrorist attacks could put more selling pressure on the S&P 500, but we expect the index to bounce off the 50-day SMA. If the 50-day SMA support fails, the S&P 500 could pull back to as low as the 1,975 level.

The near-term headline risks for next week are the CPI report, the FOMC minutes, and that Fed officials will be out talking again. One should expect higher than usual market volatility, as next week is also options expiration week. Home Depot and other retailers will report their quarterly earnings, and guidance outlooks, so let’s see whether we are going to have a “Bleak Friday” or a “Black Friday” this holiday shopping season.

S&P 500 Summary: –1.74% YTD as of 11/13/15

Barclay Hedge Fund Index: +0.69% YTD

Outperforming Sectors: Consumer discretionary +7.59% YTD, Information technology +3.09%YTD and Healthcare +1.38% YTD.

Underperforming Sectors: Consumer staples –1.77% YTD, Financials –3.56% YTD, Industrials –4.3% YTD, Telecommunication services –6.46% YTD, Materials –8.77% YTD, Utilities –10.53% YTD and Energy –17.57%

YTD. |