|

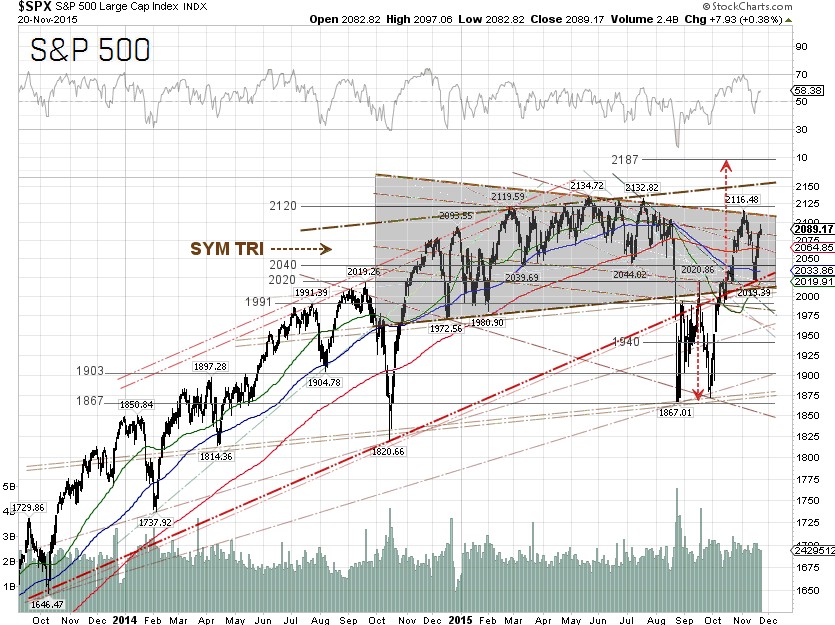

S&P 500 bounced off the 2-year trendline support at 2,019.39 and shrugged off the headline news concerning the Islamic terrorist group, Islamic State of Iraq and Syria (ISIS), that released a video on Monday threatening Washington D.C. with Paris-style attacks. Short sellers scrambled to cover their positions after the index broke though the 100-day

SMA, which sent the S&P 500 up 1.49% on Monday. Short sellers could have become overly confident that the S&P 500 would continue to move lower after the index took a 3.62% nosedive last week.

According to the Commitment of Traders (COT) data released by the Commodity Futures Trading Commission

(CFTC) each Friday, as of November 17, there are 166,045 short positions of S&P 500 consolidated futures, traded on the Chicago Mercantile Exchange by leveraged funds, a decrease of 9,248 short positions from the previous week. This is compared to about 66,015 long positions, down 224 from the previous week. The data suggested that until Tuesday, hedge funds were reducing their net short positions by 9,472 contracts, worth about $4.85 billion, where contracts of S&P 500 futures are traded in units of $250.00 x S&P 500 index.

The U.S. Labor Department said on Tuesday that its Consumer Price Index (CPI) increased 0.2% month-over-month in October on a seasonally adjusted basis, in line with economists’ forecast polled by Reuters. The September CPI was revised to a 0.2% decline. In the 12 months through October, the CPI inched up 0.2% after being unchanged in September, compared to the estimate of a 0.1% gain from a year ago. The U.S. Federal Reserve usually prefers the Commerce Department’s personal consumption expenditures, or

PCE, figures for a rate hike decision.

Separately, the Fed said on Tuesday that U.S. industrial production fell 0.2% for the second straight month in October, missing the economists’ forecast of a 0.1% gain, according to Reuters. A strong dollar is restraining U.S. inflation and has reduced overseas demand for U.S. manufactured products.

The U.S. Federal Reserve minutes of the October 27-28 FOMC meeting was released on Wednesday, stating “Most participants anticipated that, based on their assessment of the current economic situation and their outlook for economic activity, the labor market, and inflation, these conditions could well be met by the time of the next meeting,”.

The minutes also stated that “some” Fed officials, in October, felt it was already time to raise rates. “Some others” believed the economy wasn’t ready. Chicago Fed President Charles Evans and Boston Fed President Eric

Rosengren, made their cases last week for a slow and gradual rate increase to give officials time to analyze the effect of their decisions on the economy. St. Louis Fed President James Bullard and Richmond Fed President Jeffrey

Lacker, on the other hand, told The Wall Street Journal last week that they don’t want to get locked into a particular rate path.

The

S&P 500 surged 1.62% on Wednesday, as investors digested the

Fed minutes and interpreted the wording that Fed decisions are

still split and the rate hikes, if any, could be slow and

gradual. The big market run-up was also in part due to Goldman

Sachs adding Apple Inc. [NASDAQ:AAPL] to its "conviction

buy list", and forecasts the stock rallying more than 40%

over the next 12 months. It was most likely possible that short

sellers were forced to cover their positions for the second time

this week, after the index broke though 200-day SMA.

The index inched up 0.38% to close at 2089.17 on Friday, after

European Central Bank (ECB) President Mario Draghi gave a speech

at the European Banking Congress in Frankfurt, underlining the

ECB’s concerns about eurozone inflation and hinted at more

quantitative easing. The market is pricing in various measures

from the ECB, to be announced at its Governing Council meeting

on December 3, including an expansion of the 1.1 trillion euro

bond-buying program or measures such as taking the deposit rate

further below zero. The EUR/USD currency pair tanked 0.82% on

Friday, to close at 1.0647 dollars per euro, near the 6-month

low.

For the week, the S&P 500 surged 3.27%, the best weekly gain in almost a year. Of the 481 S&P 500 companies that have reported earnings so far, to November 20 for the third-quarter 2015, the blended earnings have declined by 1.6%, according to FactSet. If this is the final blended earnings decline number for the quarter, it will mark the first time since the second-quarter and third-quarter of 2009 that the index has seen two consecutive quarters of year-over-year declines in earnings.

For the current year 2015, analysts at FactSet estimate that the S&P 500 would post a 3.0% decline in earnings and a 3.4% decline in revenue. This would be the first time for the index to report a year-over-year decline in earnings and revenue on an annual basis since the global financial crisis in 2009.

The yield of the U.S. 10-Year Treasury Note pulled back another 0.48% for the week to close at 2.264% on Friday. The yield of the U.S. 2-Year Treasury Note surged 8.23% to close at 0.921% on Friday, driving the yield spread between the 10-year and 2-year Treasury Notes down 5.69% to 1.343 percentage points for the week, the lowest in six months. Falling spreads may indicate worsening economic conditions in the future, resulting in a flattening yield curve. A very low or negative spread could signal an upcoming recession.

The federal funds futures, traded on the Chicago Mercantile Exchange and commonly used to estimate the market’s views on the likelihood of changes in U.S. monetary policy, dropped to 26.4% odds from 30.3% odds last week for a quarter-point rate hike at the Fed’s FOMC meeting on December 15-16 while the odds for a half-point rate hike jumped to 73.6% from 69.8% last week, according to data from the CME Group as of November 20.

The best performing S&P 500 sectors for the week were Consumer discretionary and Information technology, which surged 4.51% and 4.27%, respectively. Both sectors were the worst performing sectors last week. The S&P 500 Healthcare sector underperformed this week, as the sector tumbled 1.63% on Thursday after UnitedHealth Group Inc [NYSE: UNH], one of the largest health insurers in the U.S, warned that the company is considering pulling the plug on the Obamacare by 2017.

The worst performing S&P 500 sectors for the week were Energy, Utilities and Materials, which were up 1.31%, 2.01% and 2.48%, respectively. The Energy sector was the best performing sector last week.

S&P 500 Summary: +1.47% YTD as of 11/20/15

Barclay Hedge Fund Index: +0.72% YTD

Outperforming Sectors: Consumer discretionary +12.45% YTD, Information technology +7.49% YTD and Healthcare +4.17% YTD.

Underperforming Sectors: Consumer staples +0.71% YTD, Financials –0.54% YTD, Industrials –1.24% YTD, Telecommunication services –3.43% YTD, Materials –6.5% YTD, Utilities –8.73% YTD and Energy –16.49%

YTD. |